Related Posts

Conversation Starter

Conversation Starter

More Posts

Coach

Pro

Bowl Leader

Coach

Additional Posts in FIRE Financial Independence Retire Early

Anonymous User

Coach

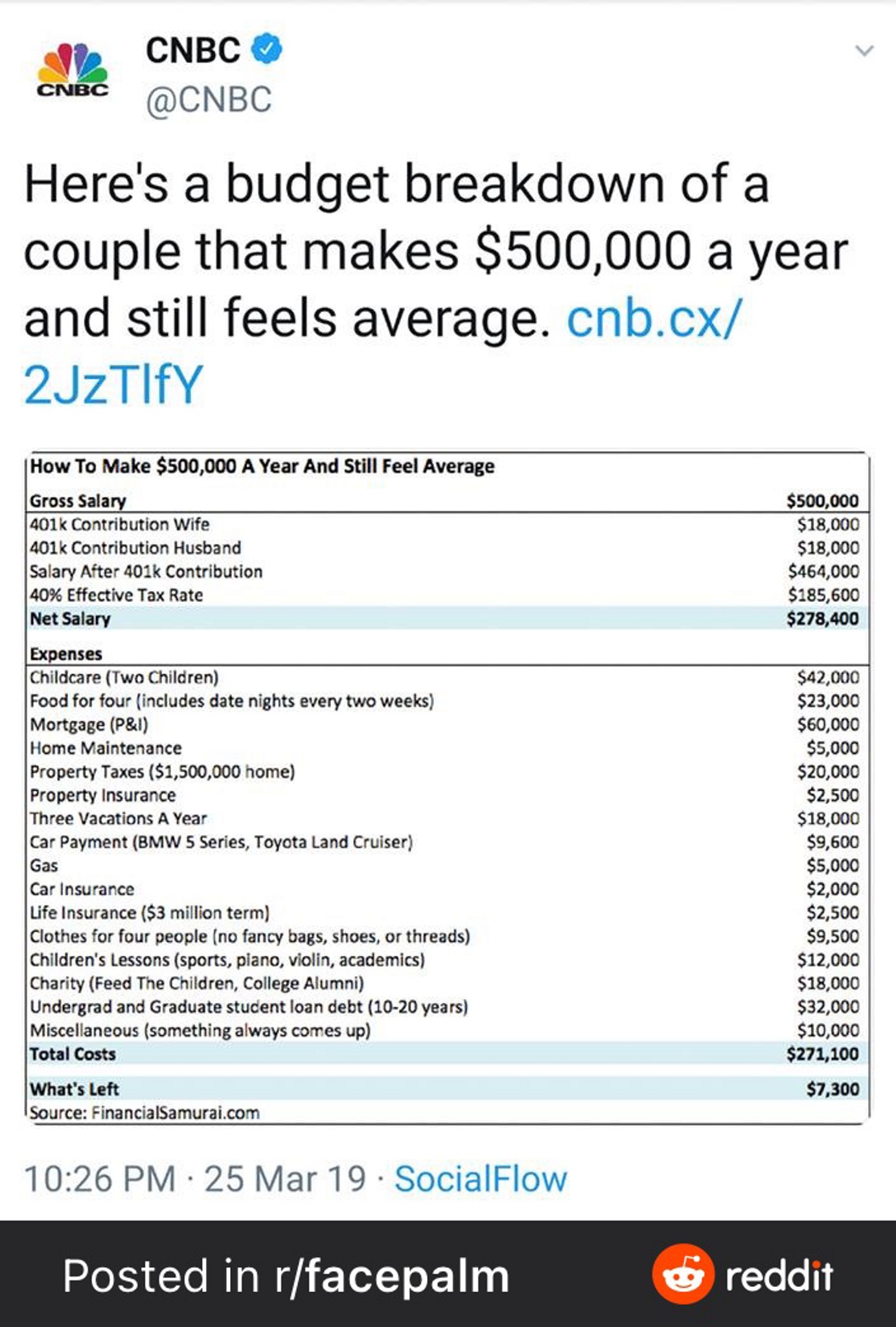

Nyc couple with $0.5m in income who feels average

Anyone else into Bank Bonus churning?

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

If the housing costs aren’t uncomfortable on either budget - i.e. they don’t exceed 40% of gross for either party, then I recommend going 50/50 just like you would a roommate - which is technically what you are if not married and no partnership agreement is in place. Once my husband and I got engaged we opened a joint account and both contributed equal dollars to it for shared expenses, including a new home. I made a bit more and had a lot more wealth but knew he’s catch up soon. And if we’d split I’d have wanted to keep things 50/50 anyway.

pro rated

What I would ask is why you’re getting married? It is one institution I just never understood. The split of expenses depends on what you’re both comfortable with, however.

Probably depends on 1)if you're planning on having kids and 2) if your partner is planning on doing FIRE as well.

Those will affect how/if you combine finances.

Ok, I'd split the condo 50/50 until you're married then. Other expenses should be either according to income, or taking turns paying.

When I moved in with my husband, we paid rent proportionate to what we had been paying previously when we lived alone. That way it was in line with how much we prioritized housing.

You’re in your mid-20s and both make over 175k? I think you should just join everything unless you plan on getting divorced.

50 50 chance it happens

If you will be keeping your assets separate even after you are married then consider a prenup. Consult with a family law attorney in your area on whether that is right for you or not. Getting a prenup does not mean you are planning for divorce. It is one among many prudent investment decisions where it is appropriate.

On a non-legal note: you don’t know the future and one of you could have a medical event or something else come up later that means that person’s income reduces significantly. You should discuss now what will happen with paying expenses if one of you no longer makes a significant amount of money.

Also, consult with a financial advisor who can do financial projections because you may be able to earn more from your investments by pooling your funds together. You can pool a portion of your assets and then separate the interest/gain when it is distributed. NOTE: I am not a financial advisor. So, consult with one to determine if that will be correct for you or not.

Yes we have talked about getting a prenup. We are both pretty logical and reasonable when it comes to finances

First get married I would say but definitely have the financial conversation with a marriage counselor before that... 50/50 is fair if both make the same income

My question was based on both making high income ($175k+ but with still a decent level of % delta…. Ie $200 vs $300)

What do both of you do??

(My analyst title is outdated)

Here’s what we do in my marriage:

I pay all of the main expenses. I’m a better admin person so it just makes sense.

Both of us contribute each pay period a pre-defined amount to savings based on the fact that 1) I pay all the main expenses and therefore have less to contribute to savings and 2) based on our respective incomes

The rest we keep in separate accounts and don’t micromanage each other.

Note: we are both frugal AF so there are no trust issues about the personal accounts.

I’d split it evenly.

There are pros/cons of keeping finances separate. Because we combine, I'm gonna highlight pros for combining/cons for separating.

- You'd never be able to figure an equitable split if separate. 50/50? But you earn more; Proportionate? Well why should I get punished by paying more for b/c I earn more; can go on.

- If you combine, divide labor, and the better skilled person can manage the finances, allowing other party to focus on other family improving tasks. You both are board of directors, with a CFO/VP doing operational activities

If there is a divorce in your future, then combining is not for you.

Given you’ve already bought a condo together…..Get a pre-nuptial agreement that is valid if you split up before getting married. Have some deep heart felt convos about how money is going to work when you actually get married. How are you going to handle the $20 you spent yesterday (and the 6000 other times) for groceries or the new car your spouse wants to buy just because the last new car is over a year old? What about working (or not) after the kids come along? - it can be difficult for some folks to stay in their careers either at all or at the level they were once at when the kids come. How will you handle finances if the disparity between your incomes grows? Come to a decision matrix you can live with.

For us - putting it all in one pot works - we have similar philosophies on spending -both neither overly frugal (although I lean that way) nor overly spendy. We don’t think at all about the 6000 times we buy something small. We do look at our overall budget but we’ve been in the fortunate position that we’ve never had to cut back. We started out with me making significantly more than him but when the kids came, I cut back my career to take care of them so now he makes about 10x what I make. We discuss big items (think cars and homes not toaster ovens). I make all the financial/investment decisions, pay all the bills, taxes, etc. He sometimes will say “he lets buy this stock” or whatever and I will usually do that but mostly he just asks what are net worth is every once in a while and I’ll tell him.

Wow making 10x. What income levels are talking about here?

So you have drastically different incomes, however it all goes into joint accounts, and a detailed pre-nup in place?

At the income levels you’re at I would just do everything 50:50 if you’re not doing joint finances.

Just do 50/50, much easier, and easier transition to married life