Related Posts

Hi,

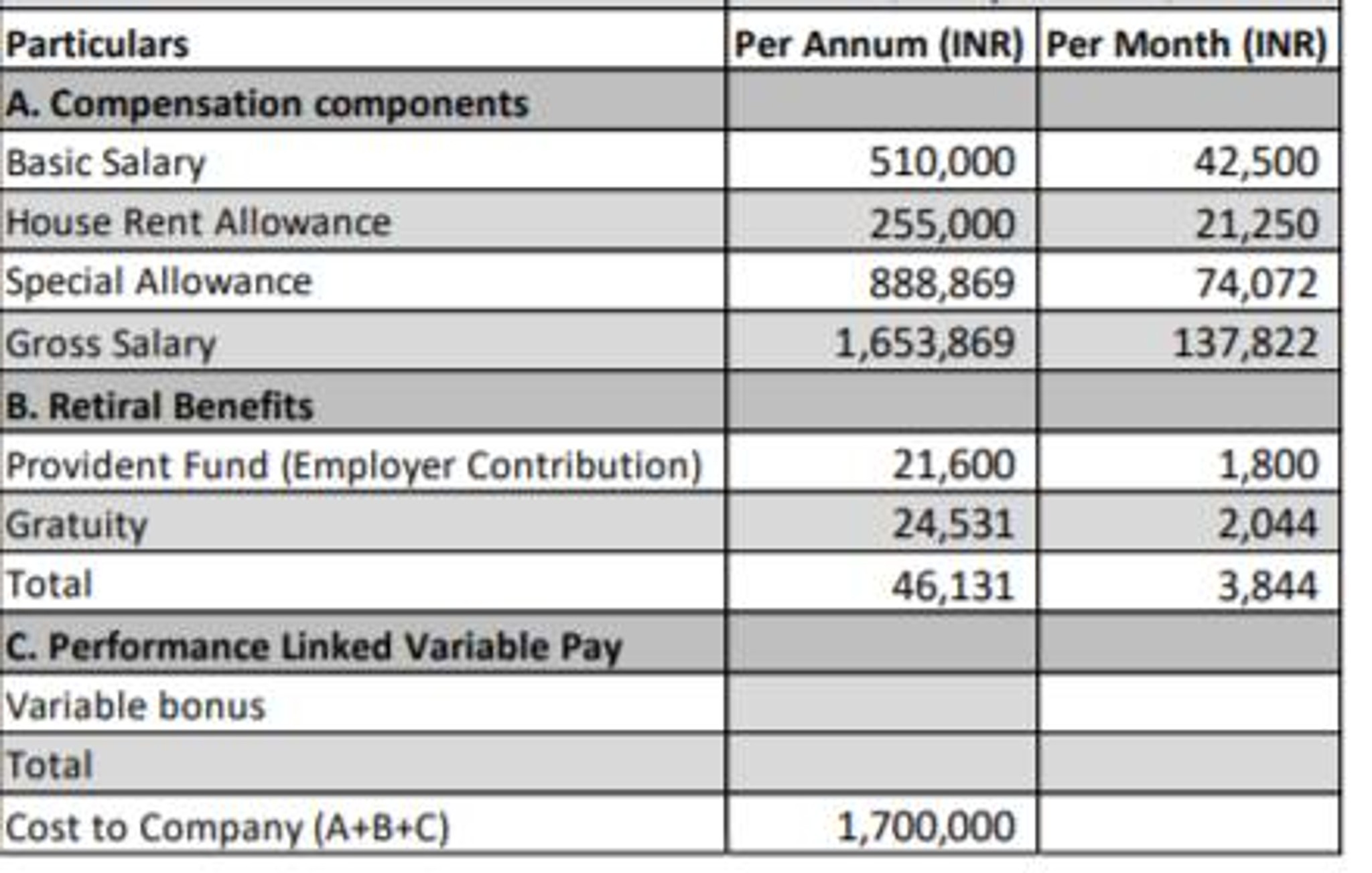

What will be in hand salary

More Posts

Conversation Starter

Conversation Starter

Additional Posts in FIRE Financial Independence Retire Early

Anyone a CFP as a side hustle?

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

Things move super slow for the first million.

Unless you;

- inherited money or

- got super lucky with your investments or

- in the top 1% in your field or

- Come up with a brilliant business idea; you should not compare it with the one in your example.

If you make the first million by your 40s, you are one out of 20 financially well-planned individuals in US.

Currently 47 years old. Married with 2 kids (17 and 14). Bad decisions and gambling addiction in my early 20’s and had 0 401k/savings until 2005. Kind of hit the reset button when I got married and started with a new company. Total household income was about $70k in 2005. I got one promotion in 2008 and total household income went into the low $100’s. Never adjusted our standard of living and saved all of the leftovers.

I got a large promotion into management in 2015 (which forced us to move) and our household income went to $160k plus cash/stock bonuses (not guaranteed) up to 150% of my base salary. Still no major changes to our lifestyle. Paid off $270k mortgage in 2022. We live well below our means, take 1 very nice vacation each year and stay the course.

No debt. Currently sitting at about $1M in liquid assets between brokerage and emergency fund. $1.9M in 401k.

How did we get there?

1.) Avoid lifestyle creep as income increases. Can’t stress enough how important this is. Keeping up with the Jonses derails many retirement plans.

2.) Luck. Company stock did me very well over the years. Roughly 1/2 of our brokerage account is a result of that stock. Company stock outperformed the S&P 500 by about 4x since 2006. Very risky to leave that many eggs in one basket, but we have diversified most of it over the past 2 years.

3.) Clear plan and aligned goals. Both sides of the marriage need to be on board with the saving plan. It will not work if your goals are not aligned with your spouse.

4.) Avoid lifestyle creep and keeping up with the Jonses

5. Take advantage of whatever 401k match your company has. Max out HSA and don’t use it. Pay off debt with interest that’s above what you think is reasonable for ROI% on a safe investment. Max out IRA/Roth then max out 401k. If there’s any left, put it into brokerage

Maxed it out every year since 2014. Company 401k match is aggressive and over 1/2 of our profit sharing goes into it each year

32 single female. I started in Big 4 in 2016 $52k base. My base salary hit over $100k in 2022 when I left Big 4. Now my base is $127k. About $5k-$10k in bonus. About $5k-$10k in dividends. I’ve always tried to invest 50% of my income after taxes. My salary isn’t the highest, but I’m fairly frugal. I learned my priorities at a younger age than most and have spent accordingly. I still split subscriptions with friends and family. When I worked at big 4, they paid for most of my food and I had lots of left overs. While my parents haven’t supported me by giving me money or paying for my things post high school, they support me emotionally, taught me what they know about finances, and let me use their senior citizen discounts.

I started out in big four in a LCOL area. My partner said when I was an intern that I should expect to hit 6 figures base after manager level. I know smaller firms may not pay as much. When I was a senior 3, my base was $83k I think. When I left for public for private, my base increased to $98k then $114k the year after.

Coach

What do you want to know? I didn't break $100k until I was 30, $200k at 34. Hit $1m nw at 36. Just worked and consistently saved 15-25% of pay check.

Coach

I went to school for accounting. I got a job in public accounting. I followed the standard promo path.

The bigger issue is people double counting their money when their NW is shared with a spouse. Cut it in half when you represent your numbers.

Marriage is the greatest finance hack there is.. if you and your spouse have the same financial mindset.

I'd love to post here just because I never have. I'm not sure if we'll ever hit FIRE, because we want my wife to be home with our children (both of us had really bad upbringings) but I'm an average guy working with a fairly mediocre salary.

I'm 34, we just broke 200K liquid net worth a few months ago. Mostly due to the fact that my wife was working full time until the end of the school year in 2025 and we could save almost 100% of her salary. Our NW increased by almost 90k last year alone

I make 75k a year, and now a large amount of my income is going to regular COL expenses.

That said, I'm also in a masters degree (Trying to increase my income) and that's 6k every 4 months that we can thankfully pay out of pocket for the next 2 years. The hope is that during these same two years our NW stays right around 200k until I've graduated. So there are LOTs of people like me just trying hard to scrape some savings. And just time makes all the difference. I'm nowhere close to 1M like everyone else here, but maybe in 10 years? Maybe 5 if my income goes up. Regardless, I'm just going to keep grinding.

I am on same track. Wife not working and living in high col area. House has 300k equity and thinking of moving. Just got laid off and seeking next shelter. 550k in 401k and 100k liquid. Selling stuff in house to close gap each month.

Move to lower col area or tough it out? Mortgage is 2%, so considering making rental.

Does it matter?

Available to everyone and likely to work: Live below your means, invest in equities.

Everything else is situational or so unlikely that you shouldn’t worry about it.

the more you stack, the less your w2 income matters

Single M40. $2.2M net worth. 5% in cash/equivalents, 5% in crypto, 15% in home equity, 40% in 401k/IRAs, 35% in brokerage.

Worked hard to save money my whole life. No family money, public school kid. Worked odd jobs through high school. Got scholarship to college. Worked through university. Went to an expensive law school. First semester ate my entire life savings. Took out loans for the rest.

Got a job at a big law firm at age 27. Paid down debt instead of saving (other than company 401k contributions). Finally hit positive NW in 2017. Have saved 50% of my take home pay ever since, almost entirely in S&P and Nasdaq-pegged ETFs and a little bit of crypto.

Took 3 years to hit $500K, another 3 years to reach $1M (took lower paying job). 2 more years to hit $2M. Along the way bought a house but it’s still mostly debt.

On track to hit $5M before 50. Hoping to be married with a couple of kids by then and coasting.

My path wasn’t particularly lucky. Do well in school with a natural track to a high-paying job. Save aggressively. Avoid unnecessary debt. Let money grow in the market. Still had a zero net worth in my early 30s but had set myself up to grow quickly after that.

Looking back I would have tried harder to get invested assets growing sooner (savings and potentially real estate), but 8-9% student loan rates scared me too much. But my path spanned the Great Recession and COVID, as well as 12-18 month dips along the way. Things recovered every time. Just be steady, smart, and intentional about staying on track.

I think you guys are ignoring the “30” aspect. No amount of compound interest is getting you that by 30 on a 100K 200K or even 400K salary

Mentor

You stated age 30, OP

The fact is very, very few people under 30 have $5m.

It’s not realistically achievable for the vast majority of people.

Some very talented or lucky people might achieve it, but it’s best not to get hung up on it.

Of course if you earn $400k at 21 then you make $5m. The top 0.1% of people are gifted and can do that.

Don’t give yourself a hard time if you aren’t exceptional.

I spent all my money on experiences in my twenties and early thirties. I had some emergency savings and the standard annual 401k amount but the rest were spent on travel and buying things I wanted: sports car, watches, etc. I made a lot of money compared to my peers back then. I still make a lot of money compared to my peers. I’m still on track to FIRE by 58 (chosen to align with my spouse’s pension vesting).

As others said in different ways, it’s time in market so it starts slowly in the beginning and then at some point it snowballs but then you really stop watching the five figure +/- movement on the daily tracker of your Fidelity account.

42M. $2.75M NW. $915k in retirement accounts, $593k in house equity, $590k in brokerage, $511k in vested company stock, and $140k in savings. I was consulting for 14 years. Always saved into retirement accounts from the start and saved up to buy a house early on. Then in my 30s I started invested in my brokerage accounts heavily and did the minimum on the retirement accounts for matching. 7 years ago finally left consulting for tech - and that helped me get the company stock vesting and took advantage of the employee stock purchase plans.

I can't relate because am from African and am just a graduate

I would say growing up poor is why I’m frugal and hardworking now. Nothing handed to me.

-Married, 38 yrs old

-Household NW of $6M

-$400K in home equity, rest in investments, 401K, etc.

-Hoping to leave the rat race in a few years

Coach

What’s your planned spend and how do you plan to fund it, besides the deferred comp payout that you’re anticipating?

Don’t wait to get to $10M, the time now with your family is precious and by the time you hit $10M, you might shift your goalposts again.

Also, if you’ve planned properly - your NW will continue to grow, albeit at a slower pace.

I originally wanted to leave at 40 or $10M, whichever came first. Instead I left at 37 with $7M NW, spouse and 2 kids below 3. Two years on our spending has increased by 150% but NW has grown to $8.4M despite not earning any income.

So would advocate for pulling the plug sooner rather than later as time with your loved ones is something you can’t get back whereas you can always figure out ways to make more money later on.

It always reminds me of the Flywheel Theory in business. Things start off slowly and it takes a lot of effort to get anything moving, but eventually things accelerate. Investing is very much like that, as things compound and time passes the initial early effort pays off exponentially.

Life isn’t fair though. You will see people who are wealthier than you.

I love that you asked this because I have always wondered myself. I would assume people save from their salaries but how do you save so much so fast?

Yes, but at 37 I had no investments (wasn’t even contributing to my 401k) and was $100k in debt. My salary was $155k/year at that point and I lived in NYC where my rent was $4k/month (idiot, I know - I should have had three roommates and not lived alone). My point is, if I had started out by living well below my means (which is the number 1 hack) and contributing even nominally to my 401k, I would have had a bunch of money at 30, even with low salaries as I started out ($30k at my first job).

Subject Expert

I married into money. My wife's father invented toaster strudel.

My wife invented the Post It notes.

Visual Storyteller

Was on an academic scholarship to cover undergrad tuition. Room and board was paid via part time job, grandparents and parents.

Worked during grad school. So no student loans.

Childless by choice

Live in a LCOL area, bought my house after the 08 bubble burst.

Remember people start the game with varying amounts in the bank account and different life circumstances.

Sometimes I feel like the stats in this bowl are like an aol chatroom circa 2004

37/LCOL/$1.1M (excluding spouse)

I (we) have been horrible at saving so this is NOT a path anyond should follow, but if it's helpful to anyone this has been my path.

Bought my first home while in college with $10k down (used part of my studen loan!) rented out to roomates that covered my mortgage and made $.

Single from till I was 28, married, dink's for ~7yrs with HHI of ~$200k. By 35 I'd made & saved about $500k just from moving (3 corporate moves by then). Have been single income ever since. At 36 I was making ~$140k base and left for a competitor at $220k. 1yr later I left Fortune 500's to work at a small manf business making $250k +equity. At 38 moved to CA and bought our home for $1.4M comps today are ~$3m. At 40 I joined a startup and took a $30k salary +equity. At 43 I was at $350k base, $200k bonus, and $500k annual stock. At 44 the company went IPO, at 45 I left to join another startup, currently making $275k + equity.

So, combined net worth is ~$6m. $2m in home equity, $1m in other real estate investments, $2.5m in brokerage.

$250k in 401k and $250k on my wrists!..(don't do that!)

responding to OP's fwp question (for some reason I couldn't reply directly to that).

NW when I took a chance on the startup was prob $3m? Not sure. most of it was in the house, but that startup paid off with the equity I had + real estate keeps climbing.

Reading these post are reminders of poor financial decisions I made. At 50 F working at my current job for 17 yrs making $120k (plus $5k -$15 yearly bonuses) with $30 in 401k , $4k brokerage. $340k mortgage. $50k student loan debt, kid is grown, remarried spouse makes $70k no 401k to start until Jan 2026 ..he has a small pension. I was forced to cash out my pension and My ex took 40% of that. Had to start over and pay many debts through my years of making bad money decisions. What advice would you give me to become FIRE?

Subject Expert

That's a tough situation for FIRE, no question.

What is your gross income together with your spouse? How much do you spend each year as a family? How much do you save each year? How much equity is there in your house?