Related Posts

Conversation Starter

Does anyone happen to be in or know anyone who is in the RUV alliance Angel Investment syndicate? https://ruvalliance.com/

We’re looking for angels who are familiar with investing through RUVs (a special purpose vehicle on Angellist) and specifically think the RUV Alliance could bring a lot of value.

#startup #angelinvesting #investing #angels

Conversation Starter

Best Alt Coins to buy?

More Posts

Bowl Leader

Bowl Leader

Bowl Leader

Ever did that??

😂😂

#Meme #MondayMotivation

Ciao! We're hiring a Sr. Brand Marketing Designer in NYC for Duolingo! Ideally we're looking for a senior designer with both agency and in-house brand experience with a passion to bring culture stopping ideas to life. If you have an eye with impeccable detail to craft, passion to develop world class award winning creative and believe in making language accessible to all, hit us up on our careers page! careers.duolingo.com/#openings

Additional Posts in The Real Estate Bowl

New to Fishbowl?

unlock all discussions on Fishbowl.

I’d say don’t buy a house and see how things shake out a year from now.

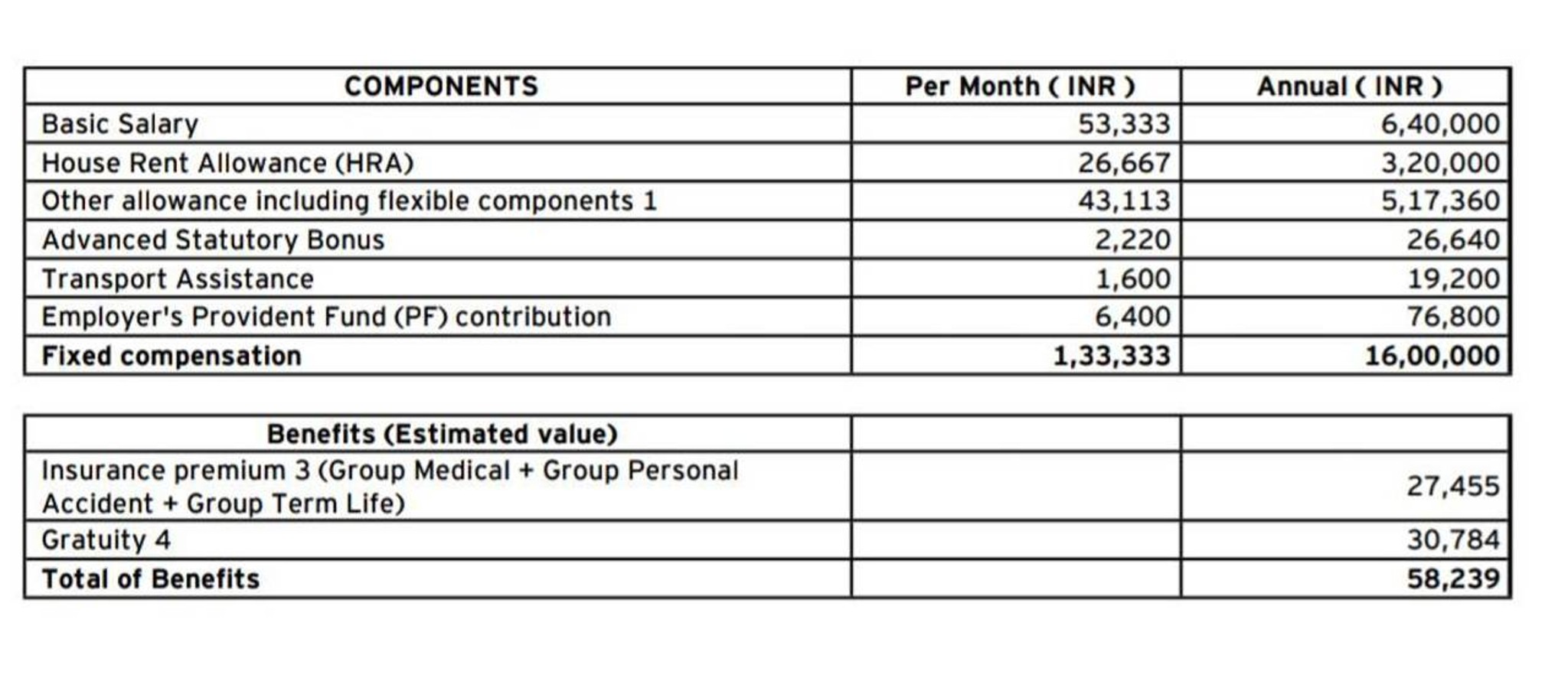

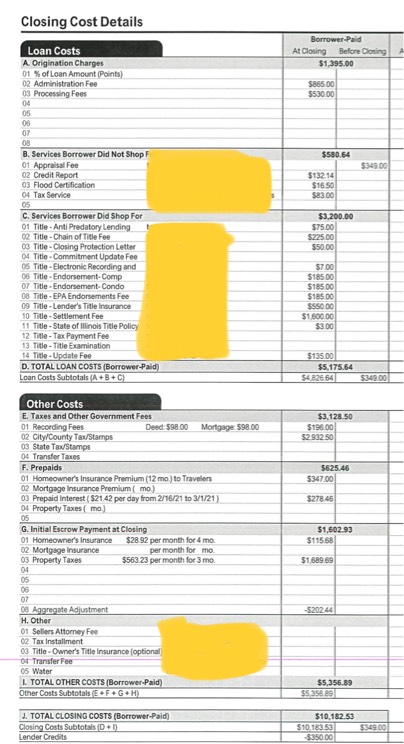

So this is an $800k house. I plan to put down about $200k. Planning on doing a conventional at 30 year. My general philosophy is I'm going to aggressively pay down and live lean. Probably going to take home ~6.5k/month after withholding/taxes/employer 401k match.

AllyBank Loan Details: https://imgur.com/a/rFIMRne

My Local Lender's Loan Details: https://imgur.com/a/ENPnRrQ

Essentially I got a locked in rate/loan estimate after buying down points from Allybank's home loan powered by better.com to the tune of 5.12% by buying ~$24k in points (I have a 790 credit score, and roughly 250k in liquid assets that I have been saving for a house for a while). I talked to another lender (local mortgage lender, LML) and he said I wouldn't want to do that because I would be paying a lot for points if the rates go down within the next 1-3 years.

He said I should do a 2-to-1 buy down with the first year being 4.99%, the second reverting to 5.99%, and the 3rd year at 6.99% but that within that time I could probably refinance to avoid the 3rd year. With the 2-to-1 buy down I would pay ~$10k I guess for something like points.

Ultimately I'm trying to figure out at what threshold in payments or amount paid down would I reach 20% equity (or would I already be able to refinance whenever due to my putting ~25% down?) so I can qualify for refinancing and looking at the Federal Reserve to gauge their general sentiment on the funds rate so I can decide whether to go with the buy down.

From reading at least within this year some of the heads of each regional bank are fairly steadfast in keeping above 5% to combat inflation. And just looking at the movement in rates in the past couple years it has steadily gone up, but the pandemic was such an anomaly that its hard to use it as a predictor in any way. Also it goes up between a particular time frame roughly at .25% every 1-2 months so at what time frame with my mortgage will it look like my paying $24k in points was a bad choice given the interest I'm paying down if the federal funds rate drops?

So, which option makes the most sense? If I go with the buy down option can I refinance and pay points in year 2 since it goes up with another lender? I don't think the local mortgage lender is able to compete with Allybank so I'm not sure how refinancing works between lenders if its moveable.

Your budget is wack. Max you should be looking at assuming minimal other debt is mortgage is 3x your annual comp, especially with rates so high. Otherwise you're going to be house poor, especially considering all the other costs of owning a home (maintenance, utilities, HOA, etc.).

Your 2/1 ARM sound very risky as well. You want one that sticks at current rate for at least 5 years giving the market more time for rates to drop.

Is a temporary buy down an ARM?