Related Posts

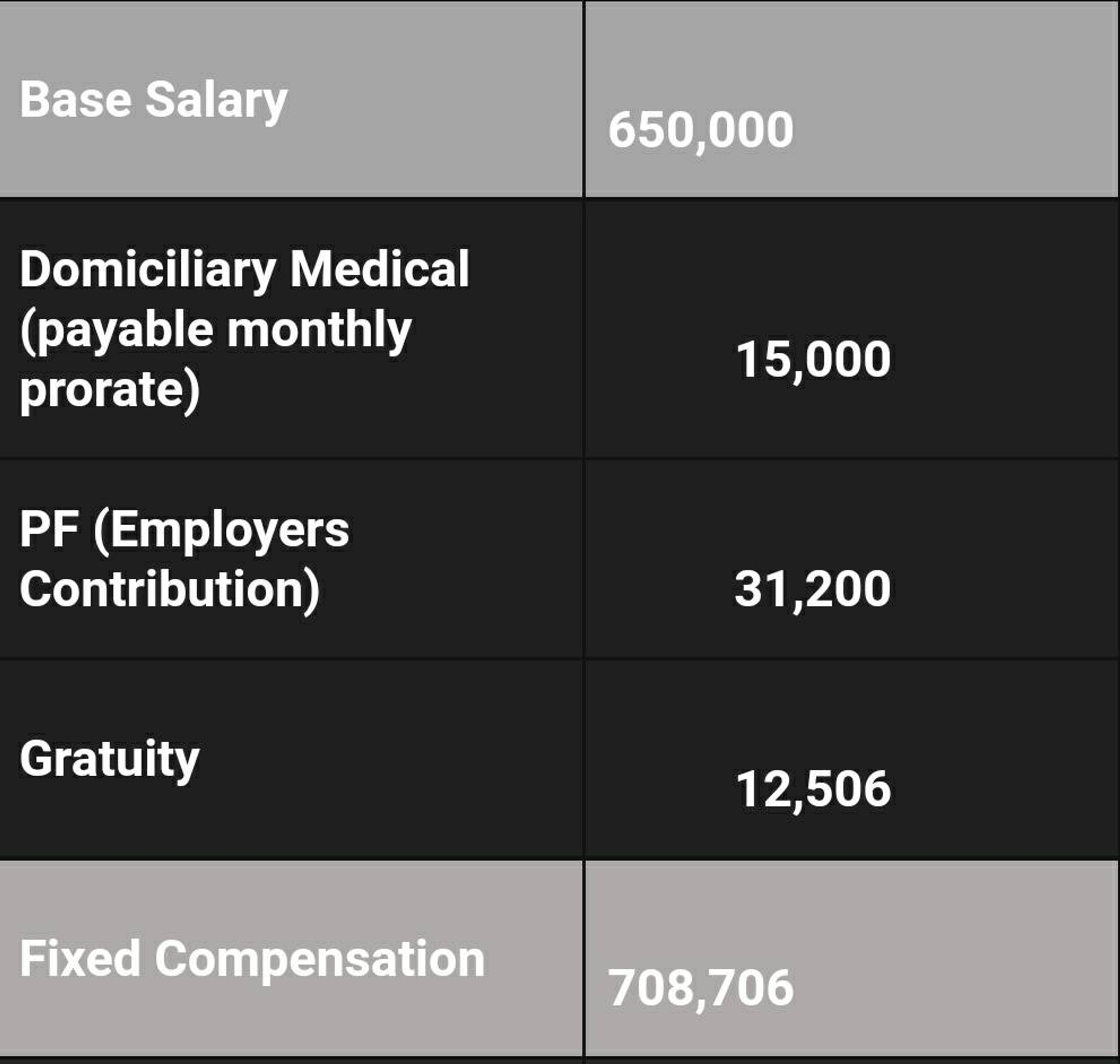

Its ey gds. please help.

Rising Star

Additional Posts in American Express India

Community Builder

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Its ey gds. please help.

Rising Star

Community Builder

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

Download the Fishbowl app to unlock all discussions on Fishbowl.

Copy and paste embed code on your site

Scan your QR code to download

Fishbowl app on your mobile

you can opt upto 30L coverage, by paying extra

Parents are covered from day1 with no waiting period for pre-existing diseases.

Thank you so much, this is great

Health insurance covers upto 8 lakhs, spouse and childrens included. Parents not included.No OPD benefits and 10 percent copay

If it is indeed a waiting period, then honestly it's a useless policy. Individuals who are younger can anyway get personal insurance at lower costs. Corporate insurance works for covering elderly, and 2 year waiting defeats the purpose.

When I was about to join a large MNC, I had the exact same question around health insurance — because onboarding decks usually sound reassuring, but the real clarity only comes when you actually need to use the policy.

From what I’ve seen with AMEX India, the corporate health cover is generally solid by employer standards. Coverage is usually on the higher side compared to many IT firms, often extending to dependents, with cashless hospitalisation across major networks. Room rent limits are typically reasonable, and maternity, daycare procedures, and pre-existing conditions are often covered from day one (though caps and waiting rules can still apply). That said, the *headline coverage amount* doesn’t always tell the full story.

The gap most people realise later is this: two employees can have the same “₹X lakh” cover, but very different real-world protection depending on city costs, sub-limits, claim settlement behaviour, and how the policy is structured internally. This is where I personally found value in using **Bima Analyze** before fully relying on any employer policy.

Bima Analyze doesn’t need document uploads. You just enter simple details like your city, family structure, insurer, and sum insured. Behind the scenes, it evaluates 100+ real-world factors — including location-based medical costs and insurer claim patterns — and then gives you a **BimaScore (400–1000)** that shows how strong your coverage actually is, not just on paper.

For someone joining AMEX, I’d still suggest understanding the corporate cover first — but also checking whether it’s enough for *your* situation or if a personal buffer policy makes sense.

If you want that clarity before joining, you can **Analyze Your Policy Now** here:

[https://bimascore.com?ref=forum](https://bimascore.com?ref=forum)

When parents already have pre-existing conditions, most of us enter the health insurance process with a lot of anxiety. I went through something similar while helping my parents — one with diabetes, the other with cardiac history — and quickly realized how confusing policy brochures can be. Everything looks “covered” on paper, but real clarity is missing.

The biggest problem I noticed is that most advice focuses on brand names or claim ratios, not on *how a policy actually behaves for a specific family*. Waiting periods, room rent limits, sub-limits on procedures, and how insurers treat chronic conditions vary widely — and these are exactly the things that matter for parents.

What helped me step back was looking at the policy from a strength and risk perspective instead of just price. I came across **Bima Analyze**, which doesn’t ask you to upload documents or decode policy wordings. You just enter basics like parents’ age, existing conditions, city, insurer, and sum insured. The AI then evaluates the policy across 100+ real-world factors — things like claim behavior for that insurer, city-wise hospitalization costs, and how policies historically handle pre-existing diseases.

The output is a **BimaScore (400–1000)** that reflects how strong or fragile the coverage actually is for your situation. That score helped me realize that one of the “popular” plans I was considering looked affordable but was structurally weak for chronic conditions. Another slightly costlier option turned out far more reliable long term.

For anyone in this thread dealing with parents’ health insurance, I’d strongly suggest evaluating policies this way before committing. It’s not about finding a perfect policy — it’s about reducing unpleasant surprises later.

You can **Analyze Your Policy Now** here:

[https://bimascore.com?ref=forum](https://bimascore.com?ref=forum)

Here’s a natural, experience-driven response suitable for that Glassdoor discussion:

---

I recently went through a similar situation when joining a new company, and I completely understand the anxiety around health coverage—especially when it comes to figuring out maximum coverage and overall protection. From what I’ve seen, corporate health policies often have good coverage, but the real question is whether it actually matches your needs and your family’s requirements. Just knowing the “maximum coverage” number doesn’t tell the full story; there can be sub-limits, co-pays, network restrictions, and exclusions that end up being more important.

When I joined my previous company, I started by evaluating my policy against real-world scenarios—like local hospital costs, specific conditions, and potential emergencies. That exercise helped me realize that even a high coverage number could leave gaps if not aligned properly with actual needs. This is where tools like **Bima Analyze** can be really handy. You can quickly feed in simple details—family structure, PIN code, insurer, sum insured—and it analyzes 100+ real-world factors to give you a **BimaScore**. That score gives a clear idea of the strength of your coverage, way beyond just the maximum sum insured.

Once I understood my policy better, I could see areas where I needed top-up coverage or alternatives, which really gave me peace of mind. Having a personalized view of coverage is far more empowering than relying on a generic policy description.

If you’re curious to check how your Amex health insurance stacks up and want a clear score of your actual coverage strength, you can **[Discover Your Score](https://bimascore.com?ref=forum)**. It helped me make an informed decision before even stepping into the office.

---

If you want, I can also draft a shorter, super-to-the-point version tailored for a quick Glassdoor reply. Do you want me to do that?