Conversation Starter

Related Posts

Chief

Rising Star

Bowl Leader

Bowl Leader

More Posts

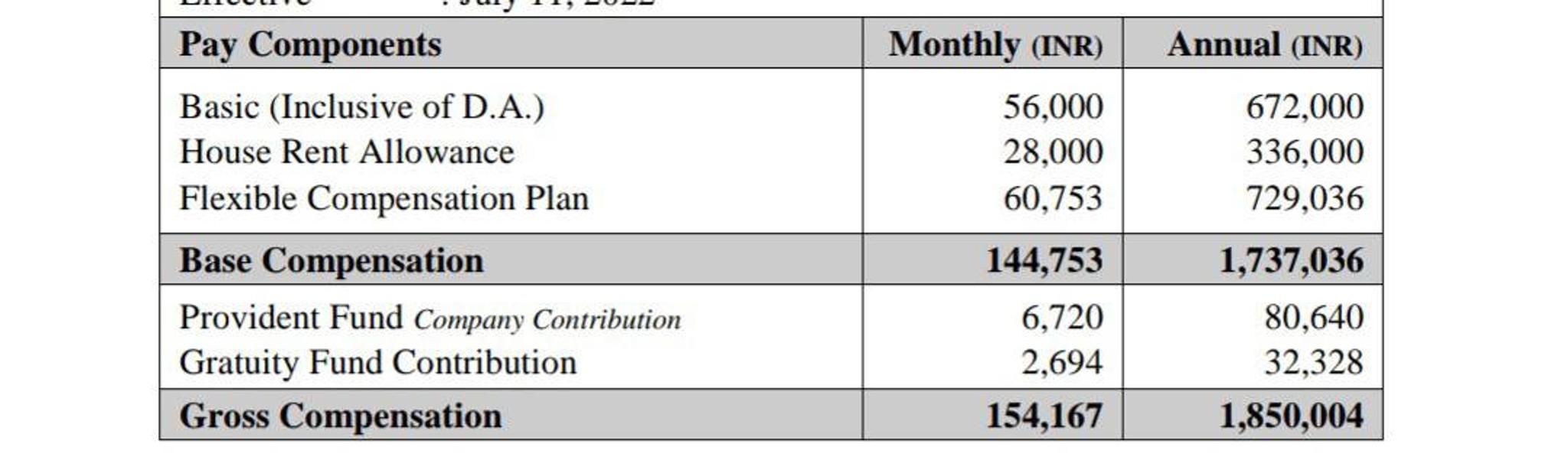

30/M/NYC 8 years exp, 162k

Rising Star

Conversation Starter

Pro

Visual Storyteller

Additional Posts in Personal Investment Chatter

Conversation Starter

Conversation Starter

Is this for real?

Rising Star

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Pro

If my rent would be $3,500 and mortgage for comparable place to live would be $7,000 I don’t think I’d buy in this market.

Especially if most of it is going to interest and taxes. All it takes is one layoff to make that a living nightmare.

I’d imagine it’s the same principle as leasing vs financing a car but on a macro scale. At the end of the day you’re building equity not building someone else’s

Conversation Starter

The equity is only the principal and appreciation. But loosing more in the form of interest, tax.

Try the NYTimes’s buying vs renting calculator.

https://www.nytimes.com/interactive/2014/upshot/buy-rent-calculator.html

What about buying an hr away?

We bought in 2020 at 1.5m. You have to believe in the appreciation story though as you stay longer at least in California prop 13 really helps. Two other factors which are not in any way guaranteed but could change the math is potential refinance potential after the fed pivots rates in late 2023 and potential SALT tax benefits in 2026 if congress lets the current legislation lapse as currently written.

I dunno your market, but I'm skeptical that the 3500/mo rent place is actually equivalent to the 1.4m house. I own a 2.1m house in SF and rent for someplace this size/location/quality would easily be 7-8k (not a lot of places like it are on the rental market though, so data is a bit scarce). My mortgage + taxes + insurance add up to just shy of 8k, not counting the effects of the mortgage interest deduction or the fact that a good chunk of that mortgage goes into equity.

I place a lot of value on the fact that I don't have a landlord that I need to keep happy. I'm free to modify the house to my liking and (assuming it meets code) nobody can tell me no. No risk of eviction. No risk of my rent going up just because the landlord wants more money (though of course other unexpected expenses can happen with a house).

I'm having trouble understanding what you're trying to say about the mortgage principal matching -- can you explain what situation you're worried about?

The thing about mortgages in this environment is that they are cheaper than the long-term return you can expect from investment in a broad stock index fund. If you could buy the house in cash, you'd actually be better off investing the cash and getting the mortgage, paying it off on the normal schedule. Even though that means paying a ton in interest! This is very different from e.g. credit card debt or personal loans.