Rising Star

Related Posts

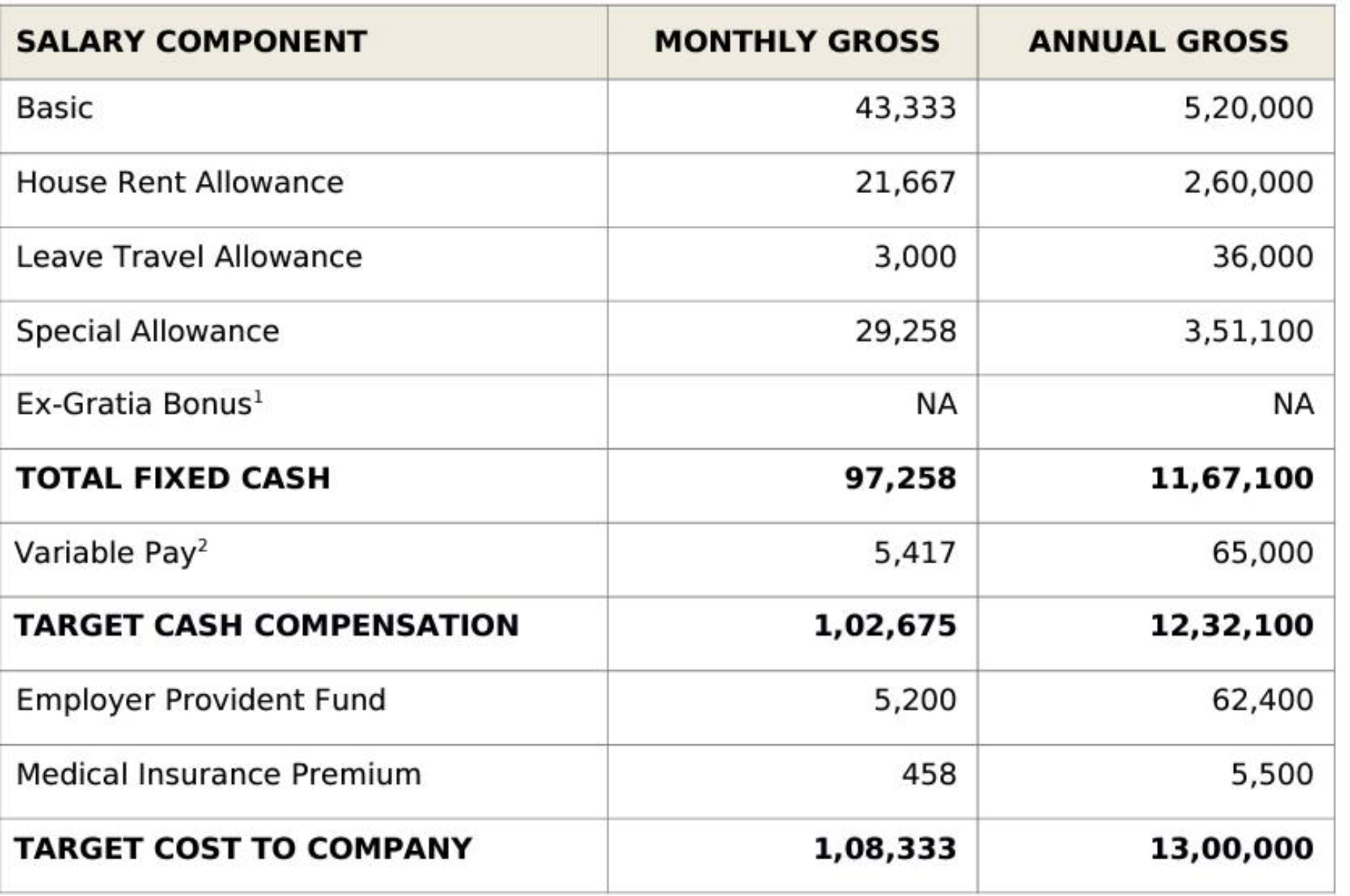

What will be the in-hand for this offer?

Kanye is amazing.

Conversation Starter

Additional Posts in Accounting

Passed my last CPA exam!! 🎉🎉🎉🎉🎉🎉🎉🎉

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

EDITED

I have experience with general and life insurance and pharma.

Pharma spend a lot of money on R& D and you need to consider whether if they carry any R&D amounts forward that the cfwd amount is not impaired. This would be by way of product specific versus R&D specific future cash flow anaylsis.

Insurance requires disclosure of income recognition, accounting for acquisition costs of new business (commissions and admin) and how claims are accounted for and reserved (including claims handling expenses).

Claims includes how both short tail claims (motor vehicle, home and contents etc) ate notified plus claims handling expenses and reserves are recognised as compared to long tail (professional liability, workers compensation, etc) claims and long tail claims not notified are reserved (usually supported by an actuarial assessment) including an allowance for claims handling, medical and legal expenses. (Long tail claims usually take many years to materialise and/or be settled).

In addition to short tail claims reserved based on reported (lodged) claims there is also an allowance booked for IBNR (Incurred but not reported).

On the other side there will also be Risks Held Covered (RHC) where policies are held on risk depite the premium not having been received from the policyholder. This needs to be dealt with in the revenue recognition accounting policies as does the policy for recognising Earned Premiums (EP) (how premium income from business written is recognised).

There are 2 layers of insurance. That which the insurer keeps as the first level of risk and then there is a further layer that the insurer lays off the excess risk for which it can write the premium income and lay off the excess risk by paying a premium to a reinsurer (mostly finding their way to a Lloyds of London Underwriting Syndicate).

From year to year, particularly in short tail business lisses can fluctuate markefly on an incurred basis. For example there may be no serious floods or bushfires in most years but ine year gets hit very badly but not enough to triggef the reinsurance pokicy for the eccess risk. Some insurance companies I have audited have been conservative with their reserves and also over a number of years build up a reserve for irregukar catastrophes below the reinsurance lower limit and also build up a restve for their deductible or first incurred losses on their catastrophe reinsurance. Catastrophe losses do not happen evenly from year to year and based on historical experience may occur say once each five years so a reserve would be built up to smooth out the losses by resrving as an expense against the premium income 1/5th of the estimated historical excess losses. The catastrophe reserves are usually supported by an actuarial report. The catastrophe losses are a cost of doing business annually and covers losses that are expected to arise ovee a oeriod longer than a year as a blimp in the losses experiences through a catastrophic event.

Insurers keep some risk for themselves but take steps based on the approved Risk Management Policy of laying off excess risk. (That is to say they may be happy to incur losses up to say $10 million but after that they lay the excess risk off with another insurer for the excess).

All of these accounting policies need to be disclosed as general insurance is a completely different animal to pharmaceutical. Life insurance is even more complicated although it relies more on actuarial assessments, mortality rates, etc.

I have experience with Pharma, but no knowledge of insurance so not sure how they align. Also, when you say SAP what are you referring to?