Related Posts

Pro

Pro

Enthusiast

More Posts

Enthusiast

Iceland to Ireland 🤔

Advice on taking and passing the SPHR exam?

Coach

Additional Posts in FIRE Financial Independence Retire Early

Decided to payoff my mortgage.

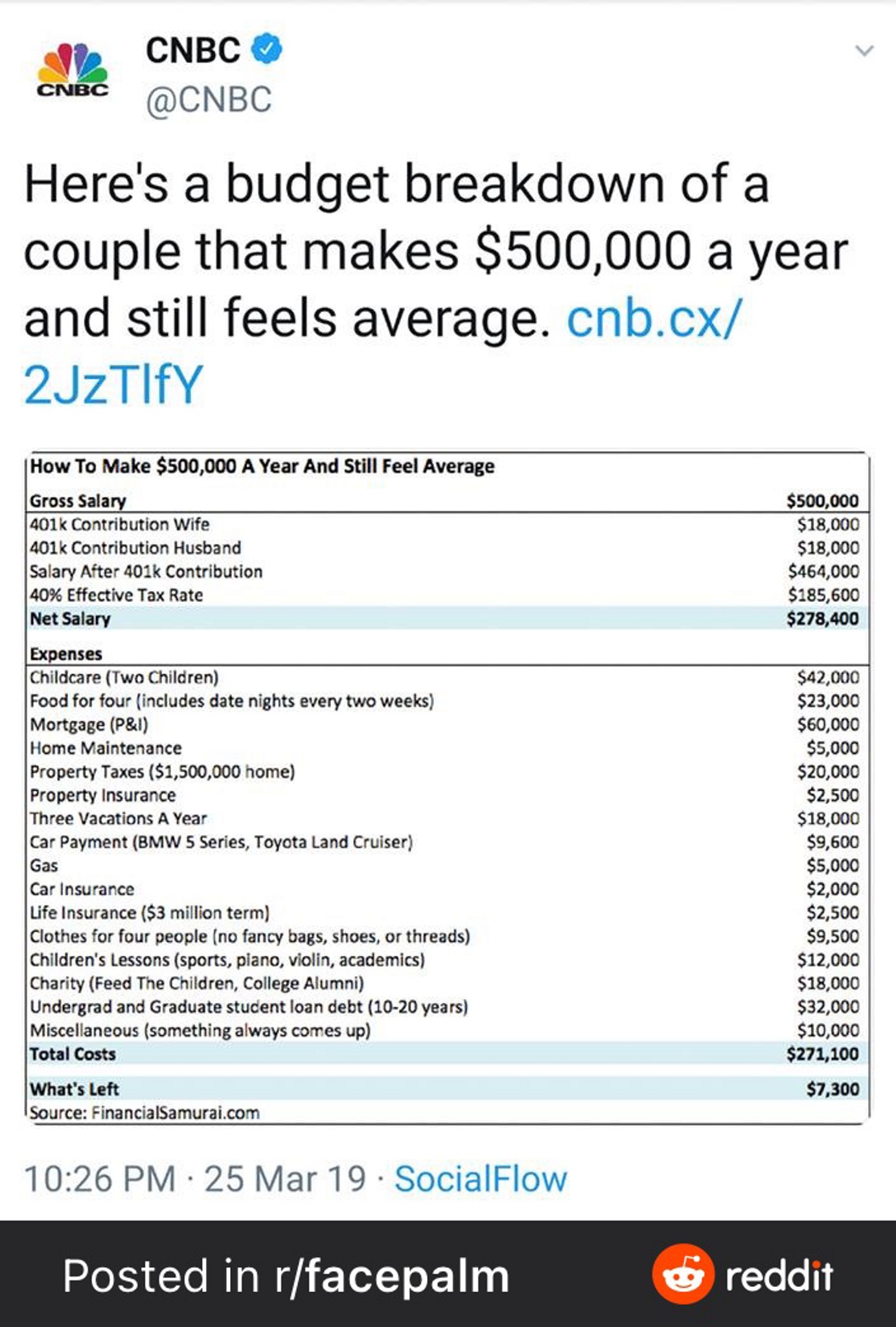

Nyc couple with $0.5m in income who feels average

Custodial or 529 for child?

Conversation Starter

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Might be wrong here but if you can get a better return in the market compared to the interest being paid, I think investing the money in a total market index fund will net more in the end

Thank you! yeah, I’ve considered that. I’ve generally been very risk averse though and am sitting on a lot of cash. But Am looking to retire early so decided to finally do something about it. I do have a good amount I can put towards both the total market index fund and towards mortgage, but trying to see if it makes sense to put it towards a higher balance or lower. Seeing the total interest at the end of 30 years scares me, but open to look at it holistically.

Assuming both are either personal or business related, it’s better to pay the shorter term/smaller balance one first. Both provide the same yield, but the shorter term provides liquidity/cash flow benefits much sooner.

Definitely not. If you have enough discipline to actually invest that extra money, the market will win out by a long shot over that time horizon. Absolutely no reason to put more money towards the mortgage.

So I’d have to check this on a spreadsheet but I think making the extra payments to the longer term will have a bigger impact because you will be paying interest on the open balance for longer.

Coach

Depends on your tax situation, but it is likely you should prepay the loan on your home property.

While it is likely your marginal home mortgage interest will be equally tax deductible as your rental as long as you itemize, once you are no longer able to itemize, your effective interest rate on your home mortgage will be higher than on your rental property, in which case you should definitely pay the home mortgage off first.

TLDR, if you plan to itemize, then makes no difference. If you don’t, pay off home first.

I did not consider this at all, so thank you for raising it. We’ve always been so far from itemizing especially since the standard deduction increased but this is good to consider.

From a pure $ perspective, put it towards the longer term.

Throw both those things into an amortization calculator and look at the monthly / yearly interest and principal composition. You’ll see the the longer term is more interest heavy at the front. Your regular monthly mortgage payment will stay constant, but if you pay down the principal with extra money, than more of each payment will go towards the principal!

That is purely a duration issue. If it’s the same interest rate, your annual rate of return is the same on either loan. Pure interest saved is meaningless

Mentor

Mathematically it doesn’t matter - the rates are the same.

If I were to try to maximize $ saved without changing much from what you have provided - why not refinance the 15 year?

Assuming the only reason the 15 is higher than the 30 is because it was originated when rates were higher; 15 year should lower rate than the 30 year because of smaller term premium.

My lender mentioned that since the 15 year is now a commercial property, if I were to refinance it, I would get a commercial rate (apparently ~1% higher). I did think it would be sweet to get a rate of 2.375% otherwise for the 15 year

Look at the amortization schedule. You are making much higher principal impacts on the 15 yr from the start, so going toward the 15 yr will only increase the impact on principal reduction.

Thank you everyone. This is super helpful!