Related Posts

Conversation Starter

More Posts

You talking to me?

Can anyone at Amex share my resume in their team to directly start the rounds of interview? I have tried for referrals through linkedIn and did not recieve any call from the HR.

29th Apr is my last working day in my current organization.

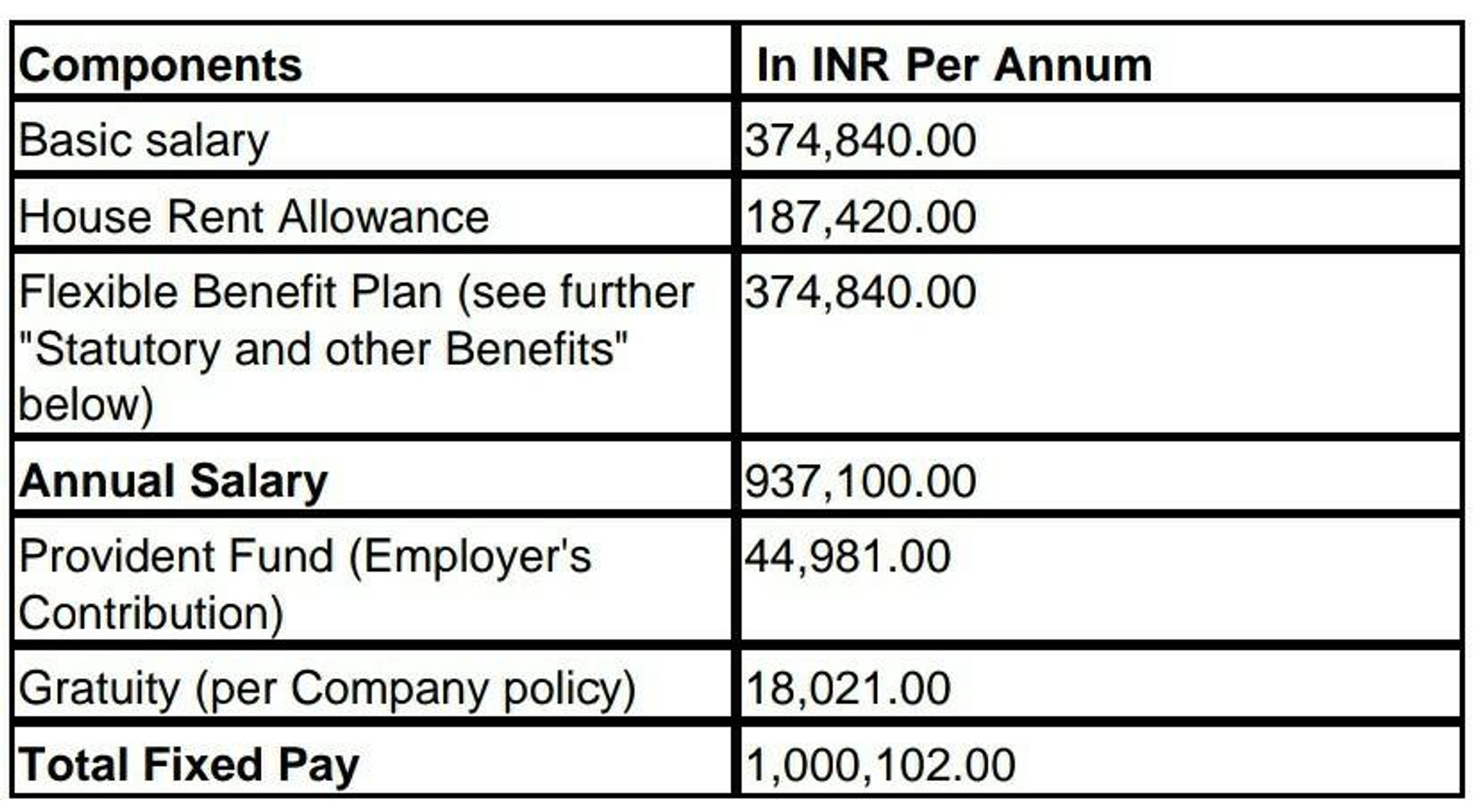

Tech stack: SQL, Tableau, Python, Excel, Powerpoint with more than 4 years of experience. Currently have an offer of 23 LPA fixed. Fixed anything above this or equal to would work. American Express American Express India Campus American Express Global Business Travel

Additional Posts in Financial Advisors

What specific tasks do your Assistants do?

Has anyone used Smart Asset for lead generation?

My Week in Emoji: ⏰☎️🧹🚽☕️📥🧾💤 Hbu?

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

And also avoiding market corrections doesn’t only work until the market recovers and it’s never a dumb move for someone close to or in retirement. Ever looked at a sequence of returns chart? If you take losses right before or early in retirement when you are about to start drawing from your accounts, you can run out of money very early on, even if markets start to recover afterwards. Hence why once you get older it’s much more important if you want your portfolio to last as long as you do, to avoid the major losses versus capturing the major gains.

Garbage. Do exactly what ej1 said. Also mention to them whoever sold that crap to the client needs to be shot.

Well if you guys weren’t complete idiots you’d know a couple of things. One that’s Not a VA so don’t say it has an income option similar to a VA. It’s an indexed annuity and it has an income option similar too.....an indexed annuity. Would be the same as if someone had a VA and you referred to it as having an income benefit similar to a FIA, just sounds like you don’t know your head from your ass with different products in our industry. Second if the client purchased it in 2007, it looks to be from the very little google searching I did an 11 year surrender charge product, which would mean in 2018 it is fully out of surrender and client can do whatever they want with account value. Third since it was purchased in 2007 I would be curious what caps and participation rates on it are since generally rates were much better then. Fourth if client purchased it then, it would mean those funds avoided all of the downside of 2008 which I would view as a plus because who knows if that client would have stayed invested all the way through 2008 to now if he saw his money drop 38%. May have gone to and sat in cash instead. Lastly asking if anyone on here knows what the cap is might be the most ignorant question ever and shows you have absolutely no knowledge whatsoever of how different products in our industry work, unless it’s a mutual fund sold specifically by American funds because you are Edward Jones. Caps and spreads on every contract for any indexed annuity company change as interest rates change. Therefore contracts issued back in 2007 will have different caps/spreads than contracts issued today. Guess what the easiest way to find out what they are is......actually do your job and call the freaking company with the client on the phone and ask them. While your at it maybe ask them what their income benefit has grown to since you say it has one on there and be sure you aren’t making a massive mistake by recommending a client surrender an indexed annuity that could have a huge income benefit on it at this point if he bought it in 2007 and had guaranteed growth to the income base for the last 11 years. Literally amazes me how little some of you know.

......unless the client bought it with the income rider to use it for.....you guessed it, income! Maybe the more relevant question before you tell another advisor to recommend to a client they surrender it would be to say what is the income base at now and what would the clients lifetime payout options be? Will the income base continue to grow or has is reached its guaranteed growth level already if there is one. All more relevant things to look at than saying “caps and par rates suck have him surrender"

Lifetime income option similar to a VA. Caps and participation rate suck. Have them set it up for maximum surender free and slowly liquidate it if it is still under surrender. Make sure to add third party auth form to bypass the selling agent.

What is the contracts purpose? Income? Growth? I’d check the fees before doing anything. VA fees are high and in an income situation very doubtful the contract gets raises most years.

Thanks. He bought it because he was nervous about the market. Client is now 62, purchased in 2007.

Does anyone know what the cap is?

Dude....don’t talk to the agent, but call the companies main number and yes the client will have to be on the phone and they will give you whatever info you want. But yeah def do not make a recommendation to the client without doing that

FA2... watch your mouth. I know how these products work and their income rider works similar to a VA as it has a income base and a guaranteed payout. Easiest way to explain it without knowing date purchased. Also, comparing Athene’s caps and participation rates to other FIA they are definitely on the low end. Lastly, even though they avoided the crash of 2008-2009 that only looks good once you get through 2011. Avoiding market corrections only works until the market recovers. From there, it’s a dumb move.

Thanks guys, I didn't mean to start a firestorm, just needed some information before I met with the client. I was trying to get information without talking to the agent.

Idk if you could find the prospectus online, but that's an option too. I will say, my last thought is to hop on fishbowl and see if we know about an annuity.

Yes Mr. client this annuity is terrible, because a random person on an advisor forum said so lol