Related Posts

My father passed away last week. I had wills written up for him, he has a small c corp, and we don’t live in a community property state. Mom’s still with us, fortunately.

Besides informing social security, filing a life insurance claim, getting a death certificate, flagging his credit card, and starting the probate process, is there anything else I need to do immediately (in a financial/regulatory sense)?

I’ve been following the guide here: https://www.reddit.com/r/personalfinance/wiki/death_of_loved_one/ but others guidance is always appreciated.

More Posts

Does anyone know if insight has kicked off?

New guilty pleasure: Indian Matchmaking on Netflix

Enthusiast

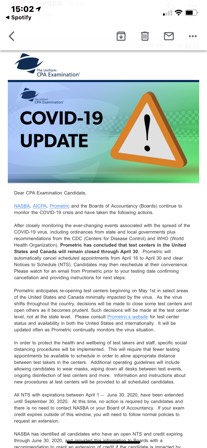

Prometric closed until 4/30

Additional Posts in Accounting

EY Irks (2): Timely review never timely

why is everyone moving to Seattle?

Dating a coworker? Bad idea? Really like her..

Rising Star

Survived day EY Purge Day 2 in my office

New to Fishbowl?

unlock all discussions on Fishbowl.

I just have a customized Excel with my budget. I allot a certain amount of money to spend per month and the remainder goes to brokerage accounts, a savings account (in a different bank), and a savings account for fun things (ie. Sports tickets, travel, etc.). That way I only see what I've deemed available to spend that month.

I use Excel too. Have a budged with amounts for different categories (house bills vs. Fun things like eating out and traveling) and then I enter what I actually spend every month on those things and compare through formulas I have set up. This way I know how my spend going during the month and I can cut back when I need, but also see the bills I can't avoid like rent and power.

I have used youneedabudget.com for a couple years now and love it.

I second this. YNAB is a life saver.

1. Separate your bill money from your discretionary spending money.

2. Use an online bank like Simple for your discretionary spending. You can define spending categories and it’ll automatically allocate deposits according to how you define your budget categories. Then you can see how much you have to spend for food, entertainment, etc. as you spend using the debit card.

Those are the main things I did to get out of debt and recalibrate my spending habits. It might be worth your while to hire a financial coach.

Pocket smith is what I like. You have to pay for it, but provides features ynab and mint cannot.

I also use an excel sheet to budget and have separate Accts for bills vs spending. The best thing that’s forced me to be disciplined is adopting a cash envelope system. Once the cash is gone, it’s gone. Check out Dave Ramsey. Following him helped me a lot.

I’m not a huge DR fan. Every time I tried his approach, it felt too extreme. I may use the envelope system for just food tho. That’s the one area where I wild out every month.

I use Pocketbook to track historic spending, as it categorises my transactions.

I then exported into excel and used 6 months as a gauge for my budget. Split it into needs and wants and tried to set reasonable goals for each category (not too aggressive), and a monthly savings goal.

I just keep a log on my phone in Google Keep of how much I spend on the categories I can control (Food, shopping, gifts, fitness etc). It’s not super exact or up to date but let’s me know how I’m tracking. The more I go over, the lower my savings will be.

I wish there was a simpler way that worked for me. 😅