Related Posts

Enthusiast

For those in private, how was bonus this year?

More Posts

Visual Storyteller

Is Woodford reserve double oaked worth the hype?

Any one register for DU event Hyd aug 5th

Hi, I am being offered 27L + 2L Variable for Manager (M1) at KPMG India. Will I also be eligible for year end performance bonus? Or is variable pay the only amount that I’d be eligible for?

Am I being lowballed by the HR in terms of offer ? Approx 8yoe currently at 21LPA (recently promoted) KPMG KPMG India

Additional Posts in Personal Investment Chatter

Conversation Starter

Will markets jump upwards the day Putin dies?

Conversation Starter

Pro

Conversation Starter

Conversation Starter

Conversation Starter

Conversation Starter

Used car prices starting to come down?

Rising Star

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Yeah, I get that people like metrics, but this one is garbage (although it makes me look great).

Conversation Starter

This assumes your salary stays constant and doesn't grow significantly so it wouldn't work for someone in their 20s and early 30s

This is the point to keep in mind.

My net worth is about $500k, at age 32, with a household income of $265k. By this absurd formula, I'm a horrible under-saver.

Never mind that:

1) My wife couldn't find a good career-type job until she was 25 and didn't find one with a good retirement match until 27

2) We had to pay off about $35k in student loans (not complaining! Loans were 100% worthwhile)

3) A year ago we were earning $210k, and five years ago we were earning $155k

One good bump in pay makes you "behind," which is ludicrous.

These rules of thumb are pretty dumb overall. If you're going to have enough for a healthy retirement that doesn't force you to make major sacrifices, then there's really no issue.

I wonder if this formula should be updated to reflect real inflation compared to salary growth from the late 90s to now. I believe this formula was originated then.

But playing around with some numbers, I see how this is still feasible at later stages of career.

Isn't this The Money Guy, not Millionaire Next Door?

I’m a 30yo ~2 to the money guy and a ~1 to the millionaires.

This doesn’t make any sense lol. You assume you’ve “accumulated” a 100% of a constant salary for 10% of your life. Alternatively that you should have accumulated 10% of your current salary since you were a baby.

Huge fan of the Millionaire Next Door. However, the formula has some defects depending on the scenario. For example, I’ve had 4 raises (2 promotions + 2 yearly review) since I started out of college 3 yrs ago. My salary is now 50% higher than when I started, so how does the formula apply here? Id say in 90% of the cases my 210k NW at 25 is higher, and should be consider at the very least an average accumulator not an under-accumulator as the formula suggest based on my current TC.

Chief

What happens if you’re married? Do you use combined salary and average age?

Chief

Oh good that’s what I used

Rising Star

Napoleon hill ?

Chief

Well I’m 24 with NW of about 1 year salary bc my salary just doubled. So I’m around 0.4N and an under accumulator? 🧐

It's possible if you bought property and haven't fully paid it off. NW also includes the property's value. One could be house-poor and still be considered doing well by this metric.

The ”net” in net worth means: assets minus liabilities. Always.

OMG, by this formula at 38 years old, I am indeed "Prodigious Accumulator of Wealth"

FYI, Average salary in the U.S. for 30year olds is < $60k.

Souce: https://dqydj.com/average-median-top-salary-by-age-percentiles/

Wonderful formula.

Apparently I need > $1.2m... Cannot be.

NW around $350k

We get it, your colleagues do not support your ego

I get the sentiment here to reach for the “millionaire mentality”.

But, for those of us who had thousands (close to 80-90k+ for me) in undergraduate/graduate school loans because of no help, no help with living expenses, no “hand me downs”, had to take care of family - a million and one various reasons - this barometer becomes very self-defeating.

I just started making a decent, non-coder income & was able to fully pay off my student loans, start really saving for a home, & put ample away now in my 401k & HSA relative to what I could before being in a HCOL/MCOL.

I love to hear the stories about those who are thriving as it serves as personal motivation & financial goals to strive for, but, TL;DR -

Your situation is largely dependent on the cards you were dealt.

Don’t be discouraged @ my <0.5N family here 😭

I may also be misinterpreting the math, but does this assume a standard/linear salary? Is that what the 10% is meant to offset?

I can tell you I make a lot more now relatively than I did from 21-26, which would be very tough today given inflation.

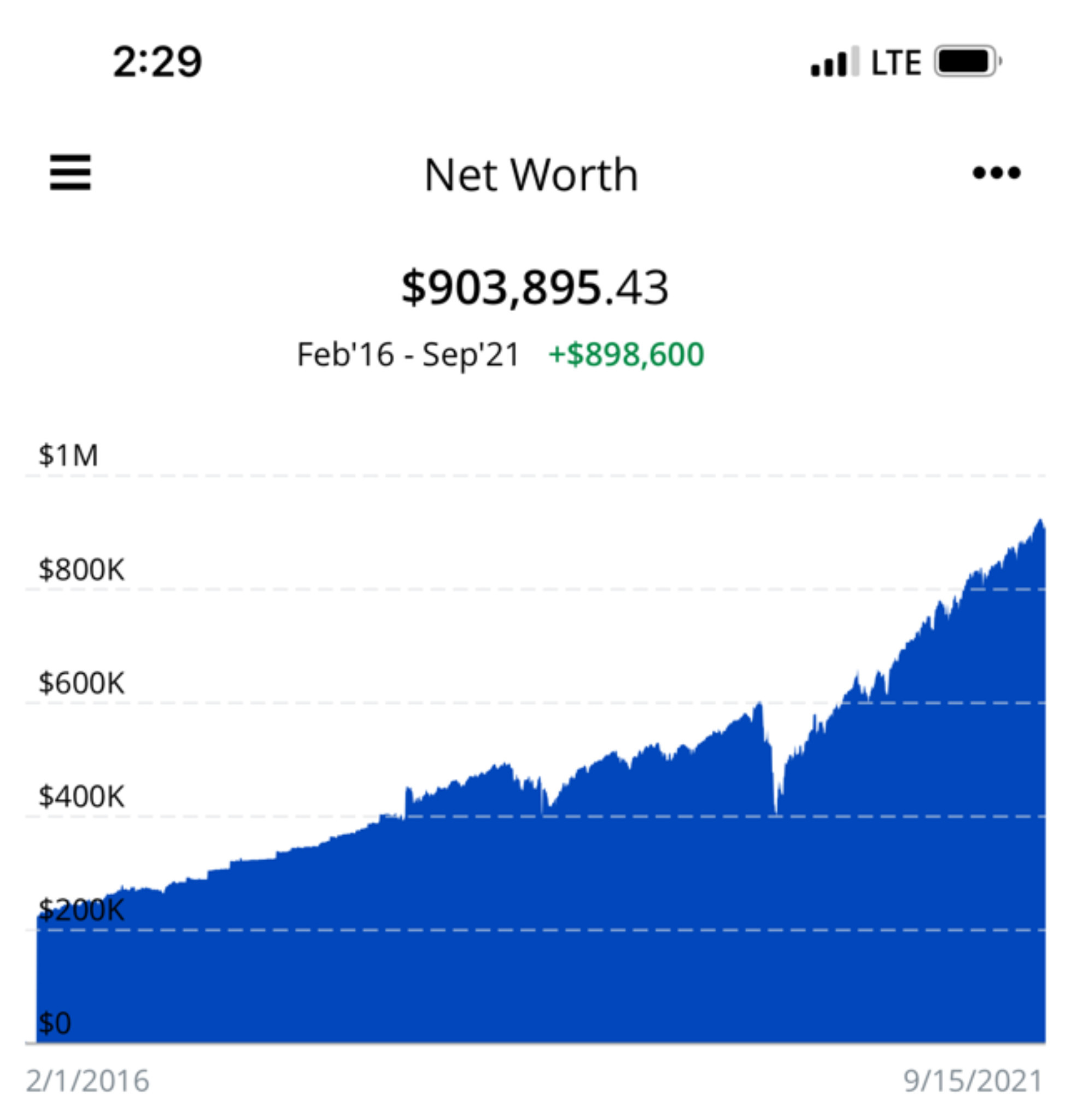

Apparently I’m under average with a 900k household nw at 31