Related Posts

Conversation Starter

More Posts

Anyone here from Investment Banking at Houlihan Lokey, Evercore or Lazard in London (UK)? I’m currently working in Corporate Finance M&A in GT UK. I’d want to move to one of these banks next year so would like to know about work culture, teams, opportunities, salaries and bonuses. Appreciate your kind help on this

Enthusiast

8/28 Thread (General):

Mentor

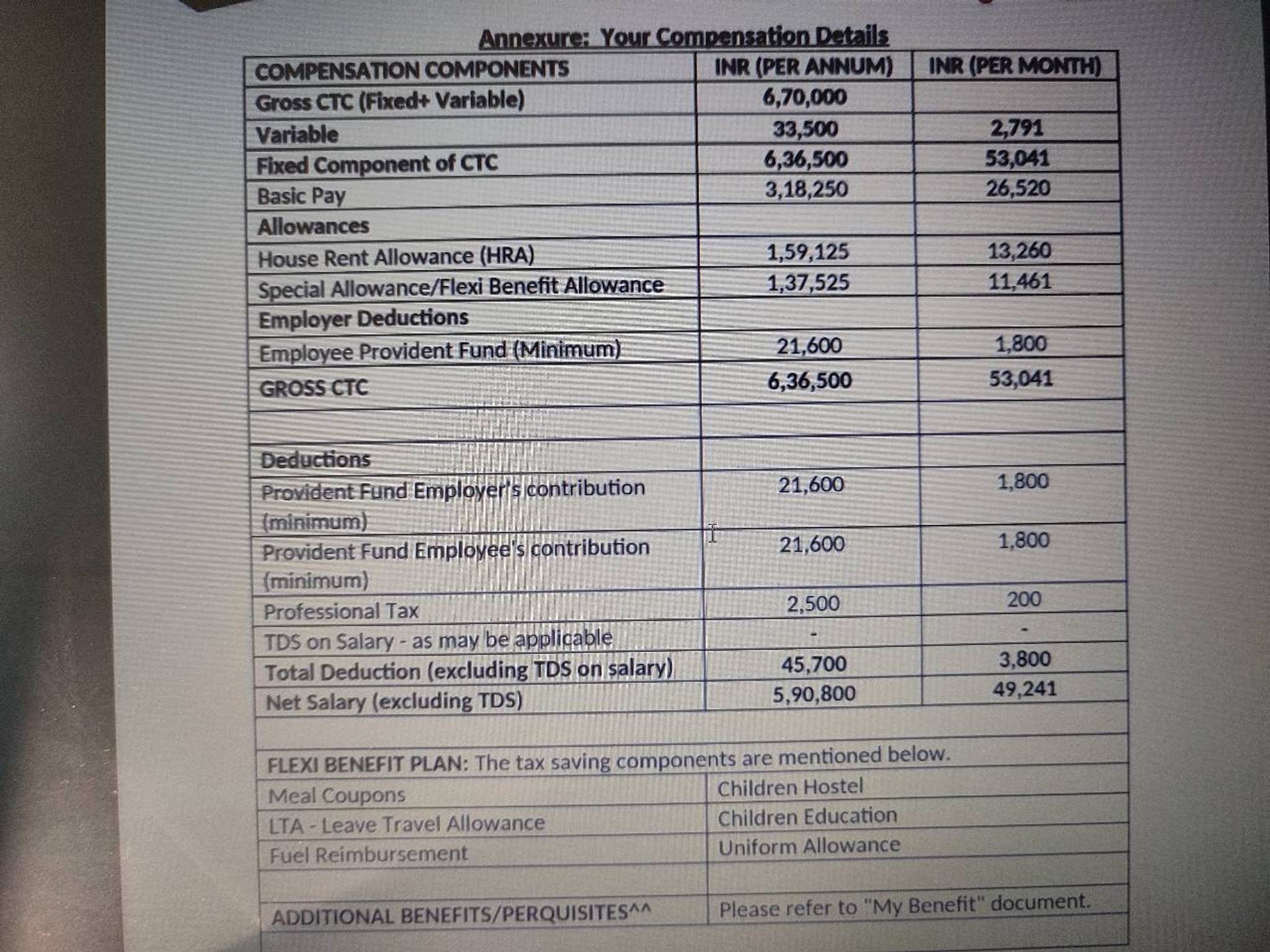

WPF merging with Alight Solutions!

Bowl Leader

Additional Posts in Personal Investment Chatter

Conversation Starter

Enthusiast

Pro

Tendies? 😊 🤚💎🤚

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

1. Never buy a car which costs more than your annual salary.

2. Usually get a used car as your first car - helps build driving history and keeps insurance premium low - also helps to understand the cost of maintenance as well as how depreciation works.( I'm not saying a 2010 car, even 2017 cars should be cheap today and last for a while)

3. In terms of direct amount, the right amount is what you are comfortable paying in full today ( if 30k to pay at once feels too much for a car, don't loan it either)

Chief

The finance gurus would tell you to buy a car you can pay cash for as you don’t want to get a loan on a depreciating asset. How much do you have saved?

Put as little down as possible! Put the rest in the market. You can easily beat 3% over 4-5 years.

Conversation Starter

I’d you really are set on buying new, your guidelines for the maximum range should be 48 month financing with 20%, and your resulting payments should be less than 10% of your monthly income.

E.g financing a 25k car, 20% down = 5k cash down payment, then the 20k loan for 48 months depending on interest leaves you a ~400-500/month payment. Add monthly insurance then compare that to your monthly income and keep it under 10%

Agreed. If you plan to keep your car beyond the loan (which if you’re buying the car vs leasing, I presume you plan to keep), it also doesn’t matter. Ironically, my car has actually increased in value by $4k since purchasing last year (and 5k additional miles)—wouldn’t anticipate this happening on all purchases, but point being, 20% down should not be a black line.

Depends how much you value a car. You set the price you’re willing to pay