Related Posts

Enthusiast

Community Builder

Chief

Anonymous User

Conversation Starter

More Posts

Conversation Starter

Media buying burn out. Is strategy any easier?

Additional Posts in Finance

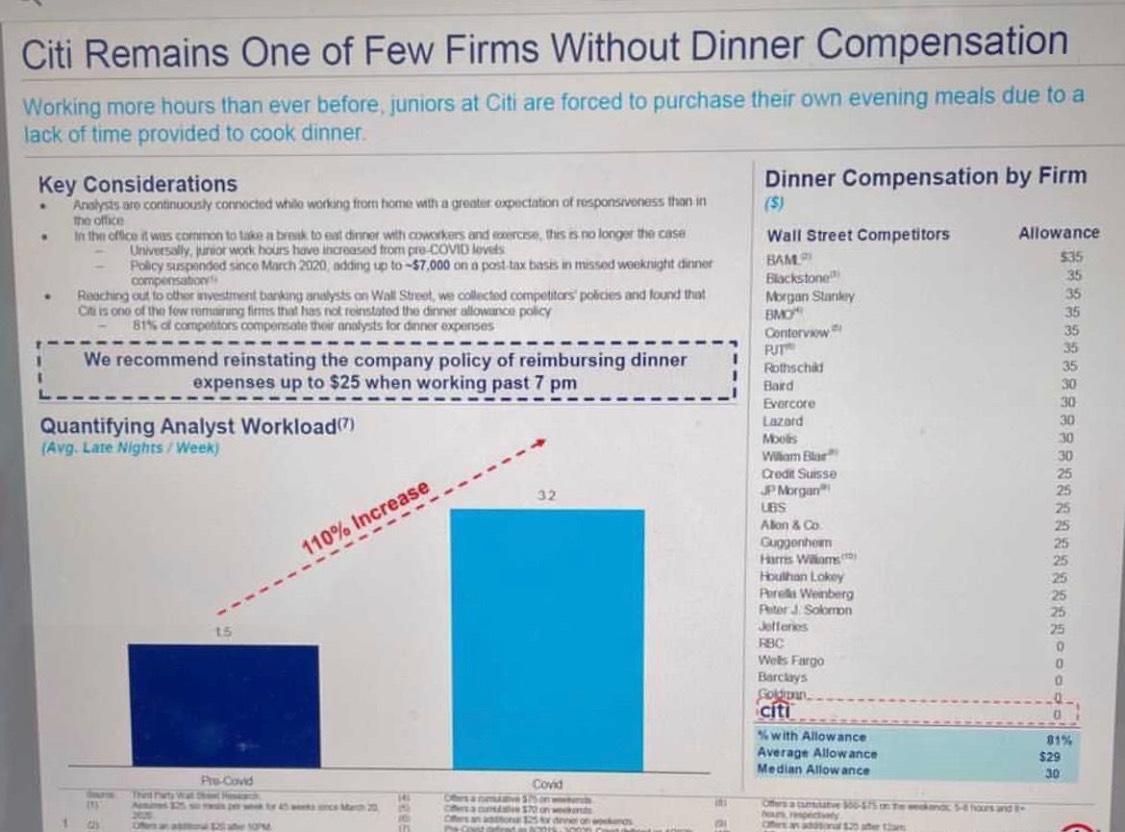

Dinner compensation allocation by firm

Hey what's ur number

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Term life insurance gives you the death & succession protection for very very little $$$.

IUL is an appropriate choice only for very high earners as a taxation and saving loophole. Not appropriate for the average person. Very expensive and has large front end expense.

I actually think IULs are excellent supplementary investment vehicles, particularly for their dual purpose. You are very young, but assuming you and your husband plan on starting a family in the relatively near future, having an IUL protects some of your wealth while also providing a safety net to your children should something untimely happen to either of you. Sure, term life insurance is cheaper, but if you can lock into a whole life policy now, while you're young and healthy, I think it's a wiser financial decision for the long term. Of course, this is my personal belief - I'm not an expert, so take it as you will and maybe speak to a financial advisor.

Rising Star

Do you have beneficiaries for whom the prospective life insurance policy would be intended? If not, there’s usually no reason to use life insurance as an investment vehicle unless you have millions in income per year and need a tax haven not solved for through more traditional means like a health savings account or retirement account(s). Worth evaluating life insurance on its own merits irrespective of the investment component. And if you do decide you need life insurance, I agree with Carlyle that usually term life gets you what you need for way cheaper.

That’s very helpful! I wasn’t in a huge rush but figured it was about the right time to start considering it. Additionally, the advisor that brought it up and I are in the process of becoming referral partners and I don’t want to refer customers to someone that might be taking advantage of uneducated clients.

You’re pretty young so I don’t know if it’s appropriate but it depends on how much. Personally, I’d look at a good term policy with a conversion rider on it. You can cover the mortgage and then some then retain the underwriting benefit when you convert to a perm policy.

If you want to be a referral partner with this person then I would ask them what the “good, bad, and ugly” is about this product. Ask them to disclose compensation differences across different products. Look them up on broker check- are they registered? What licenses do they hold? Happy to pop in a DM to chat more about this.