Related Posts

Would you buy a brand new car in cash?

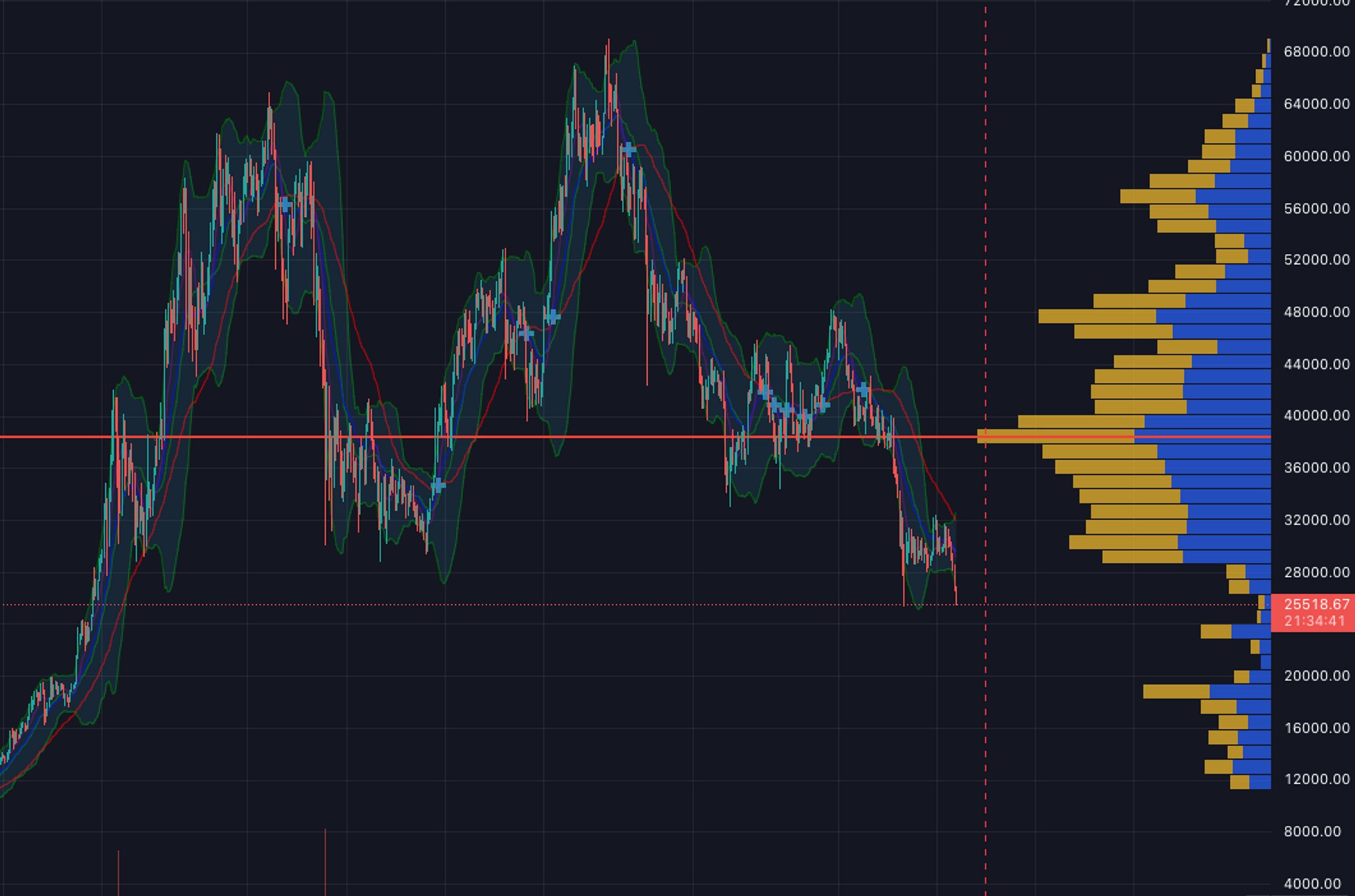

NFA, but will be buying up sub 20K BTC… DYOR 🥲

So what stonks are we buying?

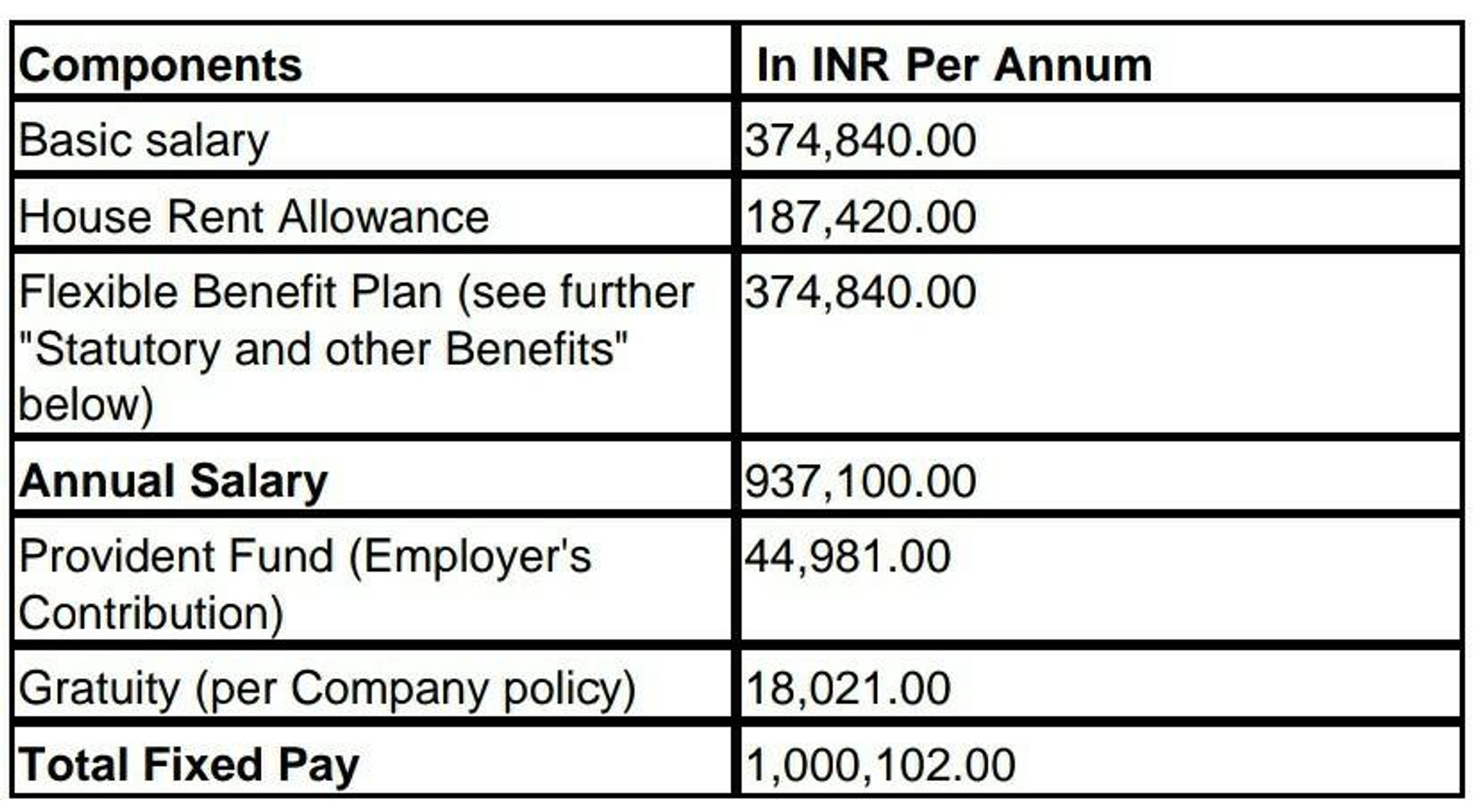

Bonus is out for EY GDS steps to see. Goto gdsindiapayroll.greythr.com, click on IT Declaration on left. Then click on My Tax Planner at the top right. Then click create my plan then click view it calculation on bottom right then expand income here under adhoc income you should see variable performance bonus amout.

Rising Star

More Posts

For all those in FS Advisory

Additional Posts in Student Loans

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

A

I’d go for the high interest rate, but smaller balance. Knock that one out. That’s been my plan, I’ve found the higher interest ones, and then start with the smallest to largest balance. My ultimate goal is to pay off all higher interest one’s then consolidate the rest. Anybody else have a ton of individual loans? I managed to have about 40 of them, I really wish I could go back with what I know now!

As someone who is just getting around to going back to school, I am asking with the utmost respect. Also out of interest to know how to manage my own expectations of my student loans..

How does one end up with so many? I mean I’d assumed you get your loan at the start of the school year or whatever and that’s the end of the loan conversation until next year.

Feeling very naive right now. Lol

Personally I would do A! Work on highest interest first, its where your money goes the furthest long-term.

Use excel to make an amortization schedule for both loans. Play around with the extra payments to see what you want to do. My husband had 3 student loans, and we made an amortization schedule for each one. This helped us know how to save the most money. We started paying more towards 1 loan, then once that was to a certain balance, we had to switch to pay more towards a different loan. A tip that not many people know, when you’re making payments, split your payment into 2 payments per month. For example, if your loan payment is $300 per month. Make a $150 payment 15 days prior to the due date, then make another $150 payment prior to the due date. This will decrease the amount of interest you pay over the term of the loan. Check with your lender first to make sure they allow partial payments before doing this.