Conversation Starter

Related Posts

Here are some awesome apps for investment:-

1.Groww

All in one app- investment in Mutual funds,stocks,IPO,FD,Gold.

Link:- https://app.groww.in/v3cO/61bcf14

2. Cred

For managing all credit cards at one place. Think as someone is paying you for your credit card bills.

Link:- https://app.cred.club/spQx/ce090339

3.INDMoney

Invest in foreign stocks and efts. As you need to diversify your portfolio.

Link:-https://indmoney.onelink.me/RmHC/9cb8da54

4.WazirX

Its my favourite for crypto investments.

Link:-https://wazirx.com/invite/j9kk5ted

5.12%club

For parking your emergency funds and getting 12% p.a is exceptionally good.

Link:-https://twelveclub.onelink.me/2Cmd/25922c

Never put all eggs in one basket.

Off Topic : 1) When Does a software engineer start financial planning for retirement since the our Career span is only 15-20 years on average.

2) How much and which schemes to invest to mitigate the risk?

3) How much do we need for retirement? Tata Consultancy Infosys Mindtree IBM Wipro Capgemini Cognizant HCL Technologies

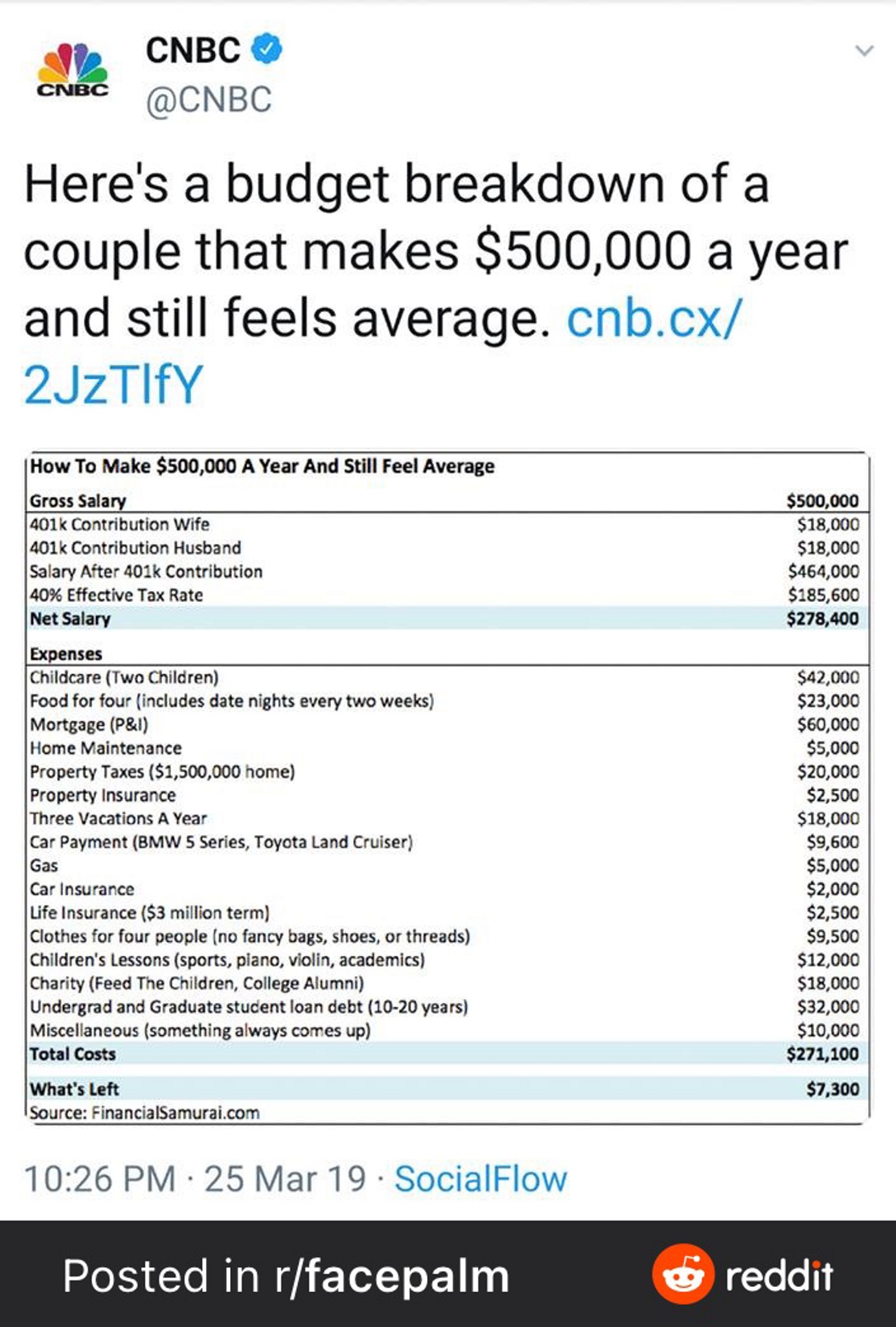

Nyc couple with $0.5m in income who feels average

Average salary in MSCI for an Assoc role?

Bain & Company Can we start a salary thread to get an idea about the salaries in Europe for different job functions, I can find solid data of tech salaries (SWE, PM, etc) but hard to find consulting salaries.

My TC - 48k +2-3k bonus, Consultant, Data & Analytics, Netherlands.

EY Deloitte PwC Accenture McKinsey & Company BCG Platinion Bain & Company KPMG

More Posts

Biggest cons of vending machines?

Rising Star

Additional Posts in The Worklife Bowl

Found this hilarious!!!

Anyone have any good book recommendations?

Conversation Starter

How long did you take off time from COVID?

Any advice on my current Vanguard Portfolio ?

Pro

Rising Star

Rising Star

New to Fishbowl?

unlock all discussions on Fishbowl.

Because you’d pay much more interest over the entire life of the loan as compared to paying it off over a shorter period.

D12 is right. Student Loan Cancellation will happen in our lifetime. No sense paying anything more than the minimum. I work overseas so my on-time monthly payments are $0. The moment I go back to the US, ~17k/year in loan payments will be factored into my budget. Unless someone give you a sweetheart 1-2% 30yr private loan, not worth paying off.

Enthusiast

So I’m the opposite, I put 2K+ a month to my loans and treat it like another rent - my savings don’t go up but I know after it’s paid off I never have to worry about it again and can save the money and go invest

Doing the same, about $70k left in loans, pay between $1000-2000 per month. I want the loans gone (especially w interest paused) so I can start saving and not worry about them. I think it’s the smart move to pay them as fast as possible and what financial advisors have told me.

I have low interest government loans that I have extended to the max. I will be 48 by the time they are paid off. I don’t care.

Maybe it’s a psychological thing but I enjoy watching my stocks, 401k, Roth IRA, kids 529 etc grow while I pay some shitty student loan debt. College and higher level education is mostly a scam. MBA here 😤

Actually, if you can afford to pay off sooner than later, that’s a much better way to go.

The years and decades ahead won’t perform as a guarantee, that you will be quite able, to pay back this loan easy peazy...

Umm did you study math at any point in your life?

Coming from GT1! Love this guy

Chief

All this math to prove OP can or cannot make more than he loses in interest...when OP openly says he’s just going to fritter the monthly cash away.

He just thinks fun money now is worth debt later.

He and so, so many people...typically doesn’t end well, but OP has that shining confidence of youth plus a little education. Bet he lets his credit card balances roll, too. Sigh.

Math. The answer is math.

I do the same assuming the rest is going to be forgiven, then I’ll just pay the taxes.

I graduated with only $17k and plan to pay it off end of next year...I hope your ROI for pulling such loans pays off. Sheesh. I didn’t even pay half of that to get where I’m at

The interest you pay to bank will eventually be 10 to 20k more than your loan

Chief

I'm curious what's your interest rate. 200/month on loan that size seems really low

Because being a first year I have few expenses compared to what I will have after I have a family and a mortgage and am further on in my career. I also want the flexibility to take a lower paying job in the future.

OP your logic is akin to saying I have a 100k job that pays all my bills and fit my lifestyle so why take the same job at another firm for 120k. I mean i guess it still affords your lifestyle that is true but just throwing extra free money away

“The borrower is slave to the lender.” That’s why.

Some of us don’t want to assume we will have well paying jobs for 30 years or that the investments you make will actually fare better than the interest you are paying. I personally value being out of debt faster. Then, if I have money to invest, fine. There also seems to be this assumption that investing is a “safe”option and that you will always be better off than the money you are giving up on your student loan. I was lucky, I got out with my bachelors with only $10k in debt and my masters later for $30K in debt. I was completely paid off in 3 years with my masters.

I worked in consulting through law school, and paid off my loans as I went - it was definitely the right choice for me. If I hadn't, it would have been about $70k when I graduated. Debt stresses me out so much that I would have been miserable.

I'm concerned that an Attorney is asking this question...

What bank did you finance that with?

I agree with OP. I have a 30 year loan at 2.9%. I was able to take the money I’m not paying on student loans to put a down payment on a house. That house has gone up in value so much it more than compensates for the interest on my student loans.

I bought no money down in 2004 and stuck it out until the market rebounded. I didn’t want to ruin my credit but I felt a sense of obligation to fulfill my promise to pay on the loan. But I saw a lot of people walk away in 2008 when things were bleak even if they could afford the payments.

It is rather freeing to have low debt. My wife and worked quickly to pay off all our student loans, our cars, and live a relatively frugal life style. We save about 35-40% of our after tax income, but she is a stay at home mom to our 2 little kids. Only having our mortgage which is relatively conservative (18% of gross income with tax/ins escrow).

Debt makes a HUGE difference. IE take the family with 2 average car payments, spent $100k more for a fancier house, and still have student loans of $300/month... In order to have as much left over for the rest of life and pay the taxes... they need to make another $35-40k annually gross. My brother and his wife make $50k more than me and my wife do... but we are substantially less stressed in our finances, and have marginally less left over.

Conversation Starter

By paying off quicker you’re reducing overall payments and hence saving on interest $$ that accumulate over time. It’s a matter of what matters more to you.. additional money long term vs more liquid money short term. If what you’re doing works for you, keep doing it

Rising Star

GT1, please stop giving advice financial advice. You clearly aren’t understanding the actual issue at hand here.

Depends on the int rate