Related Posts

Conversation Starter

Personal finance book recommendations?

Conversation Starter

More Posts

I am working as data engineer at Accenture with 2 YOE with ctc of 11LPA. After clearing all the technical rounds at Impetus technologies, tomorrow I have my HR discussion. She told she can't give more than 16 LPA. What should i do? How much should i ask? I am expecting somewhere around 19-20 LPA. Can anyone pls help. Accenture Impetus technologies inc

Subject Expert

Bowl Leader

I have a fair amount of retail experience and have created a bowl to help fellow consultants who are interviewing in retail and CPG. My experience is across a wide range of topics (primarily non technical) and would love to help folks get their dream job. Would be awesome if others can join and contribute their knowledge.

https://joinfishbowl.com/bowl_pyw52xwun1

Additional Posts in Accounting

What makes you really happy?

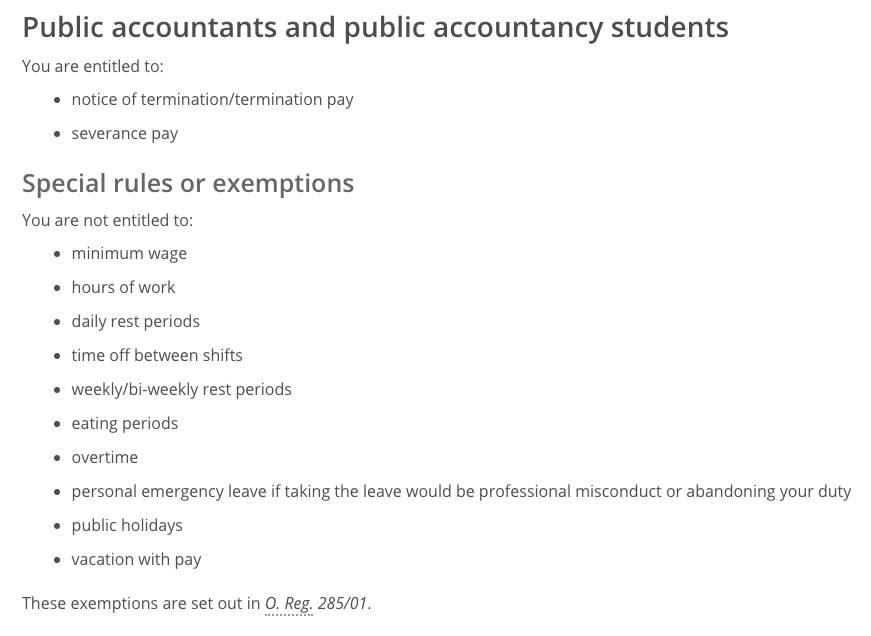

TIL: I don't have rights as a public accountant

Chief

New to Fishbowl?

unlock all discussions on Fishbowl.

Dump it into an S&P 500 fund and forget about it. Warren Buffet style

Marry rich

Lol that ship has sailed. Already married 😜

Put into Traditional IRA. While you don't get the tax deduction, it'll still grow tax free.

You can back door convert to Roth at a later date if you want when you're in a lower tax bracket.

If it is only 5.5K or lower, you can contribute to regular IRA and then convert to Roth IRA right away. This is commonly known as back for Roth. If you are working with a financial advisor just ask them about back door Roth IRA and they will walk you through it.

Give it to me I’m broke

If you are eligible, look into HSA.

LendingClub (you buy debt on a P2P basis basically)

Put into 401k post tax (up to 56k it’s limit). PwC allows for in service distribution of post tax, which you can roll into Roth. It’s a mega back door. I do often.

To clarify. PwC only offers 401K. The process goes as follows.

Pretax 401k limit is 19K

You can continue to contribute on post tax basis up to I believe 56k this year total contribution (includes your contribution, the match and what goes into wealth builder). This is readily available to set up within our system.

The second step is to call benefits express and ask them to cut a check for the balance of your post tax contributions. They will cut a check to your Roth IRA custodian for your benefit. Forward you check to your custodian and you are all set.

6k Roth limit and phase out only applies to direct contribution. You are rolling over your balance similarly as if when you would have left the firm and your pretax would have gone to traditional IRA and post tax into Roth, but since our 401k plan allows for in service distributions one dos not have to leave to roll over balances.

Set up an appointment with a PWC financial coach and they walk you through the process. Can also google “mega back door into Roth IRA”.

HSA and Backdoor Roth will be the next steps. I prefer HSA only and skip the Roth as it is just another step I have to do. Otherwise I use a lazy portfolio and otherwise am a Boglehead.

Isn’t the HSA max only 3k

Why lock it up in an account you can’t touch for 30 years? Build your post tax savings to provide liquidity as a part of a balanced portfolio

Whole life insurance

Damn you old!