Related Posts

Conversation Starter

what you buying?

How did you get into real estate?

How do filmmakers find investors?

More Posts

Good entry point for PLTR?

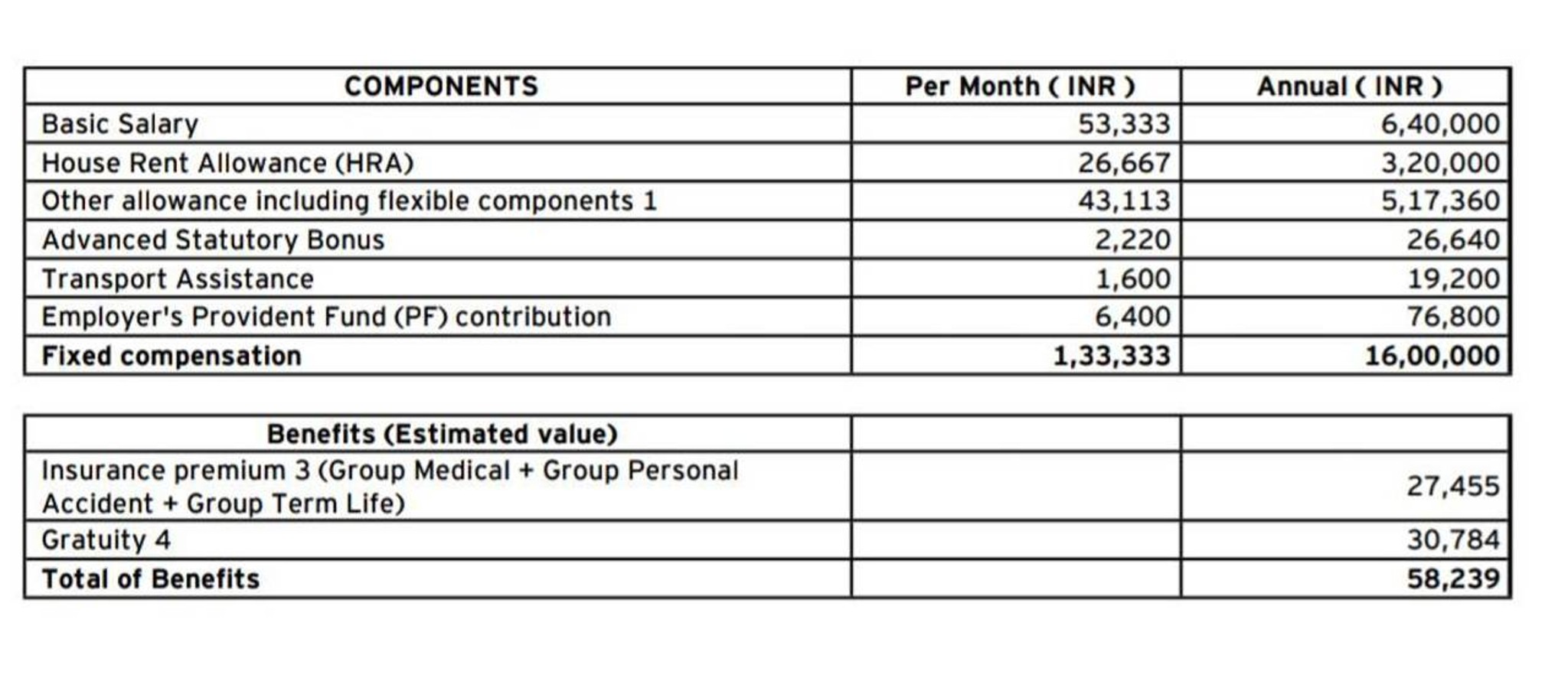

Hi Fishes, I am immediately looking for job change in Software Testing Profile(Automation/Manual)Testing. I have 4.5+ years of experience in implementing test automation using Robot framework and Selenium web driver for web applications and Postman(API testing). Excellent knowledge of SDLC, test case writing, defect reporting. Involved in training the virtual assistant(Chatbot) and RPA development. Performance and Database testing, Unit and Integration TestingAccentureGlobant HSBC India Citi

Additional Posts in FIRE Financial Independence Retire Early

Real Estate Rookie podcast thirsty for subs

Decided to payoff my mortgage.

New to Fishbowl?

Download the Fishbowl app to

unlock all discussions on Fishbowl.

unlock all discussions on Fishbowl.

I'd be retiring rn if I were you.

Coast FIRE. Sign up for some temp/contract/seasonal work just to keep some inflows.

Mentor

Wow, great job!

With the separate accounts added in, aside from 529 (which will already grow enough to cover 4yrs full cost of UCs, for instance), you're already at more than 25x your yearly costs.

So: Retire now & enjoy these precious early years with your little one!

(If you had to, you could do some baristaFire sometime over next 23 yrs pre-Medicare to cover health insurance - maybe when your kid is older and doesn't want to hang with you much anyhow ;) )

Mentor

Actually, not really Barista fire: Assume that over the next decade, you will stumble on something that you would *love* to do part-time, even if they didn't pay you. And I'll bet they will anyway, at least enough for health ins ;)

Own home, but high property taxes

42 years old

Set aside separate amounts for the lifetime one offs (will be invested and hopefully grow:

60k big home repairs

80k cars

50k vacations

Single Mom, one child 4 yo, 100k in 529

Proposing to RE very soon.

Thanks, I am fortunate enough to have an ex that for now can pick up child healthcare if I can’t (obviously at a cost to me). So, to be fair I am more like a single half-Mom.

The hardest part for me (two under 6) is the childcare costs. That seems like the X factor.

Even with insurance - unexpected hospital bills / broken limbs. Then add in future schooling costs plus extracurriculars, camps, etc.

All that to say I feel comfortable with what I can model for myself but have struggled to project how their costs will change over time.

I would continue until at least 3m before retiring with those expenses. Otherwise I’d anticipate having to cut back in retirement.

That makes sense too- I just know my car need or my home emergency or my vacation will come before I have saved for it or predicted it - so I wanted to start with those funds. For me budgeting 100 a month and then spending 15000 on a roof a month later isn’t how I like to plan.

Having the separate buckets for lifetime one-offs outside the $2.3M in retirement is a great way to keep the nest egg calculations clean for regular expenses. Have you also considered how you plan to replenish these separate buckets as you spend them down?

I’m adding all expense items to an annual budget - so in my case if I want to budget for a new $50k car every 5yrs, then I have a $10k annual budget. I also added budget lines for vacation travel, etc.