Related Posts

Conversation Starter

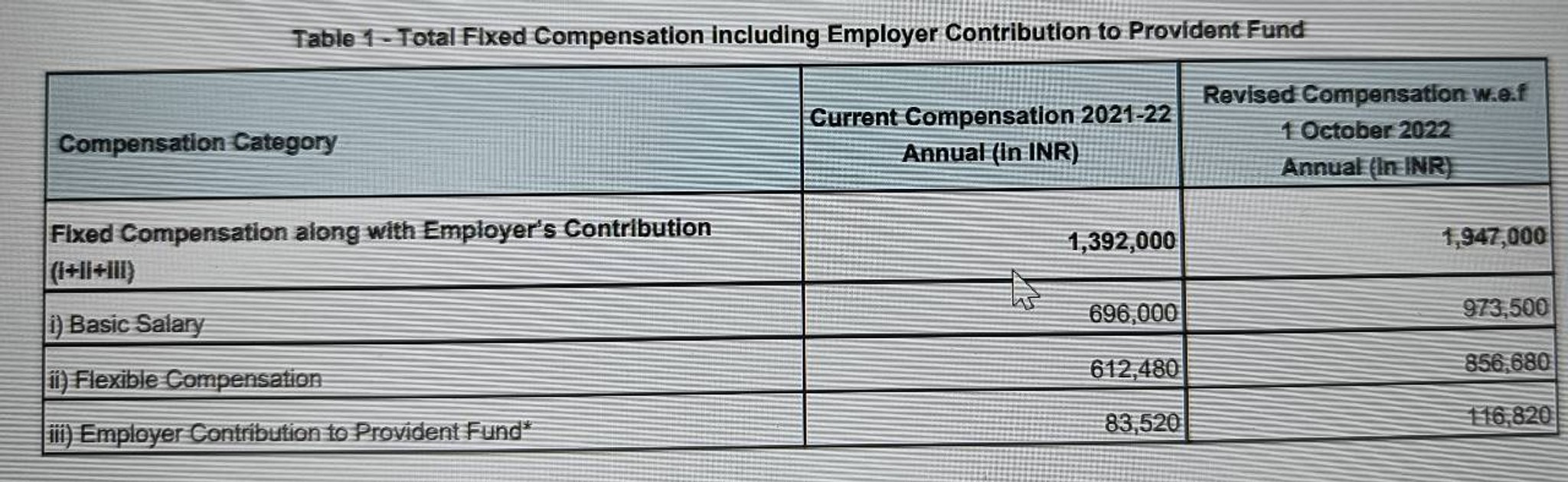

How much do strategy directors make these days?

Community Builder

Hi

Can anybody tell mw what will be inhand

More Posts

Anyone used to listen to botdf they were 14?😂

Bowl Leader

Additional Posts in Compensation in Consulting

What is the Deloitte MSP Team? Is it consulting?

Expected director base and bonus at strat&?

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Single 30 and making 175k TC in high cost of living city

Not that I don't think about it -- but really I don't stress / worry about budget that much anymore and stopped mentally comparing myself to peers at MBB / banking / big law / tech

401k & HSA set to max automatically;

$1.5k into brokerage a month automatically;

Anytime my HYSA gets above a 4-5 months of costs (emergency fund) will do an ad hoc dump into brokerage

Can go to restraunts / bars / trips I want without worrying about budget or cash flow

Definitely not "set for life" or anything but it's more stress free now

RSM1 -- by crazy do you mean 1.5k is a lot?

Yeah no debt -- still driving a paid off 2011 car bought used in ~2015; still renting; no grad school; no debt from UG

But also you said you make ~50k less; if you made the same it's ~2.5k/month post tax more into your budget -- comes down to limiting your expense increase with salary increases to focus on savings; i.e. resist the classic "lifestyle creep"

Not being facetious, but have never worried about money including when I was a graduate assistant making $1400 a month. Even then I was saving about $500 a month. Now that I make almost 20x that, it’s still the same. Maybe the fact that I’m originally from a developing economy in Africa where I knew people living in grinding poverty made me have context on what really matters in life.

I hope you arrive at that point and mindset

Eh if you'd have been one of the people you knew, I think your outlook might be different.

Having grown up in poverty in the US, the last thing I want is to live that way again.

I feel like it’s less your salary more so your net worth

When both my wife and I made manager, household income exceeded $350k in MCOL city. We had already bought a condo we could afford on SC pay. We treat ourselves to a few more luxuries with every pay bump, but don’t outpace it.

By the time we were 27 and 26

I can tell you that we are around 450k HHI in HCOL, and I am certainly worried about money. We can afford everything we need and put away money in 401k, but we are very rarely splurging, and our savings growth outside of retirement and emergency is mostly flat (we have mortgage, high taxes, live-in nanny, and some student loans but not much).

I did build a model for myself (yes, I'm that person) and calculated that, at 750k, we will be completely comfortable. Of course, more is always nice, but this is what i want to reach combined.

Live in nanny are usually cheaper because they discount for free rent

It wasnt a dollar amount thst really made the difference, it was when i paid my house off, paid for the kids college education (no student loans for them), and the end realized i had zero debt and possibly enough investments that i could retire tomorrow, sell my house and travel the world without issues. The kids are off to a grest start as a teacher and a diesel mechanic

When I hit 150k TC I realized I could live in the apartment I want, go to restaurants when I want, afford vacations, etc. all while saving significantly for retirement. I don't think of myself as frugal, but I'm not reckless either. However, it will be a different story if I have kids. It's hard to say what number I'll need them, but hopefully with dual incomes it won't be that much higher for me than what I make now (which is already more than $150k).

I think for me it was different levels of worry?

I probably stopped worrying about day to day when I went from 35-> 70/80k? I went from literally tapping into debt / line of credit to pay the bills every month and buy food at 35/40k.

Started worrying about house / wealth creation to then that subsided around 200?

Now I’m worried about retirement , what I’d need to support a family / give the kid the life I want. Am in the process of of trying to identify

Toronto / HCOL for reference

Was less about salary and more about overall wealth and cushion - for me was when mortgage was paid off and kids out of college - at that point I was paying bills and saving for retirement. Second inflection point is when you have saved enough for retirement so everything coming in is gravy - but that’s after a loooong career

300K (600K HHI)

For me it was not so much salary as Net Worth and 12 month rainy day fund.

Once my net worth crossed $5M and a 12 month rainy day fund I stopped worrying.

About 300 TC

The city manager makes over 400k lol

https://www.dallasnews.com/opinion/commentary/2020/08/27/mayor-johnson-top-city-of-dallas-salaries-are-bloated-and-its-time-to-defund-the-bureaucracy/?outputType=amp

When TC reached $450k and NW was around $4M

How old are you?

200k in Chicago let me do everything I want and need without a second thought.

Now at 500k and the only difference is more in retirement and I feel like I can keep doing everything I want + afford kids

30M, $200k TC in MCOL city. I can pretty much buy/eat anything and travel anywhere without worrying about my retirement plan taking a hit (800k NW)

I also do not have kids, so net positive there

150k

When I was young, single, and renting: $75K

When I was recently married with a mortgage: HHI of $200K

We’re now planning on 3 kids and making a HHI of $400K which is more than I know what to do with. I feel like we could drop to $275K and I still wouldn’t be worried about money. I’m in LCOL

If I was single with no kids, I'd feel good now at ~230k TC in a MCOL city.

Current HH income is ~$300 with 1 kid and I still stress a bit.

For those saying net worth, how did you get to the net worth that got you to not worry and about how old were you at that point?

Getting to $5M net worth was a slow grind for me. I came to consulting rather late - 38. Divorce, and other setbacks cost me at least 10 years. I didn’t arrive until 52.

Kids are expensive if you want to put them through private school and college.

For me it was just Financial and investing discipline. Keeping overhead low, eliminating debt and grinding. No quick path for me.

The key for me since day 1 working has been all about managing my expenses. Most people increase their expenses as their income increases - leaving them feeling perpetually insecure. For example, when I get a raise or bonus, my first thought is how can I invest this? Or, what loan principal can I pay down? Meanwhile, most folks think in terms of what consumer goods or experiences they can burn it on. If you can resist the never ending temptation to burn your money, you’ll find financial secure pretty quickly no matter what your income numbers are.

TLDR: live well within your means and plan for a future where you make less-to-zero income from a job.