Related Posts

bonus letter received?

Hi Guys...

I have a total of 5.5 years of experience with current CTC as 11.5 lpa.

I have a offer from Infosys of 17 lpa

But my company wants to retain me and they are giving me an opportunity for Canada onsite in return of retention(no raise or bonus)

Please suggest me, if i should take the onsite opportunity or keep looking for counter on my current offer.

I have 70 days of Notice Period left.

Tech stack- python/ AWS/ data engineeringDeloitte

More Posts

Bowl Leader

Has anyone used eharmony? Yay or nay?

Bowl Leader

Sea of thieves anyone?

Additional Posts in Offer Negotiations

Hi fellow fishies!

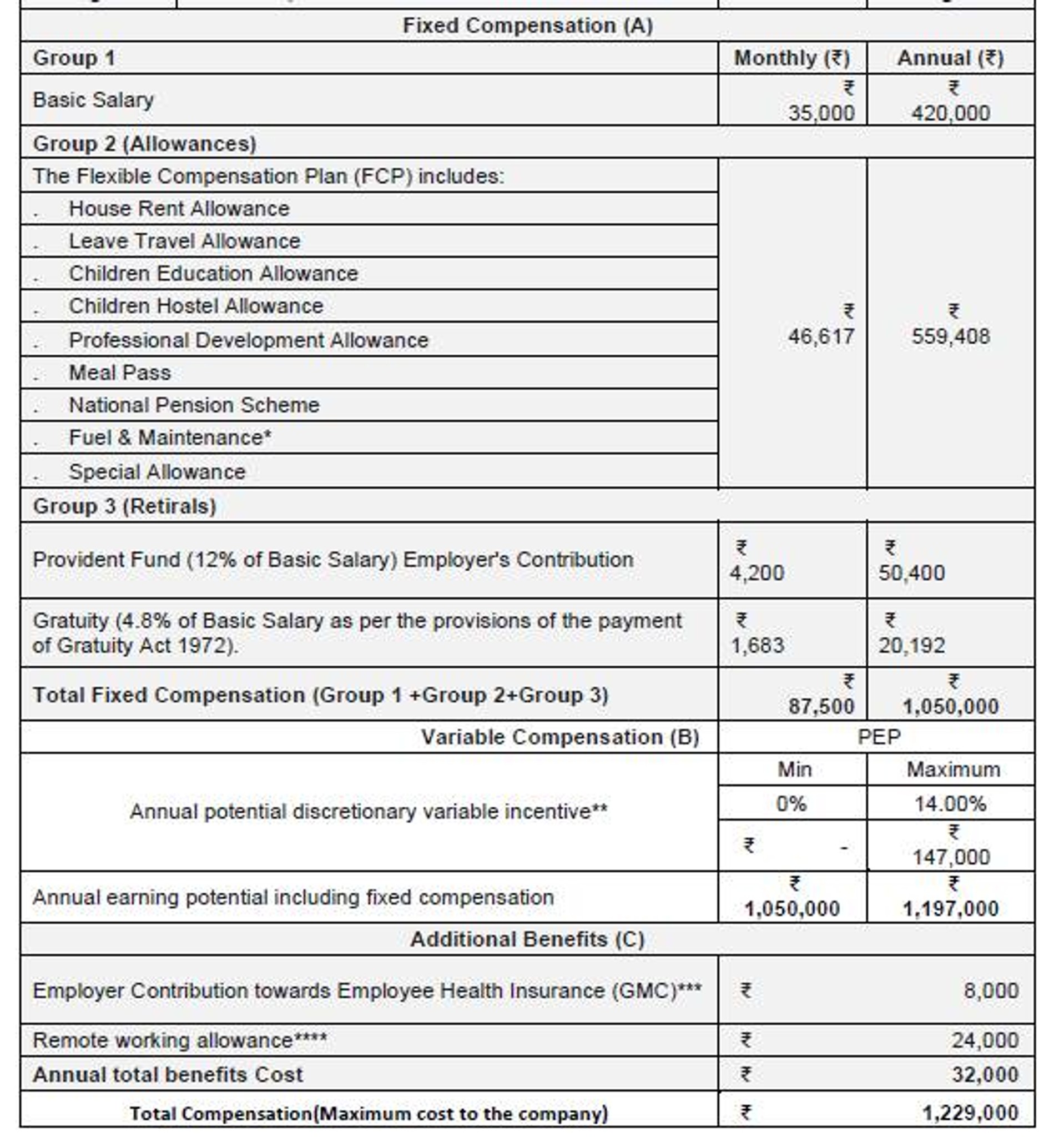

Can someone please explain what is “SUPPLEMENTARY allowance” in my payslip??? It is the highest in my entire payslip, more than basic salary. Basic is lets say ₹7 lac annually and supplementary bonus is ₹7 lac 40 thousand.

Can someone please explain why this exists in my paylslip, is it good or bad from tax perspective and shall I ask my HR to decrease it???

Please help asap.

Opus Consulting

I have 12+ yoe. I work in AWS with a 23L base, 13L JB and 5 RSU (29.8L ), L4. I am about to receive an offer from ADP . What band/grade would be great to negotiate. For ADP anything around 45L-48L including 12% variable (not sure about JB) is considered to be the right offer? I have another offer from Accenture 32L fixed, 10L variable, 6.4L JB. I guess wlb in Accenture would be more difficult than ADB?? What's your view fishes !!! Consider AWS and ADP in Hyderabad where Accenture in home town

Hello.. i have 6 years of experience in frontend development. I have offer of 27.5 from Nagarro (client to be decided yet) and 30 from HCL Technologies (apple client and work location also apple) and 26 from Netcracker Technology Corp. maybe with some joining bonus. Which do you think I should join.

How long it take for L1 round in Capgemini.

New to Fishbowl?

unlock all discussions on Fishbowl.

Saving : 2.5 cr

Age :34

All money invested in land

CTC: 20 lpa

I don't plan to save any money in fd and all, all I do is invest in land. Believe me that's the best investment.

Any suggestions how to achieve 1cr savings with 15 lpa

How did you save 80 lakhs in 30 yrs. What is your package journey in these 9 yrs curious to know

Started with 3, then switched to 7 then 10 then 14 then 24 then 35 then 41 now current.

Ideally invest in good property in your near by locality.If you can buy commercial property in better rates compared to flat.

Post that you can easily invest some money in good mutual funds do take professional help if you can or if you know use your learning

Keep 1 year salary in fixed deposit

Now for remaining amount as mentioned invest in some stocks and invest something every yearly in ppf also as it will help you in diversification.

Thanks

Rising Star

What's your end goal? It can be your retirement, kids marriage or education, a vacation etc. If it's retirement in how many years are you planning to retire? Based on your goals time duration you can go with either equities or debt funds or a combination of both. You mostly would be married so make sure you have enough to support your child's education and marriage even after achieving FIRE (Financial independence retirement early).

I hope you have a term plan, health insurance and emergency funds to support you. Also try posting this in Asan Ideas for Wealth FB group where there's a ton of financial information available.

In your case I would strongly suggest you to consult with a SEBI certified fee based financial advisor. They can help you with providing a clear cut idea about the different instruments available for investment based on your risk appetite, portfolio allocation, rebalancing etc. You contact any of them, have a connect with them and choose anyone based on your preferences. You can find them here (www.feeonlyindia.com). Also do understand that free advice in any platform is a big risk and you should do your due diligence before trying out anything new.

Rising Star

You can find the fee only advisors here www.feeonlyindia.com. you can choose anyone based on your preferences, connect with them and go with who ever you feel comfortable with.

first of all, congrats on having good savings.

Now, along with regular expenses, you'll also have occasional expenses like vacation, expensive purchase, kid's higher education/ marriage, etc.

I assume that you don't want to actively track your investments after retirement, so you'll need to have it in debt instruments like fd.

I'll suggest building some rental income as well, like buying a small shop or house and renting it out.

You can later sell it for kid's education or marriage if you need to.

Assuming that fd gives minimum 4 percent returns, I guess you need to have at least 5cr to be completely on the safe side, i.e. 3 times your current expenses.

Also, you must be having some inheritance, which will provide further cushion.

That's my suggestion, or you can say somewhat my plan as well for my future, as I'm 33 and have 2 kids, savings and investments are little higher but that's due to family business. I plan to retire with at least 2 lakhs per month rental income or 10cr in debt funds as we're a joint family.

Rising Star

Post tax it'll be closer to 5.3, so not too far from 4😅

I run a PMS you can invest in that ROI 40% per annum

Don't listen to traditional advice with poor asset allocation strategy such as heavily buying land/flat/physical gold/LIC policies, etc. Write down your financial goals, the number of years you are away from them and the amount that you want to achieve when the term ends. These can be short term things like buying a MacBook or going on a vacation to Europe or medium term things like buying your dream car or long term things like kid's higher education and your own retirement. Then do asset allocation. For short term goals, 100% in debt. For medium ter goals, 10% in gold (go for etfs or gold bonds), 40% in equities (mutual funds are fine, no need to invest in direct stocks), and the rest 50% in debt. For long term goals, 65% in Indian equities (mutual funds), 10% in US equities (use INDmoney and buy Vanguard S&P ETF which is like the oldest index-based ETF in the US), 15% in debt, 5% in gold and another 5% in alternative assets such as REITs or crypto.

Namak chawal kha ke jinda ho kya bhai

It is very much possible to save 80 lacs at the age of 31.

Pro

Q: Where do you want to see yourself in 5 yrs.

Me: Same as Senior Software Engineer. 😎

(Just for laughs)

BTW, good work bro. ✌🏻

You need 25 times annual expenses as retirement corpus.

25*6L=1.8 cr

The goal is to invest in some asset class which gives atleast 8% returns an year, you withdraw 4-5% and reinvest the rest.

Invest in land buy some plot in good area where there is a scope of development. it will give 10x or 20x in some years

Not financial advice but it is recommended you:

1. Keep 6 months salary in an FD as emergency fund.

2. Then you max out your 80C - PPF, EPF etc.

3. Then have invest in Mutual funds (debt & equity) based on your time horizon. The longer the time, more equity you should keep. If you want least stress just do an SIP (not lunpsum) in any Index fund and don't overcomplicate it. (Can read about this in India Investments sub-reddit)

4. Invest in land.

I have seen a corrupt govt employee buying a plot building a triplex house with 9 individual houses for rent. Now he is earning money from 9 rented houses. He has his own apartment in neighbouring to ours.

That is what the problem bro. We are not able to compete with property prices because of these corrupt people. This is why property prices are sky rocketing. These guys throwing money like anything. They buy property at any price since it's not their money

Keep it in FDs. I assume you haven't bought a house yet which is why you have this amount? Keep it in FDs if you want to build your retirement corpus first. Apply the rule of 72 - i.e money at 8% a year interest doubles every nine years (8x9). Current interest rate is 6% so money will double every 12 yrs. I guess going by this logic, you will need another 20 lakhs to secure your retirement so that by the time you are 50, you should have ~3 cr. And at 6% interest, 3cr gives you 18 lakhs per year which should take care of day to day expenses post retirement.

The remaining amount then you can start saving for various other goals like emergency funds, kids education, travel, exigencies etc and you can increase your risk appetite by investing it in a combination of debt and equity MFs and some amount in stocks. Hope this helps

Sab fake hai kuch bhi

9saal me 80lakh

Koi ka to 25 lakh bhi ekatta nahi ho paraha hai

Feku ask

Hmm, sab fake h. True!

Saving 2 lakh turning 30 next week

But wait I did have explored every single sort of state and city of India with kids and husband living a whole life with everything happening so spontaneously just living my whole.

Adding to same our kids is in b grade schools for now learning so well and we are planning to work until 60 retire at 60 with good corpus considering pf some recurring mutual funds and NPS with that’s one more thing that’s a well stable kids with good parenting and spending as much with them until they won’t start their own😍.

Noice

Send me little of it please

Pro

Another bhikari

What is ur ctc?

Which company are you working ? Your role ?

This is awesome man. Would suggest you to diversify this amount for good returns.

Invest in yourself, try your luck in a top US or europe uni for an MBA or masters if you’re game for it. You have time on your hand and investment in oneself is the best at this stage of life .

Not a great suggestion

Pro

Your native??

Yes, in Hyderabad you can find these type of investments in low budget.. but be careful n be cautious when investing

Start with a blue chip MF with sip… if you don’t have knowledge about stocks it is best to start with MF as there are fund managers to do that really well.

Eventually start getting into stock trading with little money, get an account opened for stock trading and you will learn !

Another desi option is buy gold / property. !