Pro

Related Posts

More Posts

Has anyone worked for IKEA FOOD?

Bowl Leader

When is the Deloitte Tax comp call?

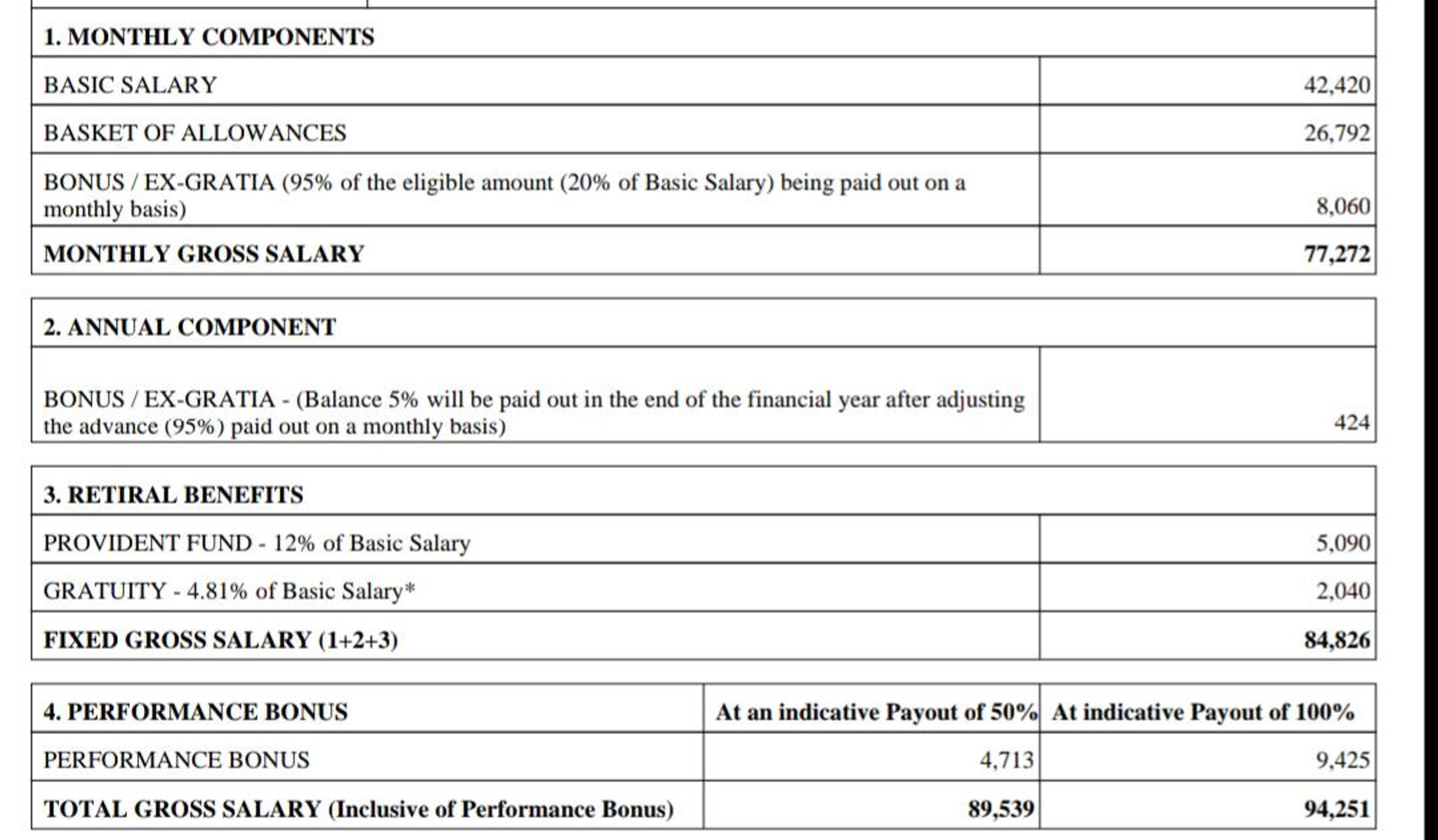

Hi guys :) Glad to join fishbowl and this community. Guys I have an offer of 14.41 ctc from a big 4 (11 is fixed).

Technology-Microsoft Dynamics 365(I am a functional consultant in SCM and HR; Relevant exp: 3 yrs & Total exp: 4 yrs).

My interviews in IBM are done and I am waiting for the salary discussion with HR.

What is the likely offer that I am going to get? Any idea? (My expectation is 16.5 lpa ctc). I will adjust my expectations as per replies here.

Any response is highly appreciated :)

Additional Posts in The Worklife Bowl

Conversation Starter

Pro

Conversation Starter

Do you believe in life after love? Ed does!

Chief

Rules for thee not for me!

Rising Star

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

I laugh when people say they can’t save money. Seriously. When me and my wife got married, our household combined income was less than $100,000. Today, neither of us has a six-figure income. Yet in the 20 years we have been together (married 17); our house is paid off, I grew my wife’s retirement (work) account to seven figures and already have 2 years of college saved up (local instate tuition that is). Our retirement contribution are at 15% for me and 17% for my wife (only because she company has a pretty fantastic money manager - hence the seven figures in 20 years). Even while able to save, we still take 4-5 vacations a year. And no, we don’t have any side incomes supplement our spending. We do have investments but all our our capital gains are invested back in. I don’t use my investment gains for toys.

To the person who posted about no college debt must have graduated before 1990--i started college in 1991.. when I graduated 5 years later I was debt free. I paid out of pocket. Some semesters I could only afford 3 classes so it took a bit longer. You can save if you choose to live within your means. Can you survive on one vehicle, find a cheaper insurance, cut down on nights out, and you have to do research on child care. Child care is expensive, but if you do research you can find a good person/school/daycare at a decent price. If there is something you want save for it instead of putting it on a credit card. Try living in a smaller space to save money. There are always ways to save if we are willing to make the necessary adjustments to get what we need.

Or you can go the faster route of robbing a bank. Then living and meals will be free. Ijs

My daycare is $2400/mo in a place where that’s more than double most mortgages, so yeah. I feel this.

Rising Star

Public school is free (or more correctly supported through taxes). Some areas may charge for full day kindergarten.

Theres a good book you should read, called “We Used to Have Money, Now We Have You.” Get used to it 🤣

In the same boat, rent + daycare+ fixed montly bills alone take 6k/month, adding groceries, medical or random expenses take it to $8-9K per month expenses.

Exactly

I’m there with you, I feel like once you have a mortgage and kids you’re kind of at a point at least for a few years where you’re focused on the important things, kids, health and work vs having fun so even if you have a few discretionary bucks you’re spending it on something important but not instantly fun. Is putting a few bucks in the college fund important? Yes. Fun? No. Was spending that money in your early 20s at the bar and trying to get someone to go home with you important? No, but was it instantly fun? Yes.

What surprised me was how it felt to relieve one kids daycare payment (yay!) when they stared kinder only to find out aftercare + summer camp cost just as much (ugh!). It never ends!

I was thrilled when my son transitioned from infant to child care. Saved over $100 week. The aftercare programs were $$$ and camp programs were insanely expensive and weren’t a full day (and we aren’t talking about Camp Dudley).

Why don’t your children work? They sound lazy and entitled to me.

Our country is failing us as working parents. The way things were before is just not comparable to the society and the economy we live in now. You’re not alone, we keep increasing our salaries and are still struggling as a high middle class. I don’t know how those barely getting by can make it through

Rising Star

Genuine question, what do you think the government is for?

I get the struggle and I don't even have kids. I pay all the expenses and take care of my elderly mom and dad. Rent bills etc. It's hard for me to save much but I'm not the greatest with spending so any tips would be greatly appreciated. P.s the comment section made me laugh.

This is also my exact life. You are not alone.

The first 5 years are tough with small children. The sun will shine again!

Daycare in our area is also like 2400 a month. It’s essentially 100% of my wife’s take home meaning she really would be working to pay for health insurance and daycare. She initially wanted to quit her job because of this, but we decided the long term drop in salary (from 4 years of experience not happening) would make us worse off.

Fortunately we both work from home and I’ve got tremendous flexibility and in scheduling so we haven’t needed to pay for any childcare yet.

Yep. $2800 month on daycare stings.

It won’t help with daycare costs but have you considered joining your local buy nothing group? You can get hundreds of dollars of things for the kids and the house for free and pass on what you don’t need to others in your neighborhood. Ten dollars here and there for toys and books and household doo dads add up quickly. Its good for the Earth and great for your pocket book! 🌎 ♻️ ❤️

Yep, wait till the daycare turns into after-school and weekend activities and phone bills and college.

My checking account is more of a pipe than a funnel.

People on much lower incomes make it happen. You chose an expensive lifestyle.

Without posting your actual cash flow analysis, it is impossible for us to provide help. But if your both bringing in $200k+, your pay is over $20k/month (after taxes).

My recommendation is to download a cash flow analysis worksheet, and spend a half day/day and really crunch the numbers onto that analysis to see where the money is bleeding. You may need to do this for a few months to account for any annual swings. I would also do the same analysis on a yearly basis, to account for large annual based expenses (like vacation or large purchases).

Then you will know where your money is going. And your cash flow...if you don't have positive cash flow, you can't be saving.

People yapping about how some person bought his house 20+ years ago yadayada. I bought my house 4 years ago, 110k, 2 stories, basement, attic, 4 bedrooms, 3 bathrooms. Live in a LCOL area because remote work, wife doesn’t work. We save more per check than OP does per month. If my wife got a job, she’d start at low income and it would do nothing but cover the cost of childcare required by her working. Consider relocating now that the world has grown up? Plenty of nice houses for sale in my area

Low income area doesn't make much difference when your closest neighbor is 1/2 mile away! I love it.

Time to test how it feels vs actual. The biggest diff between cash savings and investments is you seldom have visibility into the numbers unless you’re checking your investment accounts all the time. Do you actually monitor how much you actually save? Determine what you want to save across your accounts each month, contribute, and then you’re good.

Do you have a budget?

During the child care years we just spent away. It’s hard enough as it is- just delay saving for a while. Money is there to help you need your sanity.

Trick is to always pay yourself first (which it sounds like you're doing for retirement, but what about your savings and/or short-term investments?). If your bank gives you the option, I would suggest exporting your monthly statements in excel and run a pivot table / group your day-to-day expenses into categories (e.g. dining-in, dining-out, coffee, entertainment, alcohol, etc.). You should then be able to figure out pretty quickly where your money is going. I try to do this once a quarter.

What car do you have? Also consider public HS