Related Posts

Are Creative Directors rich?

Thoughts on SoFi bank?

Hi Guys, I am 5.5 years Java Developer and I have offer from JPMorgan Chase and Walmart .

Jpmc: 50% on current fixed + jpmc benefits Walmrat: 50% on current fixed + yearly bonus + stocks.

Please help me choose which will be better, mainly looking for brand value, work life balance and yearly hikes.

More Posts

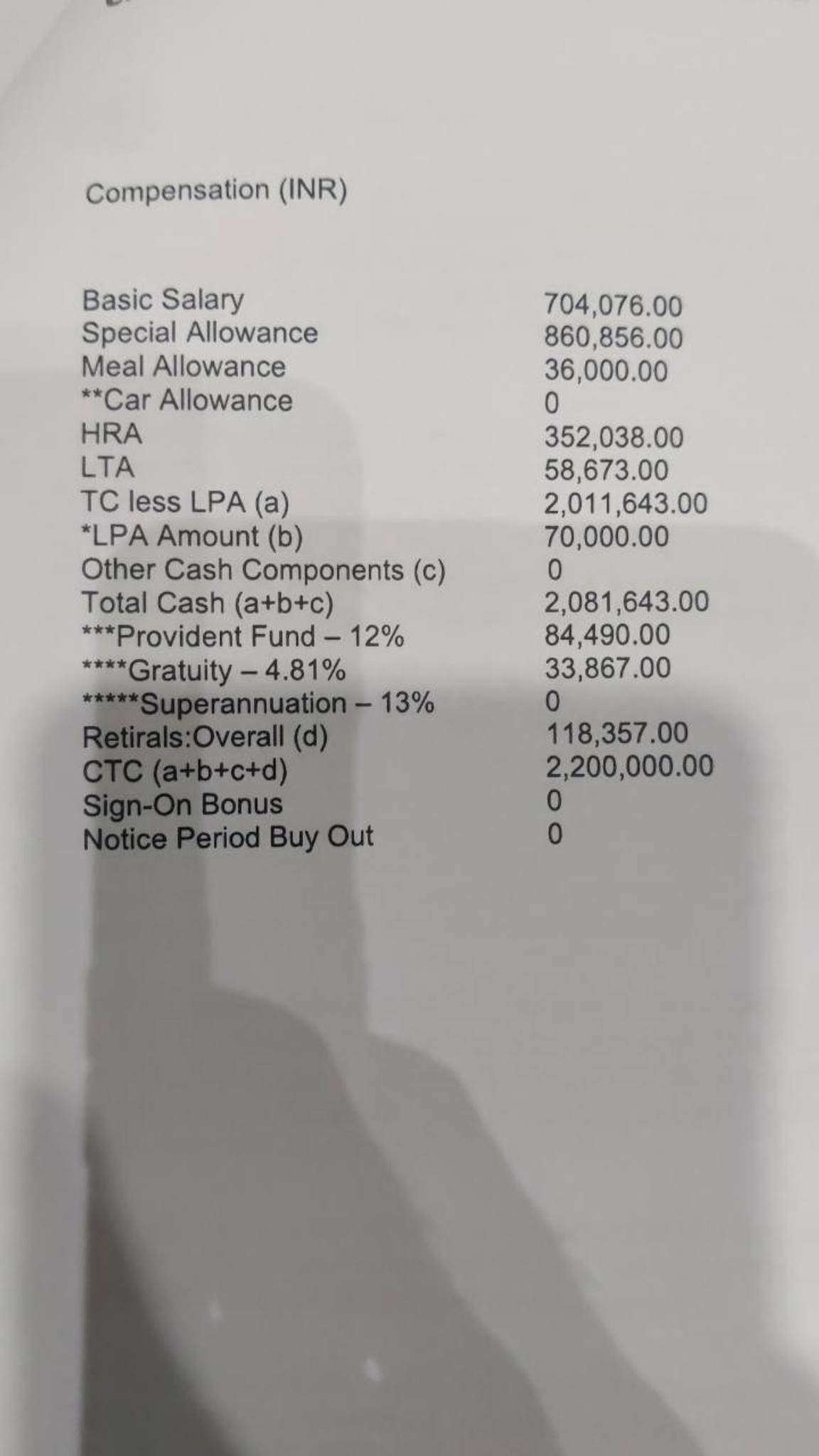

Can you please help me with the in hand salary

I’m making 55k in Chicago. Am I underpaid?

Additional Posts in WFH Freelancers

Day rate for ACD art in NYC right now?

Timesheet software “update.”

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Coach

I just opened a sep IRA with fidelity, it took like 30 seconds online (I already have a 401k thru them). Im waiting to see what my tax situation looks before I decide how much to fund it with.

If you’re an S Corp LLC you would get a Solo 401k, not a SEP.

I just transitioned to one recently since getting the S Corp approval letter.

2 major benefits:

-You can pay yourself distributions

-my accountant saved me $60k in taxes because I’m maxing out my employee contribution and employer contribution.

I got the Fidelity Solo 401k. My partner has the MySolo401k because he liked the option of being able to use the investment $ to buy real estate (to use for rental property) without penalty.

Real estate is an actively managed asset. That’s a big no no in a self managed 401k. You need better legal advice.

I worked with our financial planner to set mine up. I originally had a SEP but now that I’m set up as an S-Corp instead of a sole proprietor for tax purposes, the Solo 401k let’s me contribute more money to retirement , both as an “employee” and the “employer”. That’s the biggest advantage over a SEP, as I understand it. No big watch outs that I’m aware of and it’s worked out well for me.

I do something similar, my payroll company pays myself from my business account to my personal, and they take my 401k Contribution out of that

I have a SEP IRA which I think is the best choice for an LLC (which I have). You have to contribute out of the company, and it’s this weird circular calculation to determine the max you can contribute of your net income that your accountant will tell you. In general the calculation is approx 20% of net.

The nice thing is the max contribution is up to 58,000 for 2021 so if you are netting serious $ that is really nice.

A self managed one or are you just moving one to a new fiduciary? Big legal difference. There are only a few thousand investors in the country that do the former and it’s legally complicated. Not for casual investors