Related Posts

Subject Expert

More Posts

Anonymous User

Bowl Leader

Additional Posts in Personal Investment Chatter

Anyone looking at airline stocks or ETF play?

Conversation Starter

Conversation Starter

Used car prices starting to come down?

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Most places don’t let you do an in service withdrawl, so Roth IRA is prob off the table. Company funds usually have better fees, though.

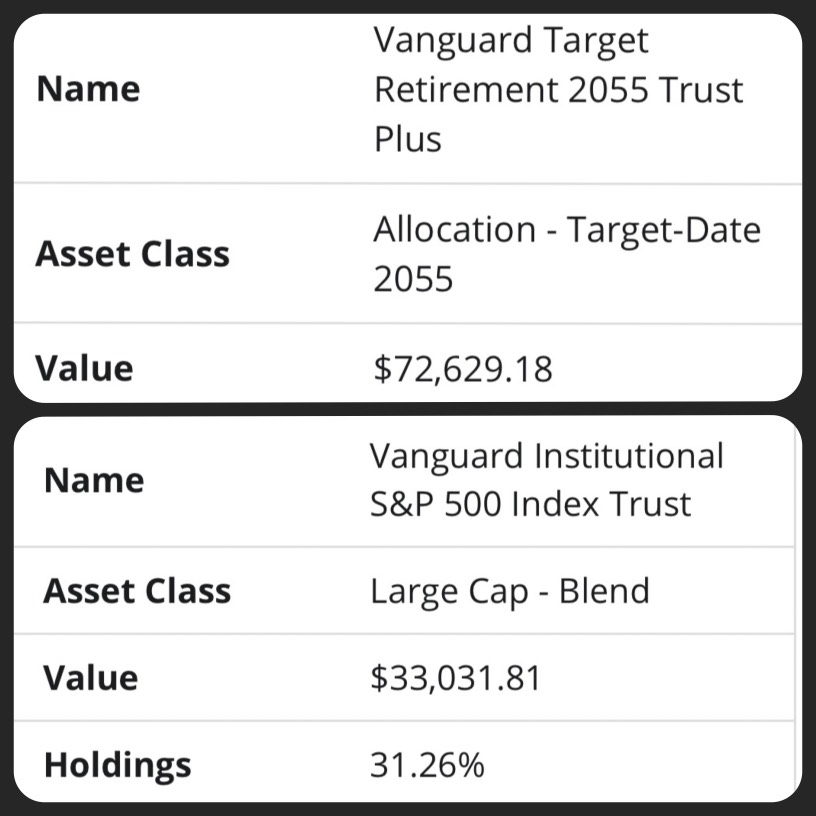

The 2055 will balance risk over time, so it is set it and forget it. They recommend you do all in that if you’re using it, but it’s personal preference. If you’re 30-35 and want more risk and lower fees now, you could transition it all to S&P

Yeah I’m thinking I want more risk and lower fees, and that $$ actually was rolled into this account from my old job at EY so is all that money been taxed already since I rolled it?

Bowl Leader

Some do, I believe KPMG allows it.

If it is allowed by your firm, why do you want it to be be in an IRA instead of 401k?

I can think of a couple reasons (flexibility, higher ira balance for bonus or status/tier, planning for FIRE down the road) but none have been compelling enough for me to bother to do so even though I'm pretty sure I can.

Also note Roth to Roth is tax free but any employer matches are pretax so they'd need to be converted (taxable event) or put in a traditional IRA.

Are you still employed. If so you probably can’t move money from your 401k to a Ira

My point is if they are at the same company they probably can’t take out of 401k to Ira. If they left year they can. When I ask if they are still employed I meant at the company with the 401k

Call Dave Ramsey.

For clarification, I am still employed at the same bank and my bank DOES allow in-plan Roth conversions.

Because you can do trading in a Roth IRA and I could potentially make more money via tax free gains - does that make sense?

My thoughts behind a Roth IRA is it gives me more control over my investment options rather than having to pick from a limited amount of preselected options in a 401k

Ok but I am not sure you can do that. You need to find out if your 401k allows it. I suspect they don’t.