Related Posts

Conversation Starter

SOL vs ETH 2.0?

Conversation Starter

Best family insurance suggestions?

Anyone have a good tax person in Philly

More Posts

Enthusiast

Never ending conference call

Rising Star

Larsen & Toubro Infotech Hi Fishes, I have offer from Optum , Larsen & Toubro Infotech and Luxoft .. almost same CTC. Luxoft joining is 25th (day after tomorrow), LTI and Optum are on 26th Wednesday. But I am waiting for Optum revised offer for the 26th.. Need suggestion to choose .. LTI progress is in onboarding state.. but my interest is more towards optum ..

Need help here ..

Bowl Leader

Community Builder

Additional Posts in The Real Estate Bowl

Thoughts on Fundrise?

Mentor

Coach

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

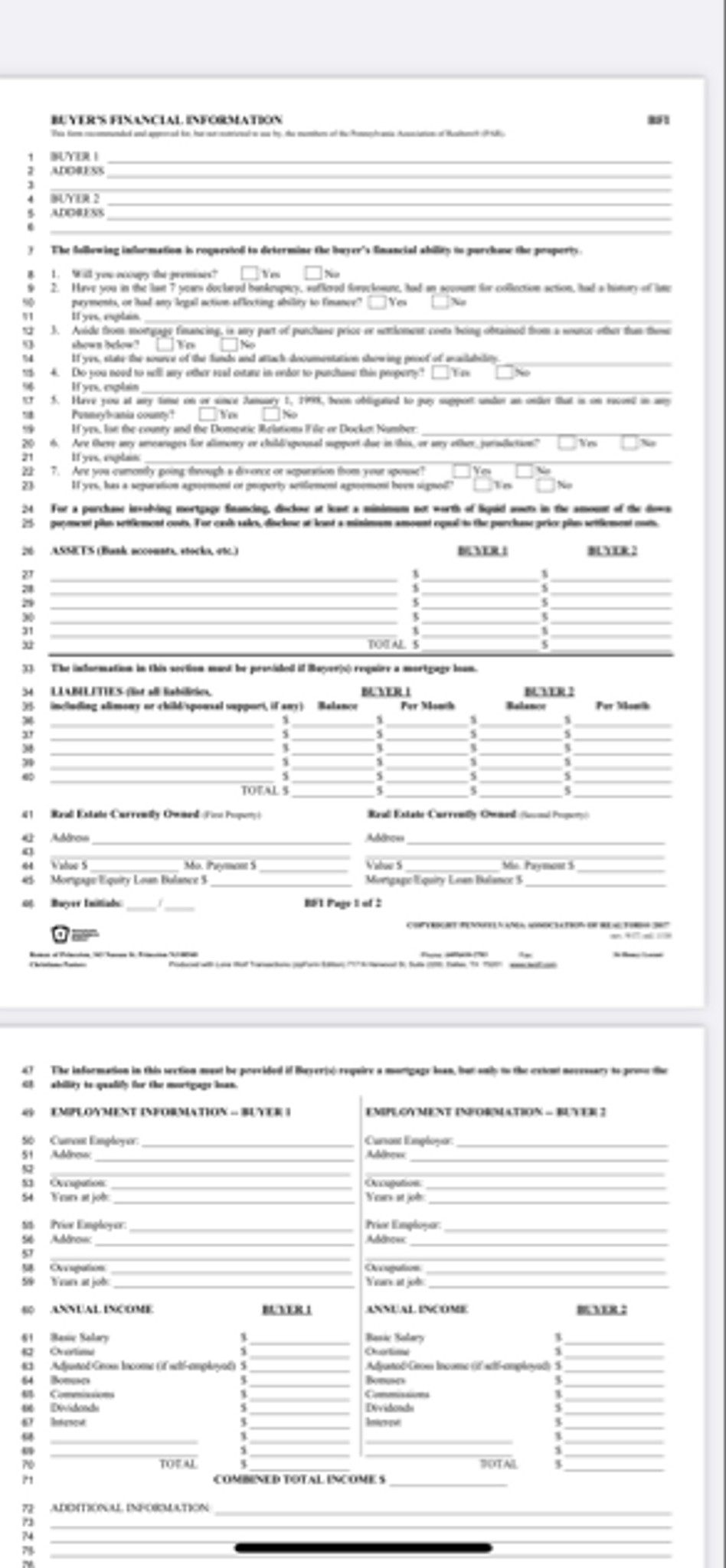

This is completely normal. That’s a standard form in PA - it’s to present your financial info to the seller so that they have confidence that you can secure a mortgage. It also gives them recourse should you not be able to come up with a down payment and misrepresented your financials.

Yes, I agree, practices vary from state to state and in different markets, so best to listen to your Realtor, since they are the expert in that market, and, because they are held to very high standards in their fiduciary obligations to act in your very best interest, you can usually rest assured that they are doing just that.

Super normal. I’ve been in Real Estate for 15 years. In a market where there are multiple offers, we see this all the time… It helps strengthen a buyers offer and help sellers make the best decision for them. The more transparent you are in your earnestness to complete the sale, and without any issues, the better chance you have of winning the bid. Sellers want to know that buyers are financially qualified, and they don’t want contingencies. The best advice that I can give you is that if you don’t do this, and you are in a market where multiple offer situations are rampant right now (despite interest-rate hikes, many markets are still very competitive like this), the other buyer offers will most likely include this info, appear to be a stronger offer, and you may end up learning the hard way by losing out on one or several properties that this info is pretty essential (under the current market conditions). I see it all the time. Better just to go with your Realtor’s advice and not put yourself through all that unnecessary.

+1

Also, as another user said, that is a standard form… you can tell by looking at the little logo at the bottom left, and the fine print at the bottom.

There is a pre-approval from the bank who does the robust assessment of your ability to payback the loan. This is sharing your income and assets and liabilities details with the buyer in addition to the pre approval.

PM1 - Definitely found your comment sarcastic.

It seems like earlier the buyer would also ask for your social security. I believe PM1 found that to be okay as well

Subject Expert

Proof of funds is sufficient. It can be “redlined” to remove personal info.

But your lender will need the details, and I wouldn’t be surprised if my buyers agent asked for proof of funds to not waste their time

Pretty sure that’s normal

Subject Expert

Did you think you could buy a house without showing that you have the funds to buy the house? 🤔

Don’t be sarcastic, this person could be a first time home buyer and unaware of how the process works.

When I sold my first house the offer included a screenshot of the dude’s e-trade account. Sure enough, the check cleared.

Cash although I’m sure he financed on the back end

I'm a Realtor in HI and I'd never share much of my client's information with the Listing Agent/Seller. That's shocking. A pre-approval letter and a bank statement should be enough.

That was exactly my thought until I started hearing from others.

This might be normal in PA, but not in MA or NH...we use pre-approval letters. That feels like showing too many cards at the poker table. Make a strong offer, with clean bank letter and drive to the commit date (appraisal in, good, fully underwritten).