Related Posts

ENBD is the crappiest bank in the UAE. Thank you

Community Builder

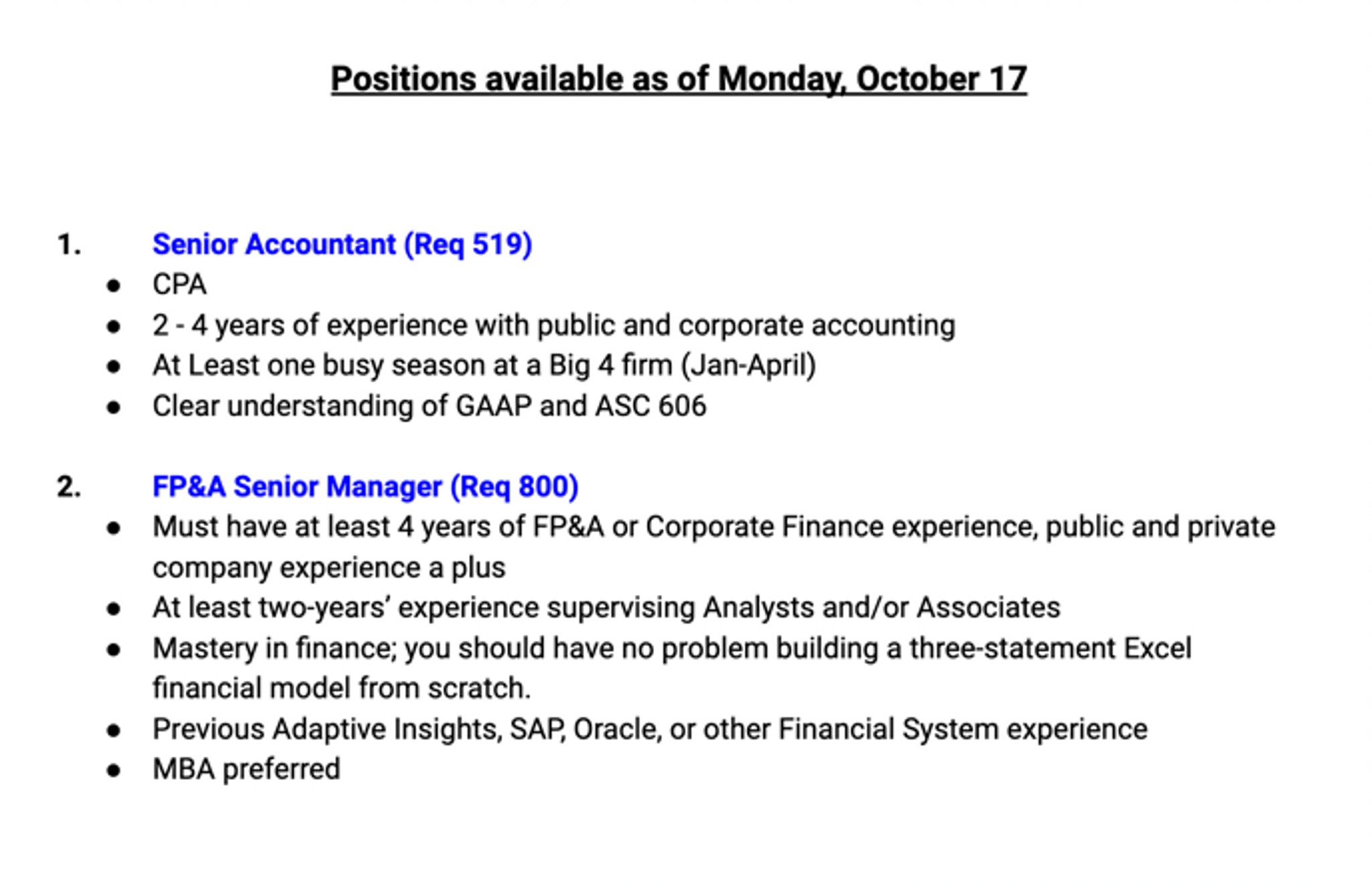

#hiringurgently at °Nomad Health which is a HealthcareTech company that is the first digital marketplace for healthcare jobs, efficiently connecting quality clinicians with rewarding career opportunities. Hiring urgently for these 2 roles listed below, be sure to apply DIRECTLY ONLY through those special referral links listed below:

1.) Senior Accountant- https://grnh.se/907a22374us

2.) FP&A Senior Manager- https://grnh.se/c93c17e14us

More Posts

Conversation Starter

Hi All,

I've an overall 9+ years of experience predominantly into training & development and project management. I worked in ecommerce and supplychain industries. Please let me if there's any suitable opening. I'm about to finish my notice period and ready join by 1st week of July.Amazon Tata Consultancy IBM Newco

Chief

Bowl Leader

Bowl Leader

Community Builder

Just came from a salatul janazah.. 😢 😔 😞

Additional Posts in Stocks

What do you guyz think of PLTR?

Conversation Starter

Conversation Starter

Pro

Thoughts on Transfix? Anyone invested?

Conversation Starter

New to Fishbowl?

unlock all discussions on Fishbowl.

F

A bad time to take money out of a 401k. Seems like you could miss out on upside if the macro environment improves. However putting 20% down feels great and avoid PMI. Also the payment on 401k loan is a payment + interest.

Probably would go with the 401k just to feel more secure and lower monthly mortgage payment.

I believe you still are “cashing out” during the term of the loan and slowly paying back in so you do lose out on potential growth

Do not take out of your 401k when market is down. You can’t buy a house right now if you only have 5% to begin with.

And why can't I buy with 5% down?

M1 is correct. When you take a loan from your 401k, you are cashing out. Your plan administrator will sell a portion of your assets to fund your loan and then you pay yourself back over 5/10 years including the interest. So in today’s environment you could possibly be selling low and then buying high over the next 5/10 years.

I took a 401k advance in 2016 to cover approx. 6-8% I needed to hit the 20% down. Each time the market goes down by 10% I throw in an additional $2k. So I figure I will pay off the 10 year loan in 8 odd years (unless the market goes down significantly over the next 12 months)

I figure with the savings on the PMI + lower interest costs ( 20% down will get you a better rate compared to 5% down) + home equity appreciation I have come out ahead.

Will you stay in the home for a long time? Could you use a rebalancing of your overall portfolio for more housing, less stock?

Those are the two questions you need to ask yourself before making a decision.