Related Posts

Who does your taxes? Need a recommend. Thanks.

Conversation Starter

More Posts

Conversation Starter

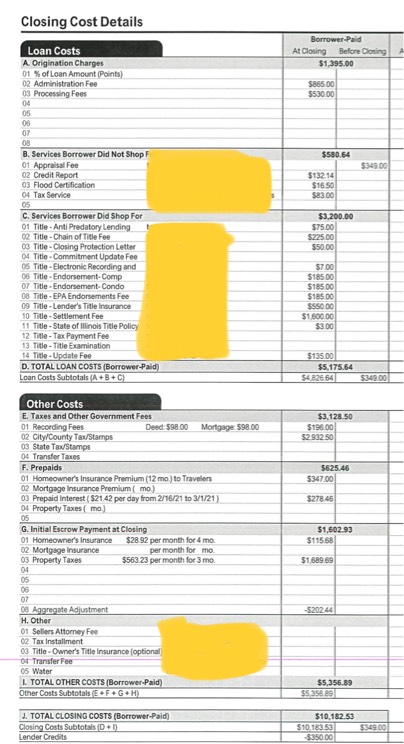

Spot the difference 👀👀

Conversation Starter

Visual Storyteller

“The Sinner” and a Yamazaki & Hakushu flight

Additional Posts in The Real Estate Bowl

Visual Storyteller

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Happy to share my perspective and answer any questions.

Short answer is it depends (unfortunately lol)

We are $450k household, on work visa (that adds some risk) and bought our first house for $1.4M. Daycare starting later this year at $2k as well.

I am more of a calculated risk taker - so the house ticked all our must haves but def comes with a bit of financial stretch but also that there’s no way you can time the future/market. Worst case, we can sell off the house as far as it’s in a desirable community. Living today and making memories with our new born was more imp and hence we pulled the trigger. I am budgeting a bit for this year until the annual bonuses hit, but otherwise, happy with the purchase - house is not something that we change everyday and is something where we spend most of our time of the day.

We’re in a somewhat similar boat at around $380k per year with a baby, and lowered our search from $1.3M to $800-$1M - ended up purchasing around $850k.

As folks here told me in my case, would most likely not recommend what you are proposing (unless you are able/willing to put down 50% or more for the downpayment). Your monthly PITI alone on a 20% downpayment is going to be $10k or more. Your daycare is $2k. Presumably you need at least one car. You might have more kids. You have A LOT of expenses in your future that you might not have budgeted. Even new houses require 1-4% per year in maintenance and significant costs to close and move in. Depending on your state, there may be a mansion tax. Is the $500k base or does it involve variable bonus? What happens if one of you doesn’t get expected bonus or stops working for any reason?

It’s a very personal decision (and we’re in the northeast so totally get how tough the markets are), but we landed on the side that new parents with a baby just don’t need to be stretched financially like that.

I appreciate the reply

Totally relate to this post. We bought 1.6m making closer to 300k HHI 7 years ago with very low interest rates. Was a great decision, our income has doubled and house is now worth 2.3-2.5m. In HCOL I think this is somewhat inevitable, and generally makes sense. However, if I lived in the Midwest for instance I’d likely not have spent nearly as much on a home, bc you likely don’t need to in order to afford a nice home in a nice area. Further, these areas typically are not going to appreciate as much, and better off putting excess income into stocks or other investment.

It’s hard to tell what will happen in this market and very easy to think “how can people afford to pay this much” … but they keep doing it. In our neighborhood the standard keeps raising. People moving now just have to make incrementally more than we did. I also think if interest rates start ticking down, prices will rise a bit faster.

Obviously DTI was close to limit, but we were fine. I put usual 20% down. 3.25% interest rate at the time, so that helped too. It was thru Wells Fargo, so completely standard jumbo financing. I think my mortgage alone was around 5400/mo.