Related Posts

Bowl Leader

More Posts

How's the wlb here?

Q is JFK Jr. and Trump is still President!!

Conversation Starter

Why are some people not into feet?

Visual Storyteller

Conversation Starter

Bowl Leader

Which one u choose for better productivity

Additional Posts in Personal Investment Chatter

Rising Star

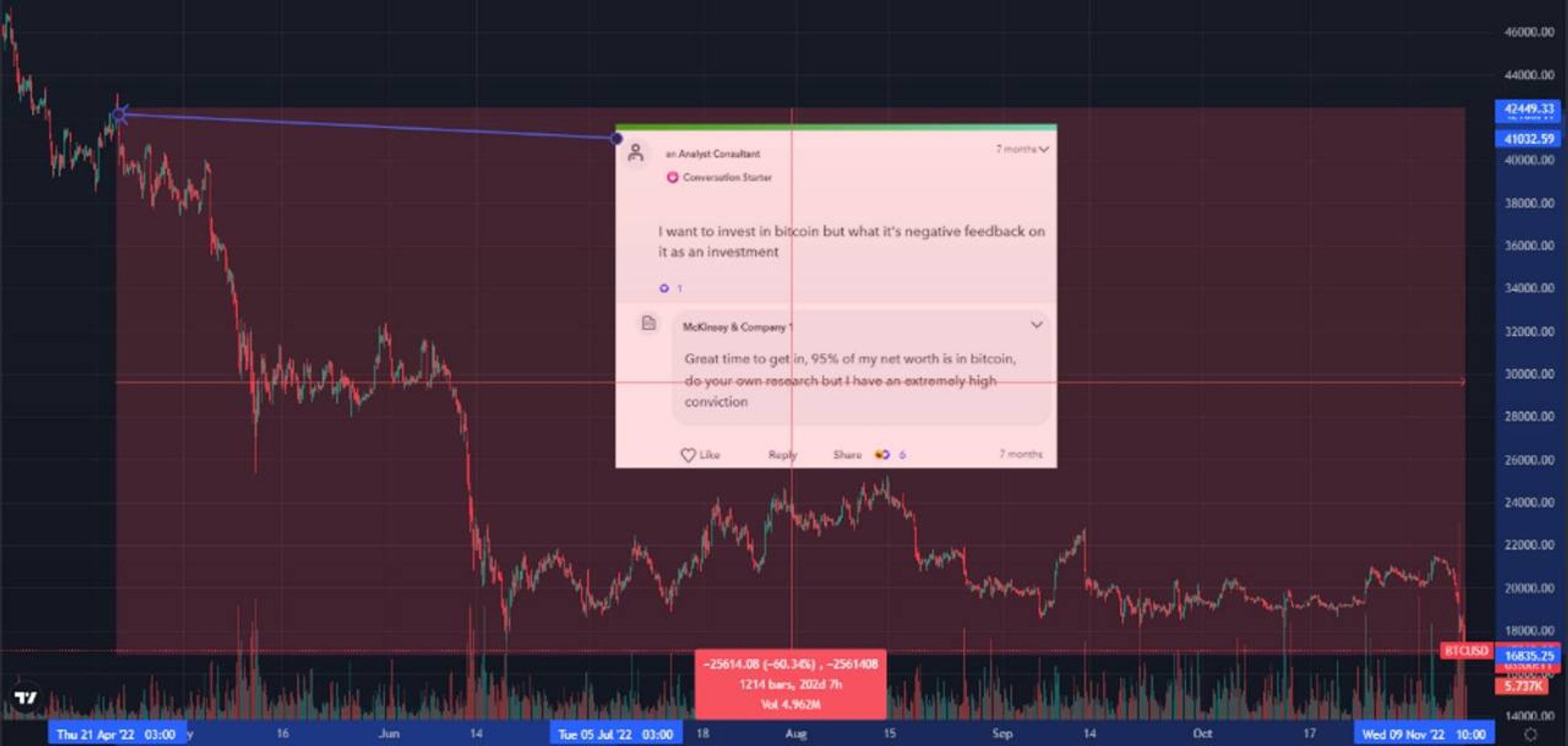

How to invest in commodities (e.g. wheat)?

Pro

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Enthusiast

Depends on your other savings goals and how fancy you are etc I guess. You make about twice what I do and you’re looking to buy a property that’s about 4x as expensive as mine. (Or, 2x as expensive as the combined total of 2 properties I’d like to have.) Not a ratio I love. But if you’re not actually planning to ever pay it off, and if you think it will appreciate more than the total of the interest payments (or at least enough that you don’t mind paying the rest for the pleasure of living there), could be justified.

Point of the more expensive home is so we could go public school route.

Bay area has been appreciating like crazy. 10% in the last 3 mo where I've been looking.

If you are living in a neighborhood where the property is $2M, chances are the value of the house will grow 6-10% on an annual basis . With interest only loan, you are leaving all that growth on equity on the table. In 10 years, you are looking at the property value doubling at 7%. That is another $2M. If you think the down payment you are going to make (400K) will yield 2M in 10 years then go with interest only loan.

Spy, or down payments for investment properties

Rising Star

Um yes. That principal doesn’t just go away. You have to pay it off after the interest-only period. And that’ll be rough on $500k

For context, I have 3 30 yr fixed loans so I'm definitely leaned toward that direction. Trying to be solid if I change towards a different route

You should absolutely take the interest only loan. Who’s giving you that? I definitely want one.

Pls share

😂

Everything you need to know about IO mortgages

https://www.bogleheads.org/forum/viewtopic.php?t=304655

Amazing

It depends on the interest rate. It might be worth it

It’s essentially paying $4k rent for a $2mil property - which is not bad.

The problem is with the refinance in 10 years. Rates will likely go up to control inflation, so monthly costs would be higher. And since it is a refinance then they will likely reappraise which means value of property could go up.

Seems like a lot of risk for $500k HhI

Rising Star

D1 no it doesn’t. OP would own the home and owe $2M. With an interest-only loan, their balance will stay at $2M. Any amount the home appreciates would be equity.

The danger is in the home value going down or if the home becomes difficult to sell around the 10y mark.

hell yeah brother

(As in, this makes a lot of sense)

What are you going to do with the $6k.

Now in the UK historically this was and still can be a smart mortgage strategy as you put the 6k into your pension. It then gets topped up be the tax benefit so anther you almost double the contribution @45% tax.

Then at 55 you take a tax free lump sum and pay off the mortgage.

Little tougher to engineer in the US because of the lower pension contribution limits but still something to think about. Maxing out his and hers 401k / IRA and HSA etc.

Not only is it not dumb, it’s the only way I would buy a house in CA

I do not see a downside