Related Posts

More Posts

What are Google Canada email addresses?

How long do your suits typically last?

Additional Posts in Personal Investment Chatter

Advise for TFSA investment in Toronto?

Rising Star

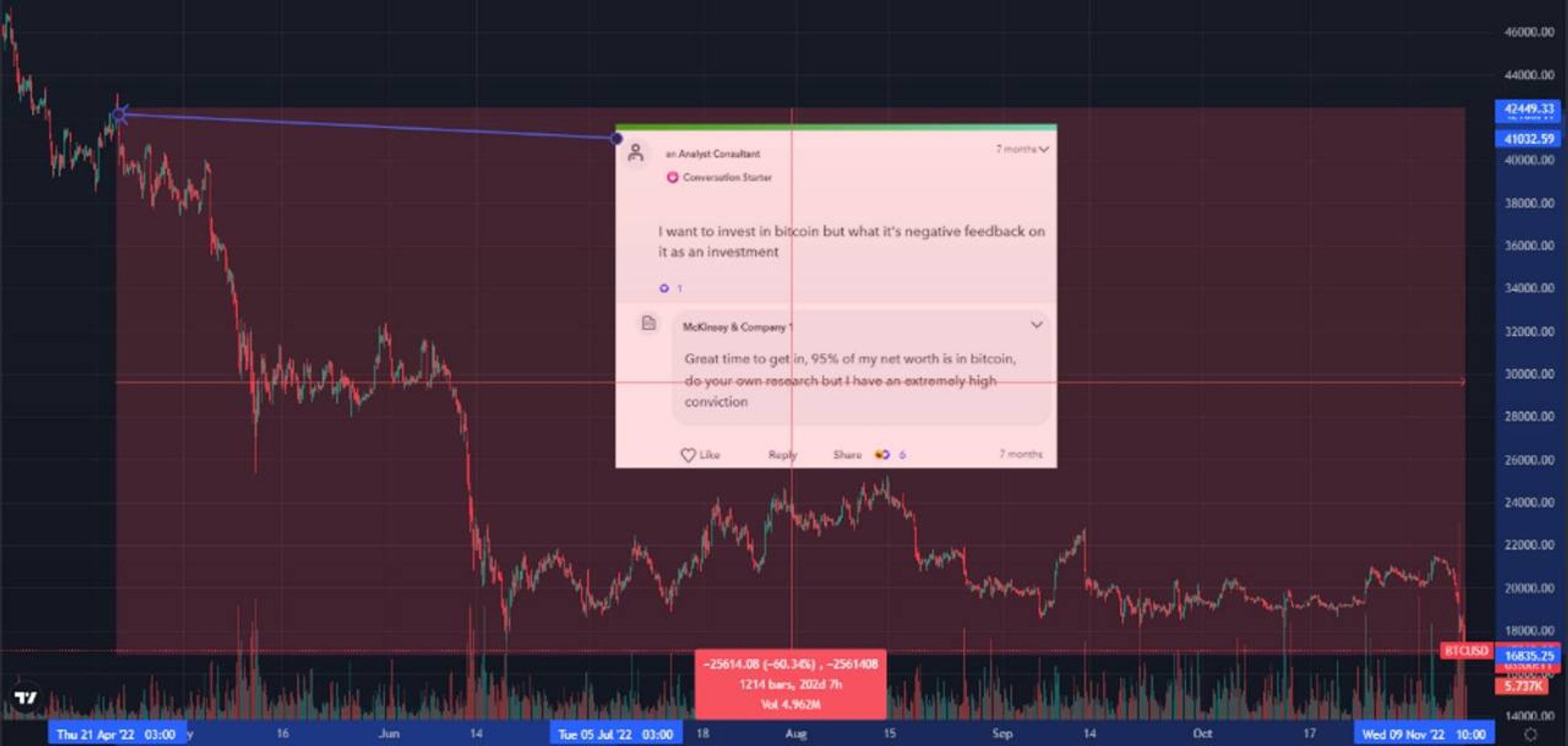

I know it's a favorite among this crowd ..

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

It depends on if you want to pay tax now or later. If you think your bracket is higher now than when you withdraw in retirement do traditional, if not Roth. Most people have no way of knowing so a split between the 2 may make sense

Agree. I think Roth is a no brainer if you are in a low bracket. After that it is a guess and a split may be best. I just see so many people saying it is stupid to do traditional without actually thinking about how withdrawals might look

If you search within this bowl you’ll see suggestions for your income level are to establish an emergency fund first (~3-6 months of expenses), max your 401k employer match, then max your Roth. After that, you can max HSA, rest of 401k or put the rest in a Brokerage account depending on your preference.

Pro

Roth is an adjective—there is a Roth 401k vs traditional 401k, and a Roth IRA vs traditional IRA. The question is to go with Roth 401k or traditional 401k. What I heard is Roth 401k for when you’re in a low tax bracket (early career etc) then traditional 401k when you’re at the peak of your earning

Roth. Your tax bracket will only increase as you age and move higher in your career

That is why I suggest a split

People always say “Roth because your income will increase over time”.

This is too simplistic a way to look at it. You’re likely going to start drawing down from your 401k when your regular income is actually $0 (because you’ll be retired) - so you won’t be in a higher tax bracket when you start withdrawing like people assume. You’ll probably actually be in a lower bracket.

If you have $0 of W2 income (which you will if you’re retired) you can draw down more than you think from a pretax 401k while paying $0 in taxes.

SC2, I assume you mean from traditional. Only traditional has RMDs. Converting from traditional to Roth makes sense often, but it all shows up as income that year and can impact your total income and all the things that go with that.

This bowl has a lot of responses. I’ll also note that if you’re planning to go to grad school, the Traditional may be better (so you can convert to Roth when you’re in a lower tax bracket during school).

I do a little of both - my 401k is all traditional, and IRA all Roth

Rising Star

Roth & taxes probably can’t drop in future as our debt keeps accumulating somebody has to pay it down.

Rising Star

This. I’m not leaving my money to chance. Historically speaking, we have lower tax rates

Both

Do all roth. As your salary rises over the years with promotions and job hops, you will become ineligible for roth contributions by maybe age 28 (assuming you stay in consulting and get promos or a new job every 2 yrs). Make those post-tax contributions now, and you still have decades for pre-tax contributions. But if you start with pre tax, you might not have the opportunity again in a handful of years.

I think op is talking about 401k. There is no income limit for Roth 401k.

Rising Star

Also consider if you’re in a state with high income tax. If you plan to live their forever, even in retirement, then either could work for you. If you plan to move to a state later on with lower or no income tax, then go with a traditional 401k.

Roth

Roth

For my 401k I split. But favoring roth more. Maybe like 80% roth & 20% trad. I don't want to worry about taxes down the line even tho it could cost more, but less stressful for me. If I need more $ now, then I'll change it up to favor trad which I've done.

Roth

Why Roth? Traditional may be better. Or a split

Roth.. returns are not taxed. Returns are taxed on withdrawal in traditional. At this stage in your life, that compounding growth will be significant

Traditional - it could lower your tax bracket and the taxes you need to pay

Roth would allow you to roll into a Roth IRA later without tax consequences, which is the only categorization that doesn’t have RMDs (MRDs).

As long as you are willing to pay the taxes on the conversion, which can get complicated if you don’t do it all at once. I.e., what to convert, when to convert. Sounds like an idea for an app....

I am 23 and have both a 401k to take advantage of employer match and a Roth IRA