Related Posts

Conversation Starter

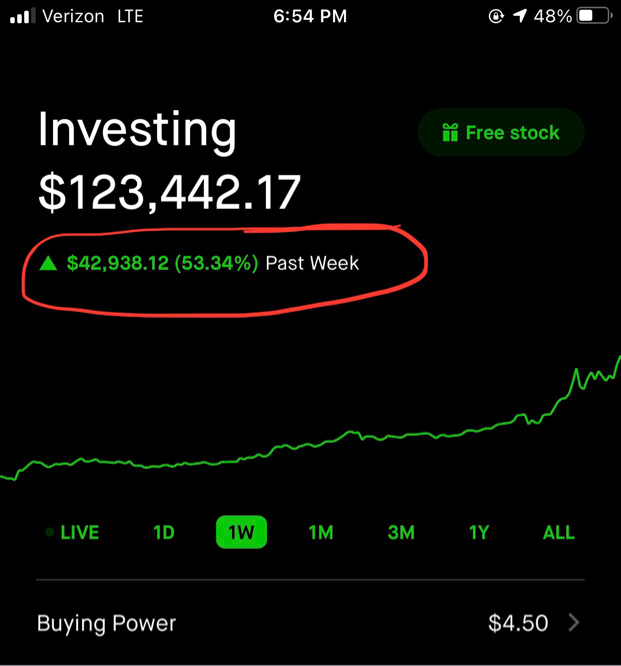

Visual Storyteller

Anonymous User

Coach

The Anti-Bitcoin Asset You Likely Forgot About

Worried about inflation?

The U.S. Treasury’s Series I savings bonds have a 3.54% interest rate that will only go up as prices rise.

https://www.bloomberg.com/opinion/articles/2021-05-20/personal-finance-series-i-u-s-savings-bonds-offer-inflation-protection

More Posts

Subject matter experts rescuing the day

Additional Posts in Personal Investment Chatter

Pro

Thoughts on pionex?

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Rising Star

You are financing wayyyy to much. Payoff the couch, computer and Home Depot immediately as if you miss payments on those ever you will get screwed. If you can’t pay cash for it, you shouldn’t be buying it for those types of items. I would personally only finance a car (somewhat reluctantly) or a house.

With regard to student loans, your interest rate is the biggest consideration. I would not hold out hope for student loan forgiveness and make sure what payments you are emailing are decreasing the principal (eg not just interest).

I’d also suggest putting a detailed budget together as what you have said indicates to me you’re living above your means. Do you have an emergency fund?

Ok - point taken. Let me adjust - it’s probably not a good idea to finance furniture if relying on future cash flow to pay. If you’re just saving a few bucks interest then by all means. (I obviously use credit cards for everything so that’s financing too)

Pro

It all comes down to interest rate. If it’s in the 3% to 5% range, pay casually. If it’s 7% or higher, pay aggressively.

… it’s 6%

Don’t hold your breath on student loan forgiveness and just assume you will pay it off.

If you have multiple student loans, start with the higher interest one and work your way down to the lowest over time.

For the 0% loans, when does interest start? Once you pay these off, do not put similar purchases on credit. Save the money over time and buy them outright.

People never provide the most important detail - interest rate

Set up a plan to pay your student debt off in 3 years. If you have more left over to invest, then by all means.

Additional context -

6 month emergency fund ✅

Home - while we knew we had student loans, overall very happy with the choice we made to buy what and where and when we did. Home has appreciated 20-30% since 2017 when we bought it and wouldn’t have had the childcare support system we love had we lived somewhere else

Have been waiting for the federal student loan pause to end before making a considerable payment of ~$25k ( my grad school loan… so timing of $70k —> $45k loans is about January).

Will be in a position to knock out other $45k over 2022/23, but make face a slight hiccup with childcare for 2nd child (likely).

Overall, am seeking other perspectives on how to make money work for you if market can get 10-12% returns vs student loan payments of ~5%.

I’ll add that grad school loans will likely never be forgiven as I’m pretty sure they’ve only slightly considered undergrad