Related Posts

Stressed, depressed, and well dressed

Hi Friends , I have 18+ years of experience across multiple departments, with over 12 years exp in Business Development , Project and Program Management. Looking for suitable job opportunities as Senior Program Manager . Any referrals are appreciated . Could you please DM . Thank you.

EY Google GE Deloitte Dell Amazon

Pro

Additional Posts in Personal Investment Chatter

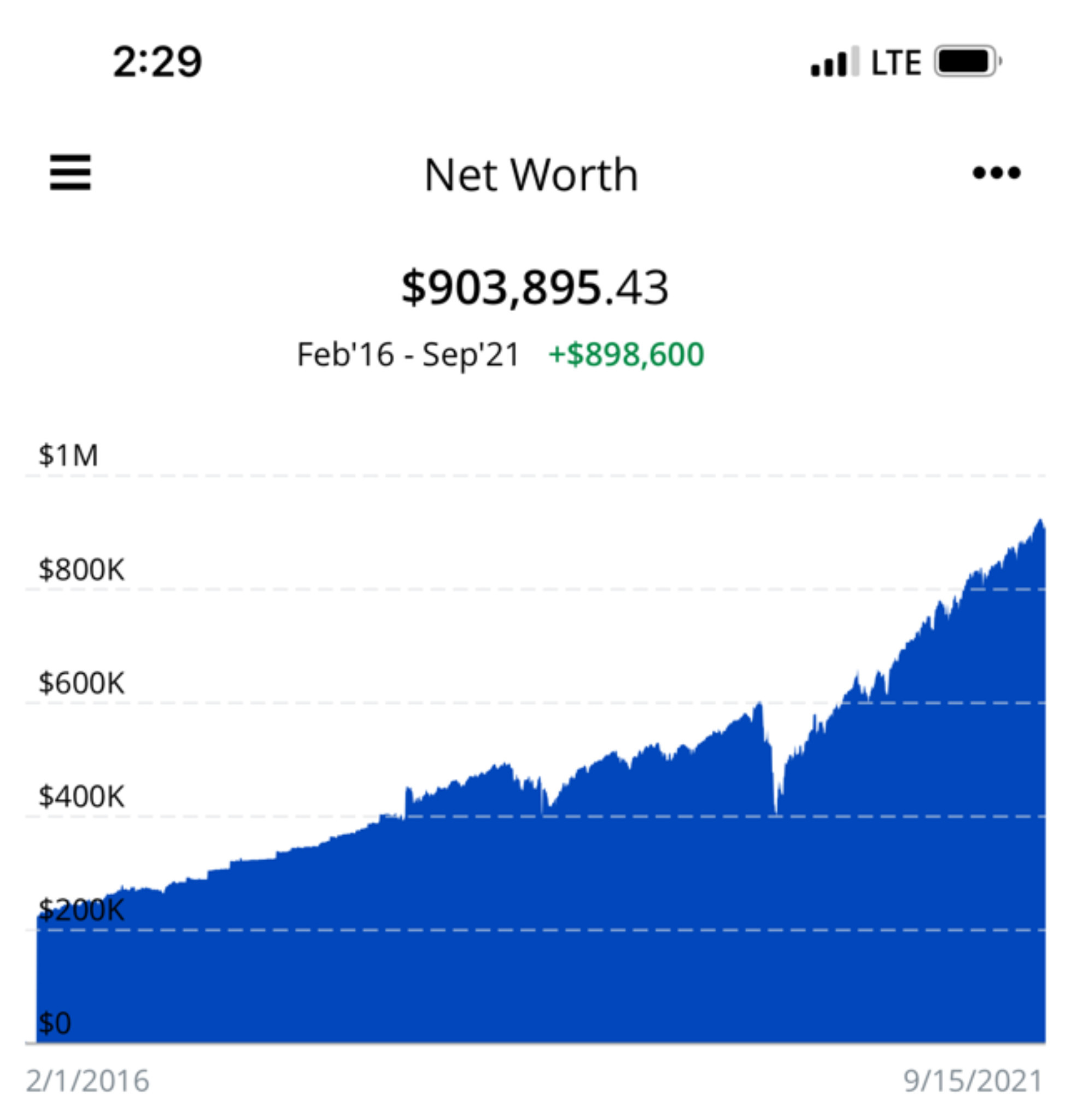

Conversation Starter

Conversation Starter

Best robo advisors for new investors?

When to buy back in to triple leveraged etfs 🔮

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Probably worth the cost of talking to someone who is an actual expert instead of randoms on the internet.

I’m sure he will talk to an expert. He is most likely doing some recon beforehand

Very impressive savings and low current burn rate. How old were you when you bought your first home?

First home at 27. Upgrade at 33. Still in same home.

Pro

Max out the lower brackets now with Roth conversions and delay Soc Sec. to 70.

When you have to go on Medicare at 65 you can soon use Roth distributions (after 5 years) to avoid triggering an increase in IRMA Medicare premiums which is income based.

The QCDs from taxable retirement funds to charity once you hit 70.5 satisfy your annual RMDs but are not taxable so also don’t increase income for IRMA.

Pro

Every year they look back two years to your tax return. So it is a rolling thing. If you retired or experienced a loss of income there is a form you can send them to try to avoid the increased premiums.

First off. Congrats on being retired. You have enough money to survive on 3% withdrawal rate in my opinion

First Look into Roth conversion ladder.

Next, I strongly recommend to read the 3 articles mentioned in the first post here https://www.bogleheads.org/forum/viewtopic.php?t=441794 (it goes over 3 methods of withdrawal during retirement)

also, you need to a full financial review before you make a decision on this. Questions like do you have any debt that needs to be paid off, do you have social security or pension coming up, etc. What does your health insurance situation look like (I know Medicare starts at 65 and you’re 61).

Why on earth a 3% withdraw rate?

Even the 4% safe withdraw rate had been updated by the author of that study to 4.7%, and it stands the test of even the WORST 20-year periods in the last century.

https://www.youtube.com/watch?v=sWf8VECoOcU&t=80s

If you only spend $80k/year, why are you withdrawing from Roth? You have nothing to worry about re Medicare premiums. Your income will not get you above the line. Live off the brokerage account. Take social security at 62. Why are you converting? You are 14 years away from mandatory withdrawals and you can spend down the pretax money in the next 14 years. Your mandatory withdrawals will be low.

Definitely spend down your IRA/pretax before RMDs start. After 63 you need to do it carefully so as to not incite big IRMA on your Medicare premiums. Do the math regarding spend down versus Roth conversions.

Thanks all. I was on the fence because they say you should have 3-5 yrs of cash on hand in retirement, so you can weather any market downturns. Guess I’ll stick to spending the “cash” this year and do the conversion as currently scheduled.

And yes, I will talk to a professional.

Do you really need 3-5 *years* of cash on hand?

You might be just fine with 1 year in a HYSA, and then a year or two in something very liquid like laddered bonds (I love tax-free munis), Treasury Inflation-Protected Securities (TIPS), or a tax-free money market account.

Beyond that, I would worry that a fat cash "safety net" is actually LESS safe, because that money could be sitting in equities earning you a lot over time. I wouldn't want to see you give up all that potential growth.

As others have said, a professional advisor might be worth it. Fee-only advisors will only charge you a one-time fee to look over your portfolio and make smart suggestions vs. a permanent advisor who will take 1-2% of your assets EVERY year = big time scam.

Seems reasonable. No one can answer without a lot more information.

I personally would not take the 40k out of Roth IRA and spend down the cash, but as I said above I don’t know your facts

I have an option that eliminates market volatility and taxes and also could provide income for the rest of your life.

Wow, a great financial opportunity has dropped in our laps because we participated in social media. How can we be so lucky?

You’re in a good position with substantial assets, but it’s important to consider the tax implications and long-term strategy when converting funds to Roth IRAs. Converting $120k to Roth could make sense if you expect to be in a higher tax bracket later or want to minimize taxable withdrawals down the line. Since you plan on using $40k of that for life expenses, you’ll want to ensure the conversion won’t push you into a higher tax bracket this year. Also, the $40k from cash can help avoid selling investments in your brokerage account to cover expenses, which can help reduce tax liability from capital gains. Have you considered consulting a financial advisor to make sure this aligns with your tax strategy and retirement goals?