Related Posts

😂 this is too real

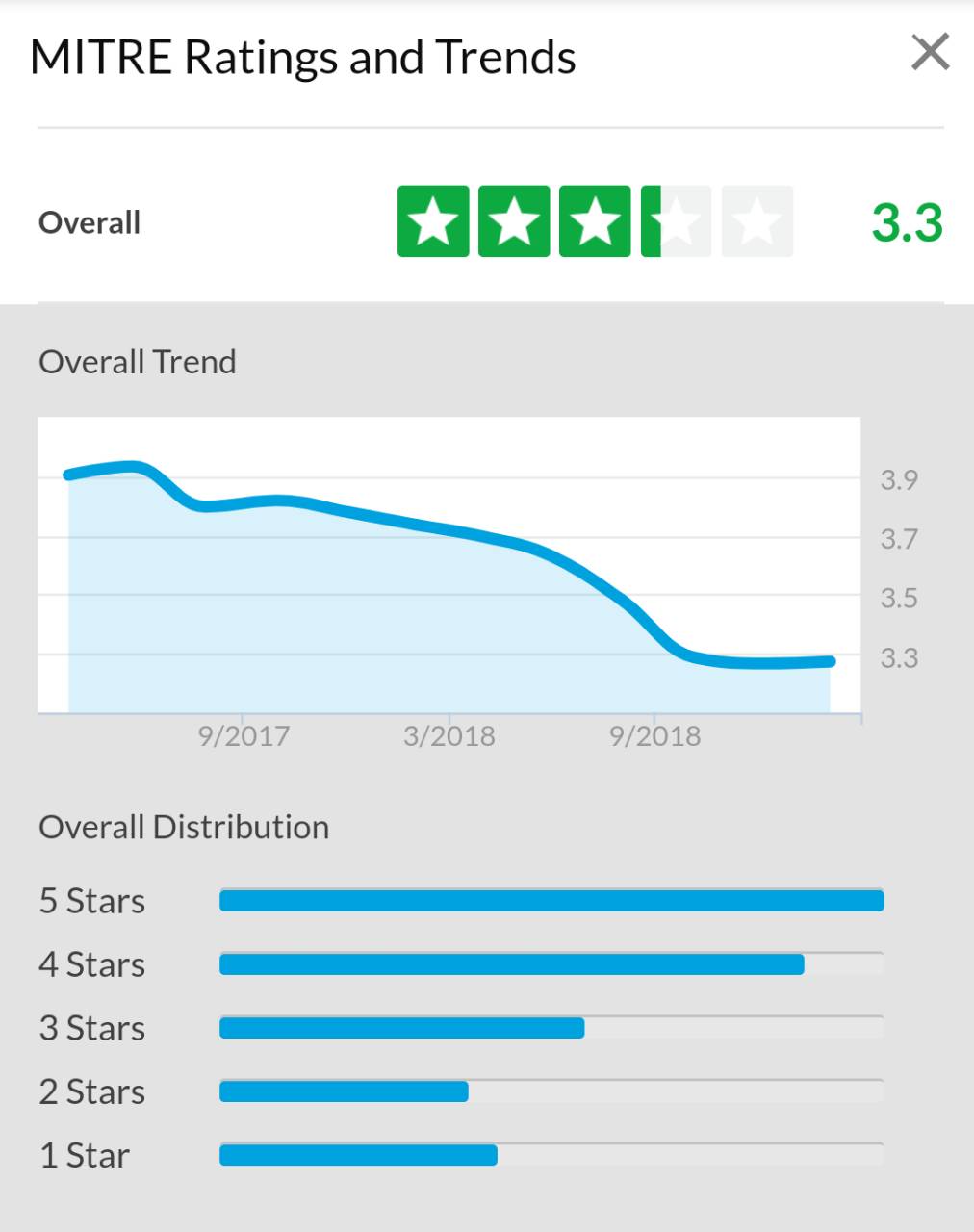

MITREs Glassdoor rating is like a ski slope.

Pro

What does these bands mean in EXL? (A,A2,B,C)

What’s the move tonight?!?!

Conversation Starter

Fishes, OK so this is true. Wipro is delaying the joining by half a month due to some restrictions or organisational changes & not ready to compensate for that half a month loss of salary. Very rude & absurd behaviour from them. Hence rejecting the offer as such company if u aren't sure when to ask for joining u may revoke the offer letter later on. Hence multiple options in hand is necessary nowadays. Infosys Tata Consultancy HCL Technologies

Pro

Additional Posts in Chicago

Thankful for live performances 🎭 🎤 🎶

Come on Bears we need a win!

Chicago fishes - have a 2 bed 2 bath available for rent immediately in Lakeview (near Montrose beach). Full amenity building with spectacular views of lake from all rooms, and easy access to public transit. Please DM if interested. Thank you!

https://www.zillow.com/homedetails/4250-N-Marine-Dr-APT-822-Chicago-IL-60613/3703720_zpid/

Anyone work at Revantage?

Best Christmas things to do with a two-year-old?

New to Fishbowl?

unlock all discussions on Fishbowl.

I think you can probably afford a $400k condo without adjusting your retirement contributions. Just be weary of the HOAs and don’t count on appreciation. It’s super neighborhood dependent and things seem to ebb and flow a lot in Chicago.

I have some friends that really struggled to sell their condo in LP. Reasonably priced and nice as well

This. I wouldn’t consider the home for the appreciation aspect because I know plenty of people who sold to break even (that’s just on purchase price, doesn’t factor in closing costs, upkeep, property taxes) after holding 5+ years in Chicago. But if you want to buy to settle down, that’s a totally valid reason too!

One thing with homeownership that’s worth considering is what you can own vs rent at the same monthly payment. Plus, the $50k you plan on putting down as a down payment could stay in the market in an index and appreciate at ~7-8% annually (historically), instead of being pulled and used for a down payment (just a thought).

There are a lot of missing variables here to be able to answer your question. How much are your monthly expenses? It is very possible to qualify for homes that you can’t necessarily afford. Are you planning on putting down $50k (and no more)? If so, the standard down payment is usually about 20% to avoid paying for PMI. That means you’re looking at a home ~$250k. Are there ones at that price point you like in the areas you’re interested in?

Would look around at areas / homes of interest, figure out the average price, figure out how much you want / can put down for a down payment, and then use a mortgage calculator (even the simple one on Zillow works) to understand your monthly payment including principal, interest, property taxes, utilities, etc. Does that payment work for you on a monthly basis with your other commitments?

Best of luck, you’ve got this!

I think it depends on how you feel about your “savings”. Some people aren’t great at investing and are behind but are better at saving cash. Vice versa.

General rule of thumb of retirement accounts is 1X your income by 30 - sounds like you’ve done that between tax deferred accounts.

You’ve also been able to save $100k combined which is a fantastic amount. Not many people are able to do this while meeting their investing goal, especially in Chicago.

If you are dead set on buying a property and need more cash, it’s not a bad idea to reduce your 401k contributions to the match to support your savings in the interim. Just know it’s hard to go back to increasing without getting a pay bump because home ownership is expensive.

Appreciate the replies!

I could lower my 401k contributions to have a larger take home. Right now my net take home is ~$5k/mo. We have $100k in savings between us in a HYSA and would use 50% of it for a down payment.

Your HHI is $180K with dual income and you’re at Google? One or both of you is really underpaid

I did very well at Google but hahaha I got laid off. That said, I’ll make over $200K on my house in the burbs when I sell. I wouldn’t invest in the city now as people are leaving, unless you intend to rent it down the road as an investment property

Chill out, buy a home, live your life.

OP you are doing great. Your future self will be grateful you are maxing out 401k.

Also, don’t beat yourself up about renting. One data point that I think might help you feel better:

- if you were to buy now with 10% down (roughly what you would need to do if you insist on staying in West Town), your first year of mortgage payments would only result in accumulating $1,600 of equity….which pales in comparison to your likely closing costs of at least $8,000. Your “investment” would be negative on paper for several years assuming the real estate market stays sane.