Related Posts

Conversation Starter

More Posts

BGC becoming strict in all companies these days

Community Builder

Community Builder

Additional Posts in FIRE Financial Independence Retire Early

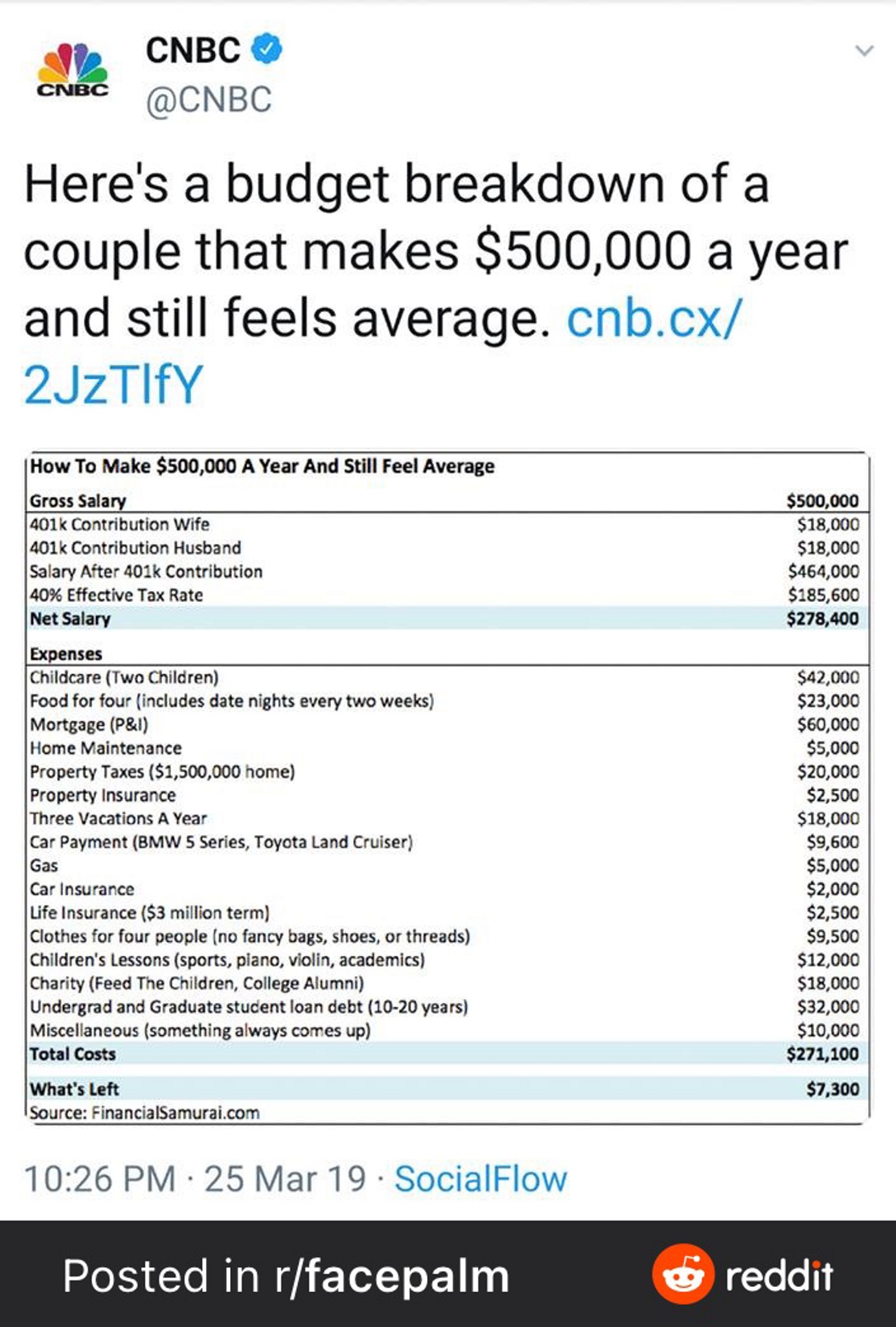

Nyc couple with $0.5m in income who feels average

Visual Storyteller

Anonymous User

Coach

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

I would pay the extra $500 to finish the loan in 9 years as you will most likely not be a high earner when you FIRE

Mentor

I wouldn’t. The interest is deductible against your rental income, so assuming your effective tax rate is 30% that 4.875% IR is actually only 3.4%

In addition, invest the extra cash in an index fund/market. You can make more than the IR on the mortgage

Mentor

As long as you have the principal and COULD pay the house off, you could arguably have that peace of mind already tho

Mentor

I was more responding to amazon1 with that post

I agree with both but for me the piece of mind of owning the property and making extra net profit from the rental side out weighs the possible 29k in interest you might make from the market in 9 years

Do you have a prepayment penalty? All of my organization’s properties do. But they are larger multifamily and straight commercial.

Thanks for this take - hadnt given this too much thought but I am achieving my goals as is. I bought this place at the bottom of the market in 2010 in an upscale neighborhood, so making a good return. Anything I bought now would not be as good of an ROI. I also sold my personal residence and might buy something else to live in for the next few years.

Carry as much as possible and take (or accumulate if you’re over the income limit) as much of the interest deduction. Your interest rate is less than inflation - that means you actually will pay less by holding it!

Why is 4.875 the best you can get with today's low rates?

The Author is correct on this. The gov’t subsidizes primary residential mortgages. 4.2 is pretty good for investment property. But it completely depends on the income from it.