Related Posts

Bain & Company Hey Fishes,

Can someone referr me in healthcare/ life science related projects. I have 6 YOE in healthcare and life science industry. ( Pharmaceutical) Currently looking for opportunities in Management Consulting.

Kindly help. I am desperate for a job change

Accenture India Amazon India PwC Deloitte USI BCG Digital Ventures EY Tata Consultancy Capgemini Cognizant Infosys Microsoft Google

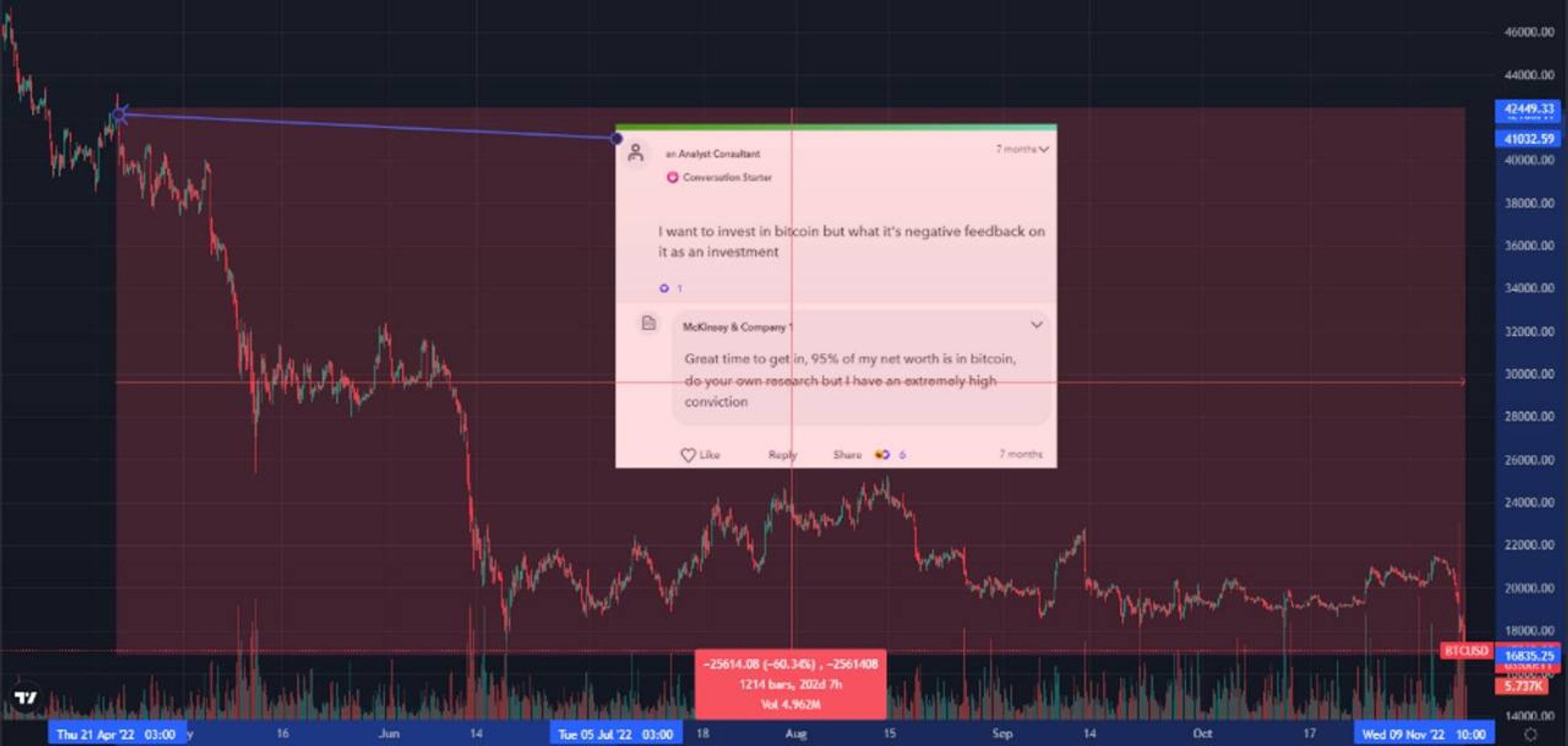

KPMG McKinsey & Company Bain & Company

Pro

What are the bands at sigma healthcare

Hi All,

Has anyone joined Accenture early and recieved joining bonus.?

I have been recieving mail like if I can join in this month I will get bonus as well as notice period buy out amount reimbursement.

But they are not mentioning JB amount before I confirm them when I can join.

I have 11 fixed offer, how much I can receive JB if I join month early??

Accenture IndiaAccenture

More Posts

Current FB celebrity is Slalom Consulting 1

Additional Posts in Personal Investment Chatter

Airlines going down... anyone buying?

Conversation Starter

Conversation Starter

Conversation Starter

New to Fishbowl?

unlock all discussions on Fishbowl.

Rising Star

How much do you have in your brokerage account right now?

At age 30, I’d try to max out 401k before brokerage. $3k per month to brokerage = $36k per year, while 10% of your income is only $16k. The tax advantages of that extra $8.5k towards brokerage will compound greatly over time.

I’d drop your brokerage contribution to $1k per month until you can get your 401k balance up.

Chief

Great point.

Chief

Two suggestions in addition to those here (especially Director 1's point about maxing your 401k):

1) Think carefully about why you want to buy a house and whether you should. Are your reasons mainly financial or non-financial? If you knew for sure that renting would be somewhat better financially, would you still want to? Do you live in an area with high, normal or low housing prices relative to rents? How likely are you to stay in this house for five, ten years?

2) Think carefully about your portfolio. Right now you are US only and tilted toward large and growth. Why are you doing this? Is it because you think that large, growth, and US will have higher returns? If so, you may be surprised to know that research indicates the opposite; tilting toward small, value, and ex-US has higher expected returns. If you do not have a principled reason to tilt, consider a neutral, un-tilted portfolio. If you want to tilt for higher expected returns, you need to do the opposite of what you are currently doing.

Chief

OK, good. You hadn't mentioned that.

It's best to consider your whole portfolio as one thing. What overall allocation do you want? Figure that out first then figure out how to achieve it.

Honestly, your financial situation looks quite good, especially considering you've only been in the US for a short time.

If you plan to buy a house within eight months, I think maintaining a 10% contribution rate to your 401(k) isn't low, considering you need to keep sufficient cash reserves for a down payment and as a buffer after purchasing the property. You can consider gradually increasing your retirement account contribution rate after you've bought the house and your cash flow is stable.

As for your credit score, 720+ is already very good. Making timely payments, maintaining a low credit card usage rate (ideally below 10%), and avoiding frequent new credit account applications in a short period will usually help improve your score.

At 30 years old, with $160,000 in income, $200,000 for a home purchase, and simultaneous retirement and investment accounts, you're already ahead of many others.

A 720+ credit score is already mortgage-friendly. Focus on keeping utilization low, avoiding new debt, and maintaining perfect payment history rather than chasing every last point.

With roughly $200k earmarked for a home purchase in the next 8 months, keeping that money in cash or high-yield savings is sensible. Short-term house funds generally shouldn’t be exposed to market volatility.

A 10% 401(k) contribution isn’t necessarily low. The better question is whether you’re on track to maximize tax-advantaged accounts. At a $160k+ income level, I’d prioritize capturing the full employer match and, if cash flow allows, work toward annual contribution limits over time.

The emergency fund looks healthy and your monthly investing discipline is excellent. Most people underestimate the value of consistently deploying capital every month.

My biggest focus before buying would be optimizing debt-to-income ratio, preserving liquidity for closing costs and unexpected expenses, and avoiding major credit inquiries before mortgage underwriting.

That makes complete sense. A lot of people become so focused on maximizing every tax-advantaged account that they overlook the importance of maintaining flexibility and liquidity, especially when a major purchase is on the horizon.

If wealth accumulation is the objective, then the real conversation becomes less about whether you’re contributing 10% or 15% to a 401(k) and more about your overall capital allocation strategy, risk tolerance, and time horizon.

What I find interesting is that you’re already doing many of the right things—building retirement assets, investing consistently, maintaining an emergency reserve, and preserving cash for a home purchase. The next layer is usually optimization rather than accumulation.

After the house purchase, do you see yourself as more of a passive index investor, or would you be interested in exploring broader wealth-building and portfolio strategies?

Are both your IRA and 401k traditional? And if so does your employer offer a Roth 401k (roth is after tax contributions that grow and are withdrawn tax free at 59.5+ years old) might make sense contributing some retirement savings after tax now rather than paying tax on everything in the future especially since you are only 30 and likely not at your highest earning years. Basically a hedge on future tax rates. I personally prefer Roth as all of the money in the account is yours and not subject to taxation in the future.

Do you really need $200k to put down on the house? I would increase 401k contribution to 12-15%

Pay 90% of your credit card balance 5 days before the end of the cycle every month

Chief

Not 100%? Why pay interest?