Related Posts

I just turned the heating on. Wtaf. 🥶

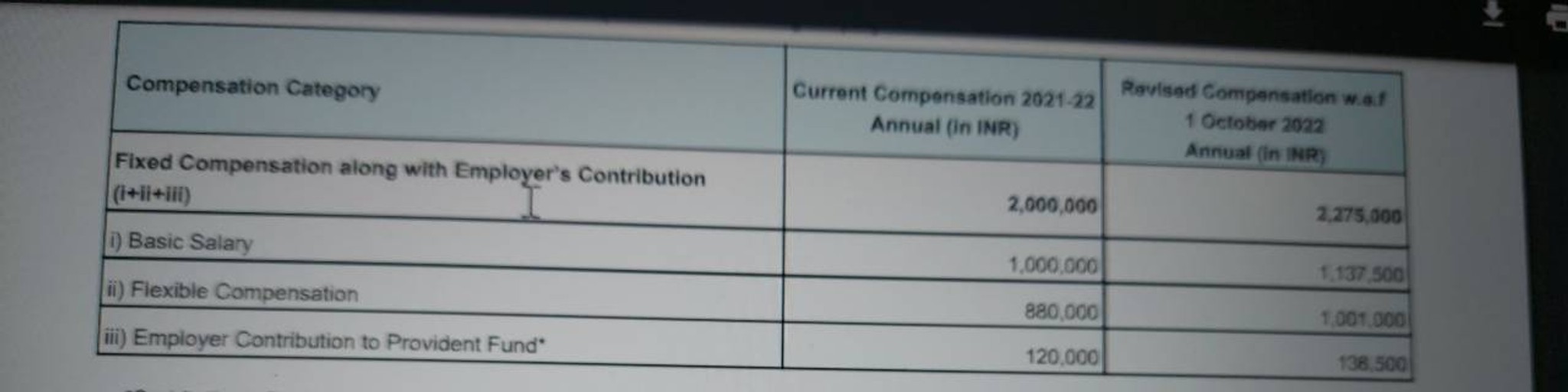

In hand salary?

Additional Posts in The Real Estate Bowl

Subject Expert

Anonymous User

Enthusiast

Visual Storyteller

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

You can afford to buy both of us houses

What does your income picture look like—single income or dual HHI? That distinction really matters when thinking about how much to allocate toward housing.

For context, we’re a dual-income household with no kids. When we bought our NYC co-op two years ago (at 38), our combined income was around $1.1–1.3M, NW $7M. Even so, we intentionally capped our purchase at $1.7M to keep fixed housing costs conservative in case of a job disruption. That decision turned out to be the right one—two years later, I was laid off, and we were still very comfortable covering payments with savings and one income.

Given that you also have significant childcare expenses, I’d argue this logic applies even more strongly. Buying at a level you can comfortably manage through a job loss or unexpected event can make a meaningful difference in long-term financial and personal stability.

Sounds bit ambitious but you know your best situation . Assuming 600k family income and a biweekly pay check of 11-12K (after all deductions - maybe you dont need to max out 401k now). Your monthly payment on 1.5M loan will likely be 10k . Assuming childcare cost at 3k per month per kid, u will be bit tight. Plus you are looking for job certainty for solid next 10 years

It all depends on what monthly payment you can comfortably pay. You have a lot of working years left so now is the time to stretch.

100%. Calculate the monthly payment you are comfortable with, and then include some room for taxes and home care expenses, and of course all the other stuff in your life.

I can help you out and provide with white glove service . Am fully licensed in NY area. LMK if interested

What’s you plan for kids education? Private or public?

We have a similar net worth and income, also two kids in a very high cost of living city. We are considering paying for a $2M house in cash to avoid the mental stress of paying 10-13k monthly mortgage, prop tax, etc. Those funds might be better sitting in the market but we have enough non retirement savings to feel comfortable with it.

We have also considered lower cost towns but we need to be within commuting distance of the city and don’t want to be miserable with 1.5 hr commutes with young kids. And the other consideration is that we want to stay in the home long term, and not buy a smaller starter home and then have to move (potentially school districts) again.

Haha yes same stage of life. My biggest priority now is not uprooting my family again now that the kids are almost in school.

You could also do a big downpayment and then decide later to make extra payments to pay down the mortgage faster. Personally I want the mental freedom of not making those massive payments each month. But if rates were lower and I could arbitrage I would.

Home or apt? In NYC it’s not just about the price of the apt, but the monthly maintenance fees that are higher than the mortgage. For example, maintenance for 2B can be ~4k monthly, on top of mortgage. The larger the apartment the higher the fees. Look on street easy for a breakdown.

Btw, How do you have 1.5M in retirement at D and only 38? Our 401k match was pretty low historically. You must be an experienced hire.

Not touching it though because it grows tax free.

I have found the market to be so competitive in the 1.5-1.7 range, that prices end up bidding close to $1.8-$1.9m anyway. Whereas if you’re willing to spend slightly over $2m (say $2.1-$2.2m) you can get a lot more for a relatively small incremental amount.

Assume it’s double HHI, you both maxed out 401k, your other benefits is about 12k a year, your kids education is 100k, after all that your net after tax (assume highest bracket) is about 200k, internet recommend 28% of monthly net income for mortgage, which gets you around 4700 a month mortgage payment (using average 30yr fixed rate), you can comfortably buy a house worth 1.7mm (with 1mm down payment). That’s a lot of assumption and didn’t count any of your 2mm non-retirement net worth. It also heavily depends on your other monthly expenses.

On paper, $2.5M seem doable based on the information you shared. Depending on other expenses you have, it could get a bit tight. But on the positive side, your income should continue to grow and you still have $1M in savings, which gives you a bit of a cushion in the event one of you loses a job.

Personally, I wouldn’t stretch so far, just because of the “what if’s”, but I am also a one-income household.

Where are you looking?

Yep, we’re all screwed

Generally your wealth is not your 401K.