Related Posts

More Posts

Hi Fishies, I was hired for wealth and asset management project EY . It is capital market domain. Any body have any idea about this project going on in EY and the tools used for it.

Please advise if anyone have idea about it.

Just want to know any global tool they use for wealth and asset management, so it's a plus for me to join.

Thanks in advance

Pro

Conversation Starter

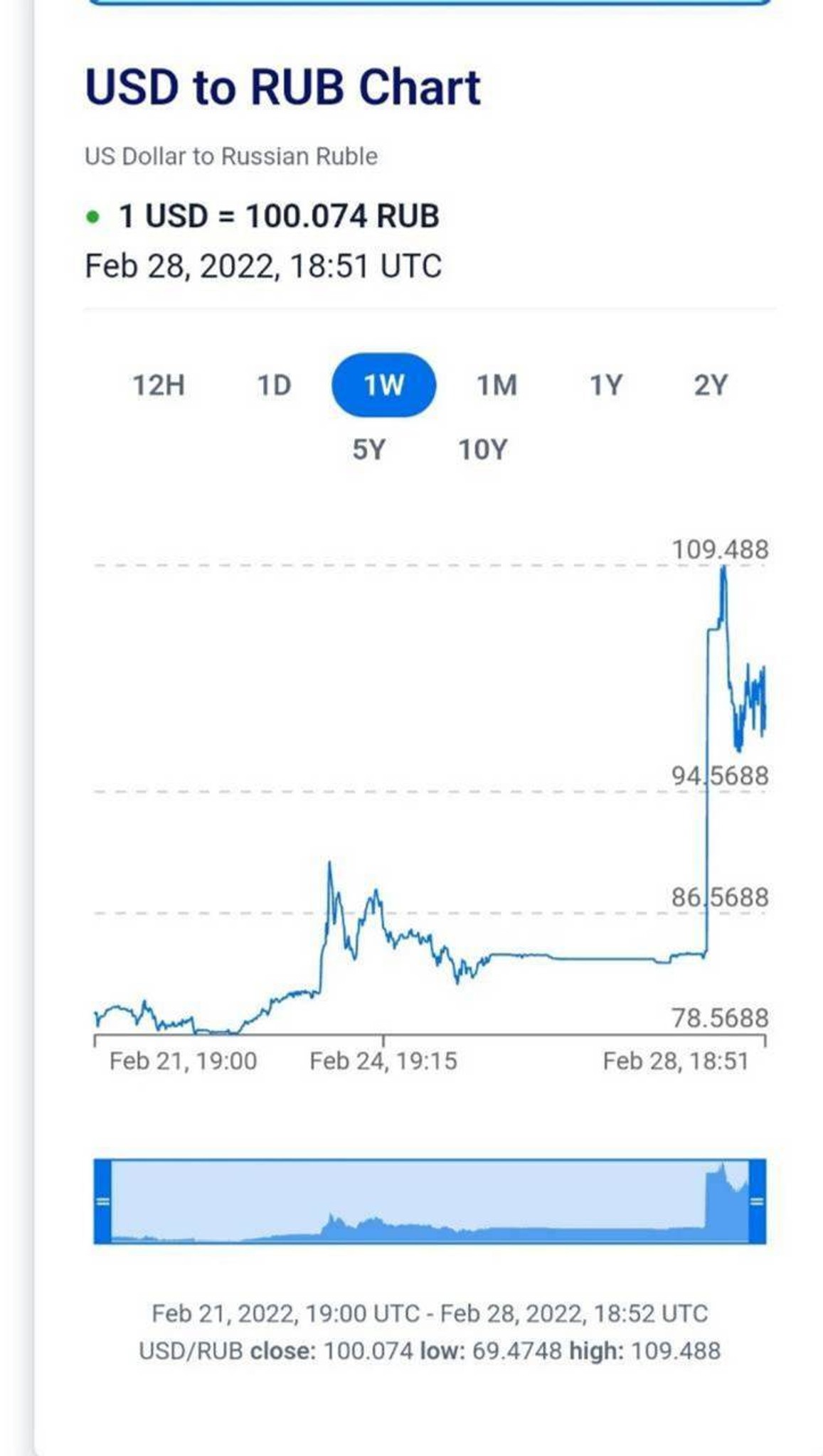

Forwarded from a friend, is this true?Barclays

Bowl Leader

Rising Star

Bowl Leader

Let’s do another ASL 32FChi

Additional Posts in Financial Advisors

Best music/audio to listen to while working?

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

72t rules

Don't roll that 401k to an IRA.... in a 401k he often has options for beginning distribution without penalty. But in an IRA he has will be limited to the T72 plans. Also remember it is when he turns 59 1/2 not the year he turns 59 1/2.

Don’t blame it on the firm unless they close you in a room with no internet access

Are the a public servants by chance in firefighter or cop they can take out of 401ks and 403bs at 55 no penalty as l9ng as they don't do a rollover

Leave assets in your 401k plan, tax laws allow you to withdraw funds from your 401k plan if you retire after turning (or the year you turn) 55. Once you rollover the funds into an IRA - it resets the 59.5yr old distribution restrictions. Anything withdrawn from an IRA would be taxes and penalized. Pension - you’re fine start receiving the funds.

Agree w/ vp1, fa2, it is on you to learn our profession. Go to conferences, get your cfp, read industry pubs (love Kitces), but it is your job, not your firm’s, to get educated. That being said, always learning new stuff and at least you are learning here!

Omg I didn't know that 401k rule and I know I should. I need to get to a different firm where my learning isn't peaked

72t

Leave whatever he will need in distributions and a 20% or so cushion. Roll the rest. That way you can begin managing the assets he does not need. Allocate the 401k conservative. Allocate his rollover to his risk tolerance. You now have a 5 year plus time frame on the rollover.

It’s already been said, but agree with those that say don’t roll the 401k. IRS allows at age 55 (must be terminated from service) to withdraw w/o penalty. One note to add, just an FYI, it only applies to the 401k at the last employer. So, for example, someone has a 401k from old “employer A"; is currently working for and participating in 401k of “employer B” and terminates service at age 55. Person can only access 401k from employer B penalty free. Now, this could be overcome by rolling 401k “A” into 401k “B” before termination from service of employer B (and assuming that B’s 401k plan allows incoming rollovers).

As for getting paid on outside 401k assets, become an independent RIA and you can do just that. 😉

So rule of 55? Does that apply to the pension as well as the 401k?

Your pension, with provisions for early retirement (ex: 55 and 10 yrs of service) all lead back to the same conceptual idea as the 401k. If you take the ‘pension’ or stream of income, you’re fine. If you take the lump-sum option and roll it into an IRA, the 59.5 10% penalty would be back in the picture. Always check with your tax advisor before making a final decision on something of this magnitude. Do it correctly as to not make a costly mistake. I’ve seen people who retired at 54 thus didn’t qualify for the aforementioned rules we’re discussing.

So do I just Google random stuff? I don't know what I don't know so I don't know what Im missing that I need to be learning

Tax rules might allow for 55 but do all plan rules allow it?? I'm curious....

The IRS allows it but you have to pay attention to the rules... retire at 55 ect... the only way a plan doesn't allow it is one who only allows lump sum withdrawals...

72T rule. And yeah, dedicate some time each week to educating yourself. If you don’t have your CFP designation, get it. At the very least read trade publications with a focus on planning issues. It’s part of being a professional. You don’t know what you don’t know and your clients will suffer as a result.

http://www.gcbaonline.com/retirement/understanding-irs-72t-withdraws-rule-calculator

@President - to further clarify my earlier post. Age 55 rule is an IRS rule. You never owe the Recordkeeper or your plan provider the 10% penalty. You receive a 1099r tax form in the year you take the distribution (lump sum or partial makes no difference.) The 10% penalty is due to the IRS - if you are age 55 or over in the year for which you retire from the company who’s plan you withdraw your balance from - you can avoid the 10% penalty (again, between you and the IRS.) This is not open for an individual plans’ interpretation - as the 10% penalty is between the person taking the distribution and the IRS.

Lincoln i4life. Keep control of the asset while getting annutization like payouts and staying invested in the market

Also depending on withdrawal desires,assuming you don’t want early withdrawals and you really don’t need income at 59 1/2, use a qlac to eliminate some of the RMD requirements