Related Posts

Community Builder

If you have cash that you want to invest. Please consider Treasury Series I Savings Bond (Electronic). Interest is 7.12% right now. While it's not guaranteed that the 7.12% will remain until next year, it's still a good deal.

My SO and I just invested 20k (10k max per person even married).

https://www.treasurydirect.gov/indiv/products/prod_ibonds_glance.htm

Visual Storyteller

Chief

More Posts

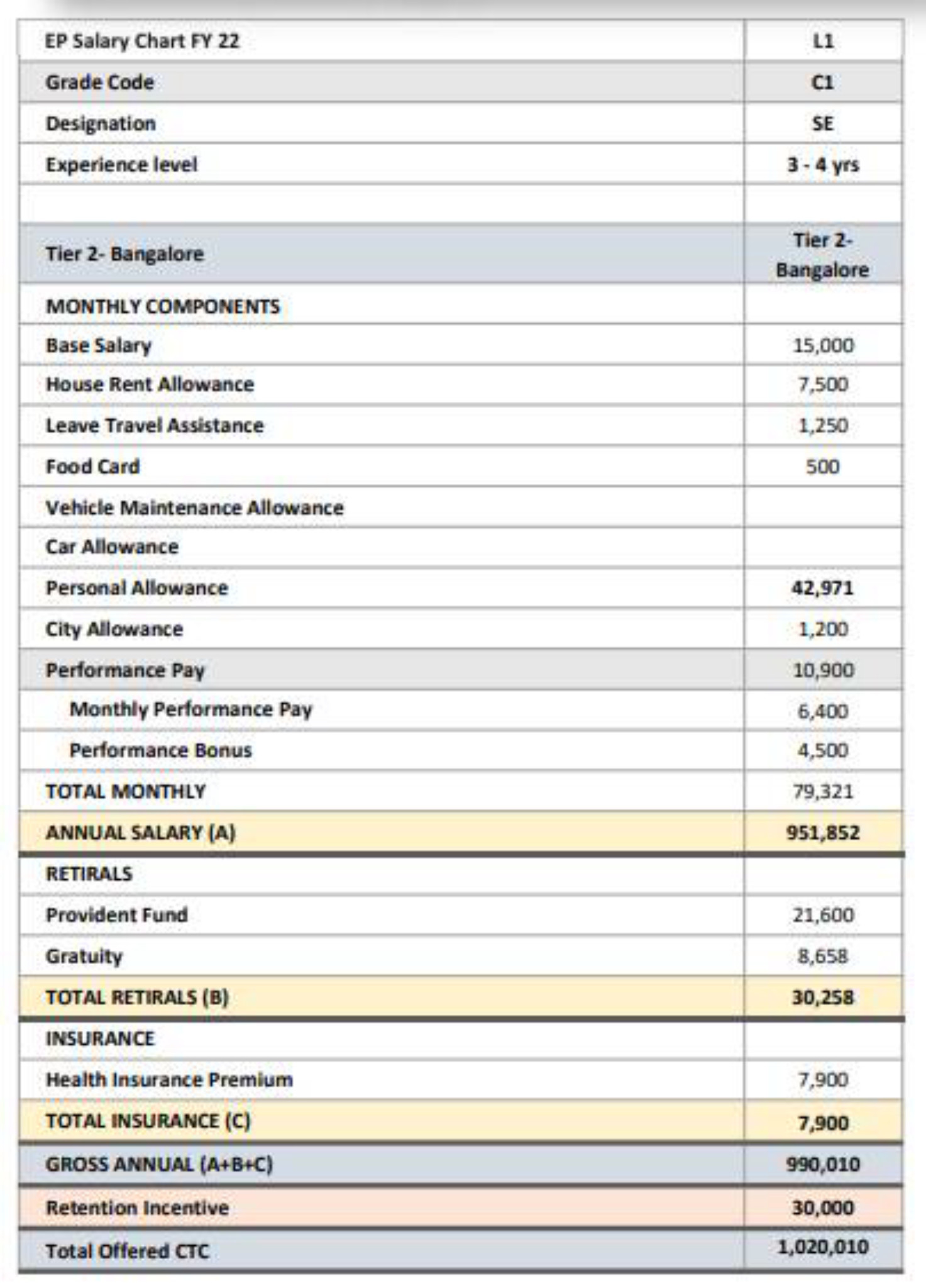

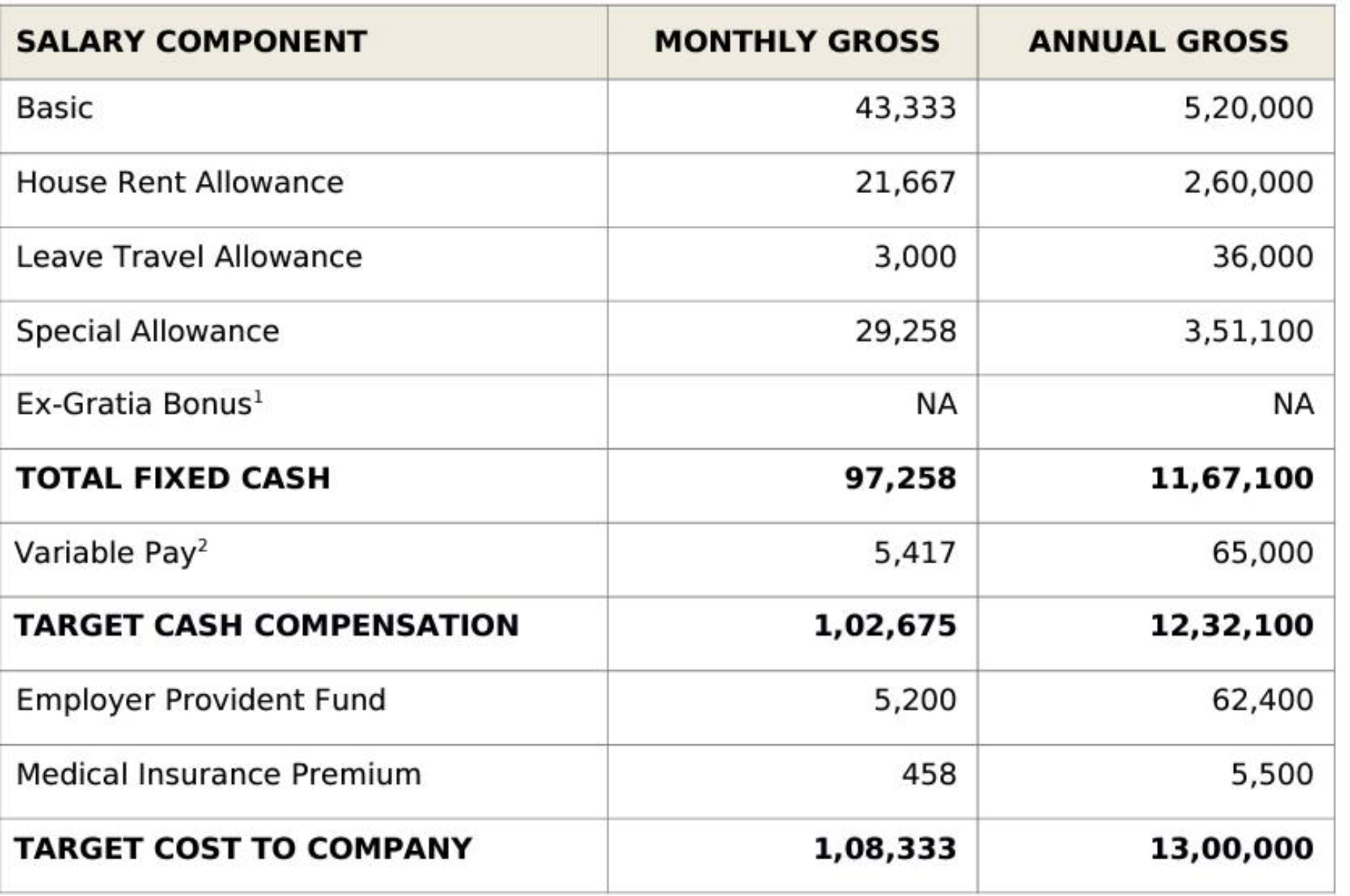

What will be the in-hand for this offer?

Which LOB is good for JPMC Bangalore location ?

Hi guys,

Need 11 likes to access dm's

Thank you

Any know of any tech transactions opps?

Community Builder

Anyone up ? 😉

Additional Posts in Personal Investment Chatter

Conversation Starter

Pro

Pro

Conversation Starter

Enthusiast

SCARED MONEY DONT MAKE MONEY. BUY NOK 🚀🚀🚀🚀🚀

Conversation Starter

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

My husband and I usually save about 50-60% of our income(after tax). Most of that is getting saved for a down payment. We both have a set $$ amount each month(less then 100) that we can spend on whatever we want or we can save it if we want to buy something more expensive. For bigger items like electronics, we discussed if it is worth it and necessary. 10% of our income is charitable giving. The rest is for other necessities. We don’t have any kids yet. What we do isn’t possible for everyone and might not always be possible for us. So for us, 30% is way above what I feel comfortable spending each month on flexible spending.

What kinds of things are in your flexible spending budget.

We want a Costco membership, can’t wait to have kids for that! Yea wow NJ groceries are a lot more :(

Rising Star

I’m 27/50/23. Single so don’t have to worry about a SO but do spend a decent amount on dates, travel to visit friends/family and going out with friends. 25 year old making around 110k in Chicago. Don’t own a car and live with roommates so I can have low fixed costs and a bigger miscellaneous fund. Monthly breakdown:

6500 income after taxes

1750 (rent, utilities and groceries)

1500 (fun/travel)

600 (savings account)

2650 (ETFs/stocks)

The missing 6% is in savings

Bowl Leader

What is the 50/20/30 rule to you?

I had heard of it as a general guideline of try not to commit over 50% to needs and fixed costs, save at least 20%, and that leaves about 30% for wants. By that measure you are doing fine. Do you consider the 20% to just be retirement savings or why isn't that 26% for you?

If it’s including retirement, saving only 20% net seems kind of low. It’s not that bad but I wouldn’t hold it up as an ideal.

Bowl Leader

Here is a similar chart from Ramit Sethi's book I will teach you to be rich. This also uses after tax net income. It's basically the same system with the emphasis on not getting overwhelmed by feeling you need to create and stick to a perfect budget, but rather start with a simple "conscious spending plan" and improve over time.

Thank you

It’s more of a concern that my flexible spending is higher than it should be. We want to get a house and we can clearly pay more than what we are renting since we’re way under the 50%. But that would have to come out of the flexible spending. My wife says no ones has flexible spending within 30%

No I’m more obsessed about the spreadsheets haha. She’s a high spender. I like your outline scenario, thanks!!

Rising Star

We keep fixed as low as possible - e.g., mortgage is $1,650/month but our income has been over $150k since 2015 and last two years over $250k.

Let’s us bump up the other two significantly.

At the end of the day, it’s a tradeoff between present you and future you.

See chart below - couldn’t find the better version that has a curve accounting for compounding savings/investments.

Rising Star

This is just an abstraction to help think about consumption and saving between present and future.