Related Posts

Off Topic : 1) When Does a software engineer start financial planning for retirement since the our Career span is only 15-20 years on average.

2) How much and which schemes to invest to mitigate the risk?

3) How much do we need for retirement? Tata Consultancy Infosys Mindtree IBM Wipro Capgemini Cognizant HCL Technologies

Enthusiast

What is comp like at a pension fund?

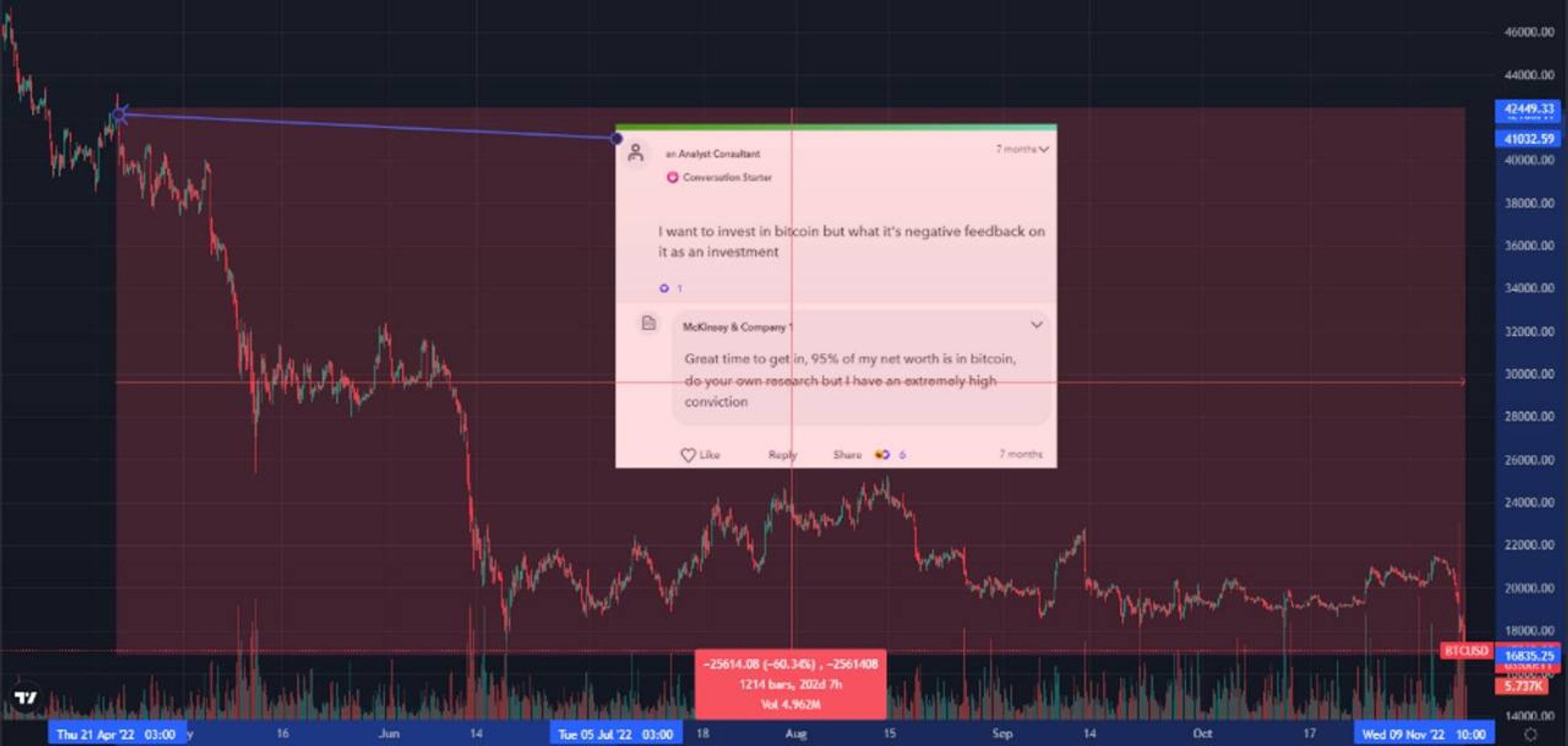

Conversation Starter

what you buying?

More Posts

Hello, Can any one assist me the title hierarchy in JPM On my offer letter if is written as Title will be Data Management Specialist IV of CIB Does this means operational analyst ? What is the next designation after this ? How much time usually JPMC take to promote to next designation? I tried to reach out to the HR but no response from them I will be joining JPMC on 5th December it would be great if you guys can assist me

JPMorgan Chase JPMorgan Investment Management

Rising Star

Subject Expert

Additional Posts in Personal Investment Chatter

Pro

Conversation Starter

Where do you buy dogecoin?

Conversation Starter

Thoughts on Jumia stock?

Conversation Starter

New to Fishbowl?

unlock all discussions on Fishbowl.

Pro

DRIP because yes you pay taxes, but never 100% of dividend. So you’re stocks will continue to grow and slowly build more income. Couple this with stock appreciation and dollar cost averaging impact from monthly/quarterly reinvestment. 💡

But the dividend doesn’t really help you. You are in the same place as if there was no dividend. It just causes you to pay a little tax and increases your basis a little.

I look at dividends as a forced sale of a portion of your shares. I don’t get the allure anyway. I think some just like the income. I personally would rather sell when I need. There is nothing wrong with them in an Ira for example, but to me total return is what matters not dividends

Enthusiast

Qualified dividends get favorable tax treatment

Qualified dividends have the same tax treatment as LT capital gains. Only difference is you have to take the dividends while you only take gains when you sell.

Pro

Everything is taxed though, your 401k is taxed when you withdraw money

I agree but why would you stop deferral sooner that you need to? That is my only point. Dividends just make you pay sooner than otherwise. Nothing bad about them, but nothing necessarily magic about them either. Some invest for dividend income and that does not make sense to me. But if it works for them, that is fine. The most important thing is to keep investing. This is a minor issue either way in my opinion

Enthusiast

I think of them as a higher risk super aggressive high yield savings account. If I ever needed a large chunk of money I’d probably liquidate them first.

Enthusiast

Absolutely. I just think of my dividend stocks as a savings account and my other stocks as investments. But again, yes. Depending on the circumstances I could and would consider liquidating other parts of my portfolio.

It’s pretty much just a different risk profile preference. Only answer that makes sense to me is “investment type diversification”.