Related Posts

Does LTI provide reimbursement for WFH setup ?

Pro

Community Builder

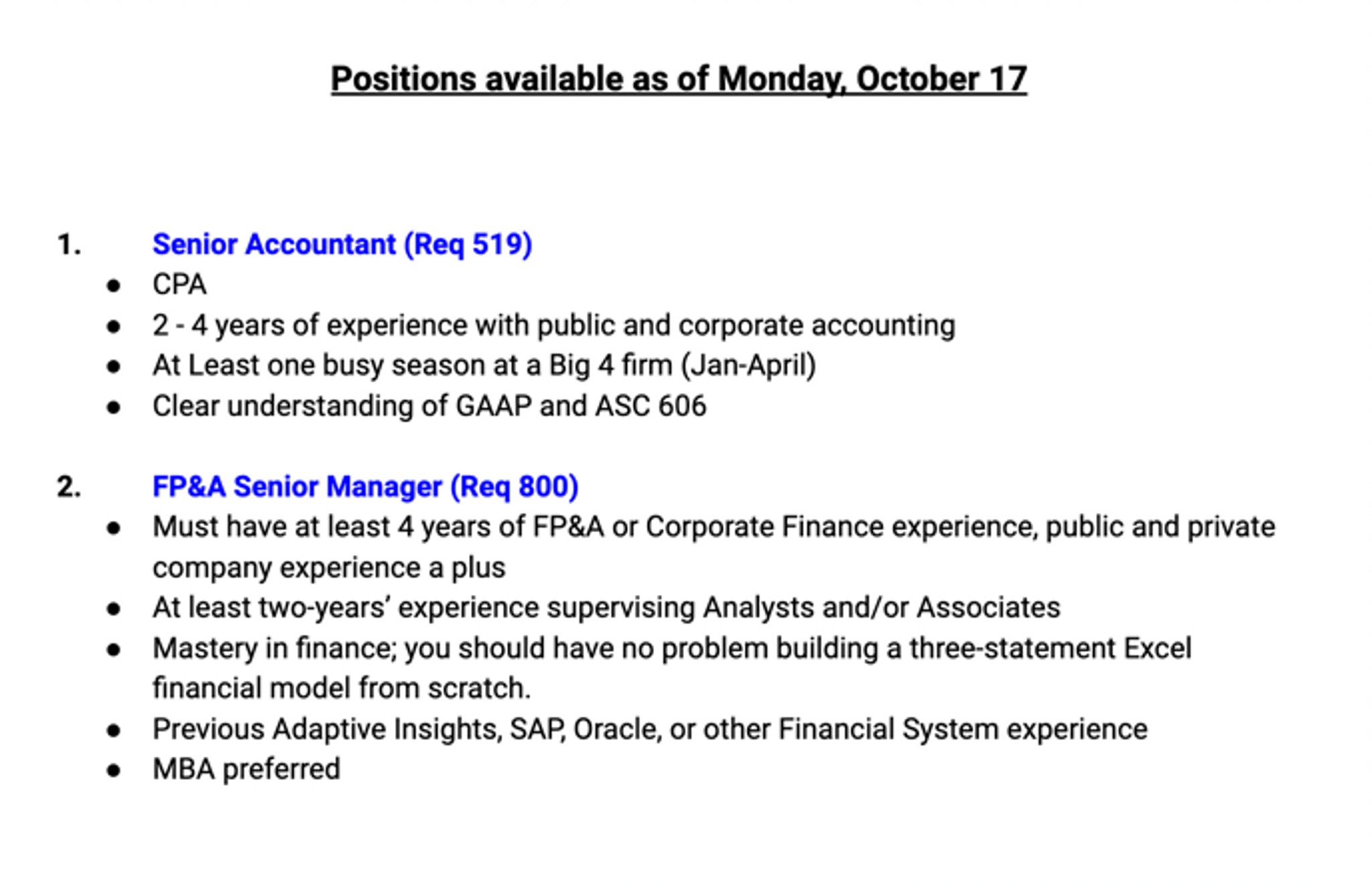

#hiringurgently at °Nomad Health which is a HealthcareTech company that is the first digital marketplace for healthcare jobs, efficiently connecting quality clinicians with rewarding career opportunities. Hiring urgently for these 2 roles listed below, be sure to apply DIRECTLY ONLY through those special referral links listed below:

1.) Senior Accountant- https://grnh.se/907a22374us

2.) FP&A Senior Manager- https://grnh.se/c93c17e14us

BDO India Hello fellow consultants, i have been offered a package of 66K GBP from Deloitte for the position of Manager - Cyber Internal Audit, Financial Services, Risk Advisory - Manchester. I am currently working for BDO India and will be relocating, what are your views on this? What are the extra relocation and accomodation benefits i can ask for? I am a 24 year old bachelor and i have 3 YoE. BDO Deloitte India Deloitte USI BDO RISE Private Limited

More Posts

Is there a United status challenge?

Additional Posts in FIRE Financial Independence Retire Early

Sooo AMC.. who’s in?

😂

New to Fishbowl?

unlock all discussions on Fishbowl.

The problem is in my mind SS benefits aren’t guaranteed in the future at the current promised amounts. I’m in my 40s- who knows what will happen by the time I’m 67 or 70. I don’t think it will completely go away but could only be 50% or 75% of what it says now.

There’s definitely a push to cut benefits by the current admin’s party. I would not count on it being anywhere near the same level in 20+ years.

If I summarize the significance of this revelation about the Social security, my FIRE NEEDS significantly adjusted down - from $5M to $3+Social security.

But that doesn’t mean that I will change my WANTS.

In total, this thought is relaxing. 😎

I don't.

I agree with AVP that it’s more certain then stock market. I also agree with guidehouse 1, I consider SS benefit in retirement a nice to have, not a determining factor in retirement calculation

I would just look at it as icing on the cake, assuming it’s much at all.

@EY1 - it’s funny that I asked ChatGPT after responding and it gave me exactly the same number.

“If a couple receives $40k each per year (~$80k total) starting in their mid-60s:

• $80k ÷ 0.04 = ~$2 million equivalent portfolio”

It seems that AI is reading what I am writing 😄

Subject Expert

I look at it a few different ways.

I use projection lab, which projects out income, expenses, investment returns by year.

It will let you predict SS income by year, calculate taxes, etc

Very useful way to visualize

I also calculate the value of social security as if it were an annuity, and add it to my assets. (Thats not my normal view, but it’s very helpful as an additional view).

$1m per person seems reasonable from your example. But I’d only accrue it as I go. For example if you’ve worked 10 years, you might accrue $500k.

You can get the exact number from SS, but of course they might change

Yes, social security could be cut somewhat, but there’s virtually zero chance it goes away entirely.

Ignoring it entirely means you are working longer than you need / or spending less than you could.

You would just include your assumed calculated amount (80k/yr) as another expected income stream on the side of your other planned income beginning in the year you are planning to begin pulling. I actually forgot to include this in our plan too. It might allow you to retire earlier if you have conviction it will not fall apart and you have other assets to pull from in early retirement. If anything a safety net waiting when you hit withdrawal age.

Yeah, I don’t. So basically, it is upside. May stop working well before it kicks in, so not factoring it relative to annual draws / spend, uncertainty. Basically it is cushion / upside.

Subject Expert

I am young, so I am currently not planning for it explicitly.

People who do plan for it explicitly often do so like this:

Assume that social security will be there for them.

Add a TIPS ladder to pay the same benefit from retirement age until they claim Social Security at (usually) 70.

Subtract the cost of said TIPS ladder from the portfolio.

Calculate a WR using only the remaining balance (after subtracting the TIPS ladder) and the residual expenses (after subtracting those covered by Social Security and the TIPS ladder).

This method works quite well, in my view.

When I was young, I tried to forecast everything. Now I count only investable assets minus debt (I have none). I don’t count real estate (2 homes) or anything else. I count only what is in my control that will produce income.

I am counting on my 401k + pension + SS for retirement after 65. I will retire before 65 once my brokerage account reaches $4M, then 5% withdrawal rate, hopefully sometime between 45-50 yo

You do know that US Social Security is on track to bankrupt in 6 years, right?

Coach

I’m not sure if there is any basis of that. Every year, the working population is contributing 12.5%. It will lead to 2 possible situations

- either the contribution will adjust up, if any pressure on the SS funds

- or some benefits will adjust down.

Bankruptcy is not an option for the Social Security program. That’s just a baseless doomsday scenario.