Related Posts

Hi fishers! I have offer and signed contract with Deloitte UK and my start day is in the beginning of April. I need skilled worker visa, and we haven’t applied yet for that. Screening and onboarding is in progress. Immigration team doesn’t reply since reached me out 1st time. How much time does it usually needed to go through the whole process? How many days take for visa to be approved since application?Deloitte

Conversation Starter

Conversation Starter

Pro

Enthusiast

More Posts

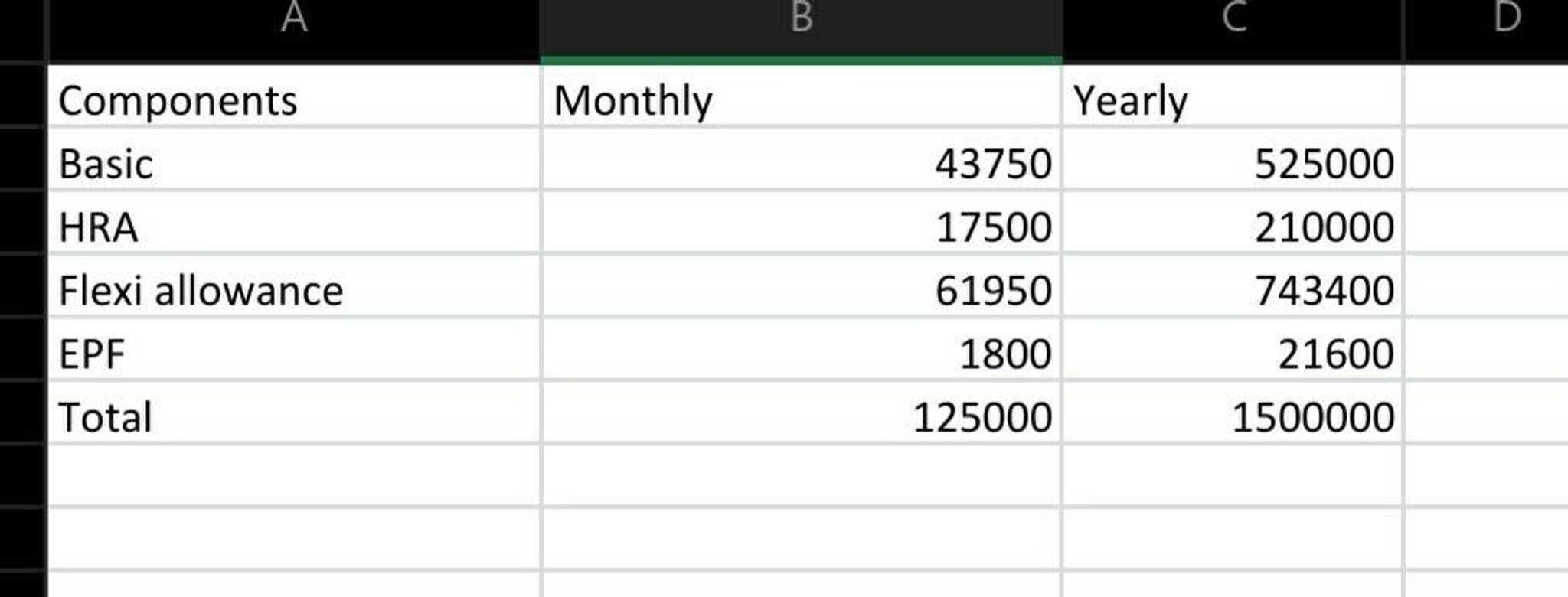

Hi,

What role I can expect for 6.8yoe developer??

Conversation Starter

This is just GOLD.

Is PDM ever going to be less crappy?

Enthusiast

Pro

Additional Posts in Consulting

I’m not sure if I’m crying or laughing right now

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Credit history? Not only on time payments but the average credit line length. Can't be all new cards. Utilization is another big one.

Mine has tanked lately too. It's getting harder and harder unless you're like 55 and over to have a good rating

I read something this week about the credit agencies being sued for fraud.

826 FICO here

For utilization if you're above 10%, it takes away a good chunk of points. I remember when I went from 13% usage to 9%, my score went up 51 points.

I have a CSR and mine just dropped 4 points for no reason, maybe there is a connection?

The number of recent inquiries impacts your score, so the fact that you recently opened a credit line would lower your score. The extent of the impact would vary depending on total number of lines opened in past two years.

Inquiries drop off after 2 years max

Number of cards, average account age, lots of revolving credit with not much long-term debt, and limited payment history (if it's less than the full 7 years)

The thing is, I'm fairly certain when I opened my CSP about 1.5 years ago my score was at least 30 pts higher

@D1, only connection would be the inquiry - which will usually drop your score a little.

What a1 says. I jumped from 8% to 12% utilization and mi score dropped from 806 to 750

If you haven't missed a payment then you probs either (1) have had a lot of inquiries recently, (2) are spending close to the limit (which usually would be hella difficult for CSR), or (3) have some type of fraud issue that you don't know about.

The util might be it. I think I'm a bit over 10% right now. I'll see once I pay my bill.

What do you use to check it? Is it the official FICO score? Most credit reporting/monitoring sites use their own scoring algorithm that "estimates" your FICO score

Set up a Credit Karma account and it'll tell you specifically what's negative affecting you as well as what your positive points are.

And to clarify, Credit Karma shows your Vantage credit score and your credit reports. You can get your FICO free via Discover even if you don't have an account w/ them.